Jump to winners | Jump to methodology | View PDF

MPA’s Brokers on Non-Banks 2024 survey cements the broker-lender relationship as a cornerstone of the complex mortgage market. Non-bank lenders continue to carve out a bigger chunk of market share by combining high-quality products with competitive pricing and delivering them with speed.

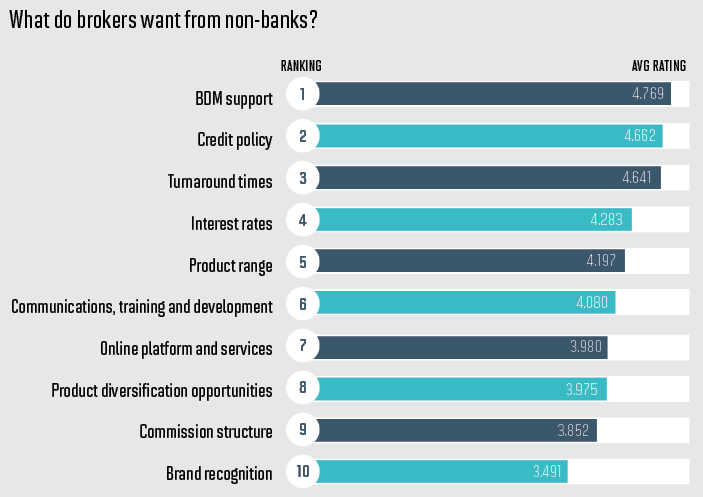

Hundreds of brokers from across Australia scored the performance of non-banks across 10 metrics, propelling the highest achievers into the winners’ circle.

This year’s data indicates that the best non-bank lenders have strengthened their ties with brokers by adapting their strategies in response to shifting third party channel and customer needs.

One broker highlighted a non-bank lender’s exceptional performance on an unconventional refinancing assessment: “Their flexibility in accepting the client’s situation and recognising that the refinance would greatly improve their financial situation was remarkable.”

Non-banks’ expanding lending prowess – rising to 16% of Australian commercial real estate debt (ACRED) from 10.4% in 2020 – is no small feat. They have capitalised on opportunities the big four may have missed and were quick to cater for underserved consumers.

“The banks have contracted their appetite for anything that doesn’t fit neatly inside a box,” says National Mortgage Brokers (nMB) managing director Gerald Foley.

“Non-banks see less volume and try to understand individual borrower needs and price risk accordingly. We’re seeing more complicated cases, especially with self-employed borrowers, that banks struggle to accommodate.”

As in years past, brokers ranked turnaround times among their top priorities, suggesting speed remains critical. There’s general satisfaction, as over half of brokers believe non-banks have improved, and a significant portion noted no change:

There was a striking shift in brokers’ expectations of non-bank lenders as BDM support and credit policy shot to the top of their priority list at first and second place, respectively, from seventh and last place in 2023.

This revelation highlights a need for proactive communication and guidance from brokers’ non-bank partners, as well as lending policies that are in tune with evolving consumer needs and market conditions.

David McQueen, Loan Market’s CEO, points out that non-banks are keenly aware of broker needs, and some of the country’s best BDMs and credit assessors work for them. Delivering on these aspects is essential to giving brokers confidence in their proposition.

“As funding has become more expensive and challenging, non-banks have tilted away from competing against the majors to increase their focus on policy and servicing niches,” McQueen says.

“Competitive pricing is important, but certainty is even more so. For example, can a lender make this loan work, and how quickly? The best non-banks can make it clear if they can do the loan and how quickly. Consistency is key, and this has never really changed.”

Brokers’ continued emphasis on interest rates, which rose in priority to fourth place from eighth last year, underscores their sensitivity to the impact of competitive pricing on their ability to help clients achieve their financing goals.

Better rates are a familiar chant among brokers. Only 6.1% listed competitive rates as a reason to pick a non-bank lender over a mainstream bank:

Lending products remain a central focus for brokers this year, who gave enthusiastic thumbs-ups for Alt Doc and Alt Doc Prime as the best non-bank products of the year from these leading lenders:

Two significant changes in brokers’ priorities are worthy of note: a sharp drop in brand recognition as a priority suggests brokers desire functional factors and practical support over brand identity; and a shift away from communications, training and development further underscores the need for more direct assistance from non-bank lenders and their representatives.

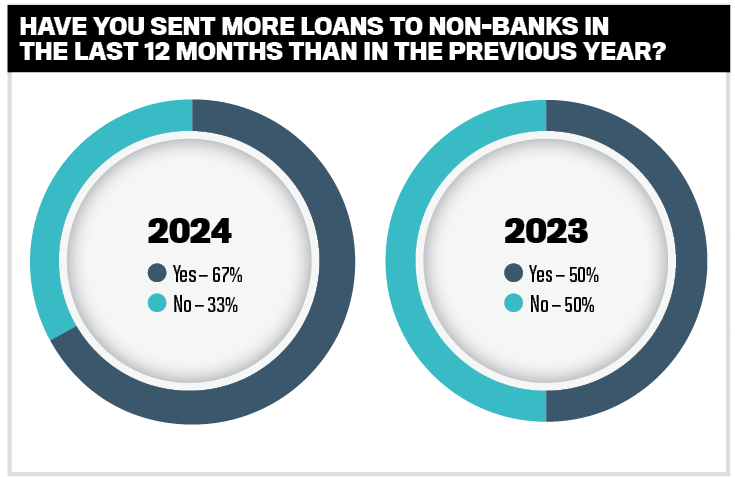

Non-banks saw a rebound in the number of broker loans put through, with brokers emphasising the need for flexibility to keep momentum going

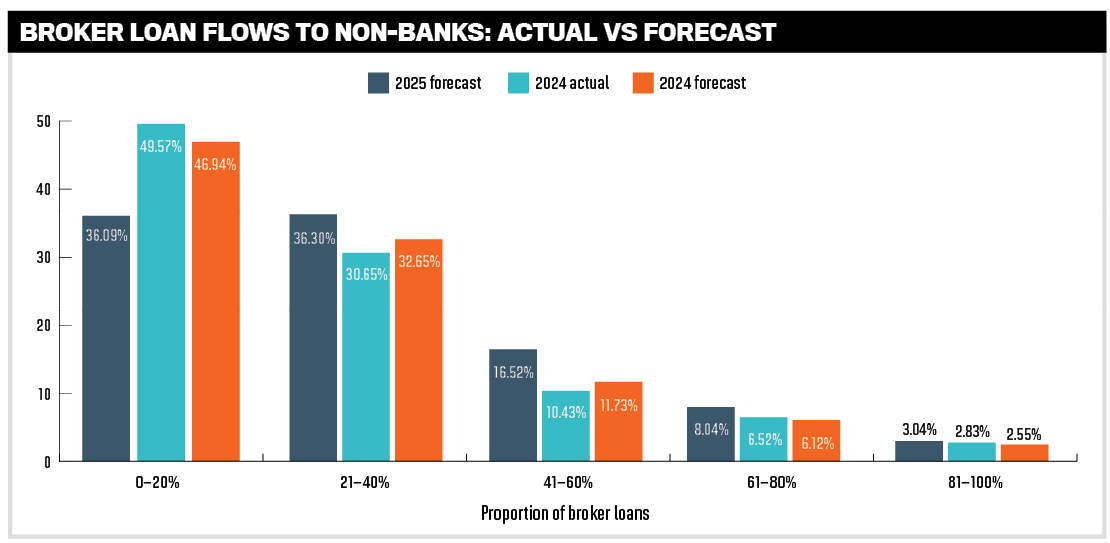

MPA’s survey showed a significant recovery this year in the proportion of brokers who put loans through non-banks to 67%, nearly catching up with 2021’s high of 69%. This follows a sustained decline beginning in 2022 and bottoming out at just 50% in 2023.

This improvement shores up the non-bank lenders’ increased market share and attests to their efforts over the past year to boost their offerings, service to brokers and competitive products.

“The non-banks seem to be looking less for cookie-cutter applications and will take the time and dedicate the resources to assess scenarios individually,” nMB’s Gerald Foley explains. “Non-banks often need to be nimble, so having the ability to identify niches and change product parameters quickly to meet these opportunities helps brokers enormously.”

The percentage of brokers putting the lowest proportion of loans (20% or less) through a non-bank declined to 50% this year, versus 60% in 2023.

At the high end of loan volume, 10% of brokers put more than 60% of their loans through non-banks than last year, showing an encouraging increase from 8% in 2023.

Non-banks have picked up market share after a period of decline, which industry experts attribute to consumer confidence during uncertain economic times, and service propositions, among other factors.

Loan Market’s David McQueen emphasises that non-banks are often faster at responding to consumer needs and less restricted by regulatory burdens.

“Non-banks do not have the same buffer and affordability issues that banks have, and this has led to an increase in non-bank volume,” he explains. “In addition, they have been better at identifying underserved customers. SMSFs and self-employed customers are excellent examples of [where non-banks] have quickly gone to market and addressed customer needs.”

The expected proportion of loans forecast to go through non-banks in 2025 is significantly lower than last year’s estimates – 36% versus 47% – suggesting that non-bank lenders may need to adapt their product and service offerings further to retain broker support and remain competitive.

While growing overall, the non-bank sector faces upcoming challenges and opportunities, including its inclusion in Australia’s Consumer Data Right open banking scheme, targeted for November 2024. ASIC is also investigating potential new regulations.

The opportunities lie in non-banks strengthening their oversight and transparency on governance and risk management, factors that will improve relationships with brokers and benefit their clients.

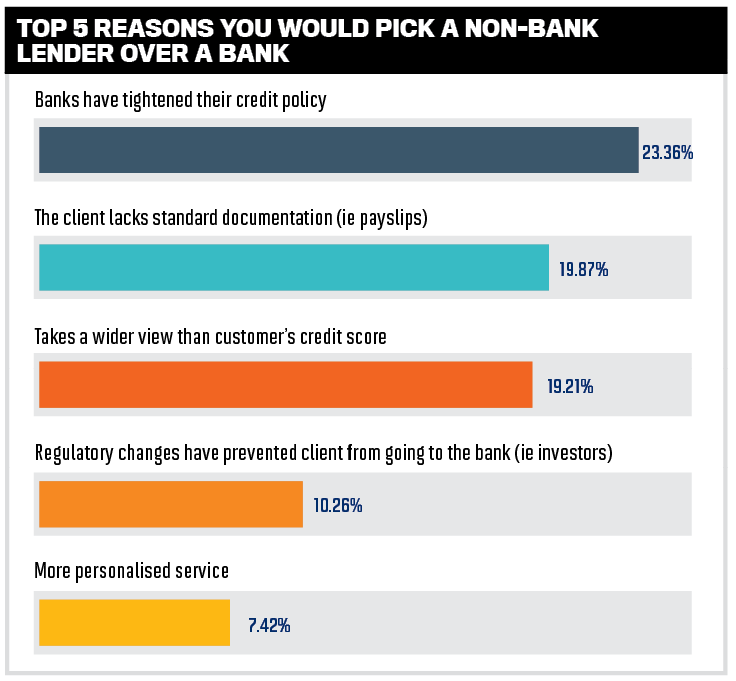

Brokers stated that non-bank lenders remain the best choice for diverse customers, particularly the self-employed. They offered the following reasons for this:

In the ranking of reasons for using a non-bank, the significant rise in clients lacking standard documentation indicates that brokers serve more clients who don’t fit the traditional borrower mould, such as freelancers, small business owners and others who struggle with mainstream bank requirements.

On the other hand, the pronounced decline – to third place from top spot last year – in non-banks taking a wider view than credit score suggests that, while this factor is still relevant, non-banks may be the first choice for clients with documentation issues rather than poor credit.

Commenting on a lender’s SMSF product, one broker highlighted “strong servicing and lower level of documentation requirements compared to other lenders”.

Although personalised service placed fifth again this year, brokers ranked it higher than in 2023, highlighting the trend towards a tailored, client-centric approach that the top non-banks are leveraging to position themselves as the friendlier alternative to the mainstream’s more rigid bank experience.

A positive shift in borrower perception towards non-bank lenders signals significant strides the sector has made in reputation and client satisfaction, offsetting concerns about brand awareness

Brokers’ ratings of the benefits of using non-banks in 2024 spotlight the growing acceptance year-over-year of non-bank lenders and their products – and illuminates the highly competitive nature of the sector. Although there is a clear runaway winner, a relatively minor point difference between the gold, silver and bronze medallists highlights the close competition among the top contenders.

The top three non-banks overall won nine golds, five silvers and three bronzes across all categories except for interest rates. That accolade went to the fourth-place winner overall, Resimac.

BDM support

Bluestone

Liberty

MA Money

Commission structure

ORDE Financial

Bluestone and MA Money

Prospa

Credit policy

Bluestone

Pepper Money

La Trobe Financial

Bluestone ended Pepper Money’s six-year streak, winning gold for BDM support as part of a strong performance overall. RedZed and Prospa earned a joint silver for turnaround times; RedZed took the bronze medal for communications, training and development; and Pepper Money won three golds for product range, product diversity opportunities and brand recognition.

Non-banks in the middle of the rankings with gold wins included ORDE Financial for commission structure.

As in previous years, the golds determined the ultimate champion, and Bluestone was crowned first place overall with a score of 4.07 out of 5. This result, and the other top lenders’ final tallies, outshone last year’s by a significant margin, a testament to the ongoing improvements brokers praised.

RedZed emerged among the top three non-bank lenders brokers wanted to see added to their aggregator panel this year, with ORDE Financial claiming first place and Liberty coming in second.

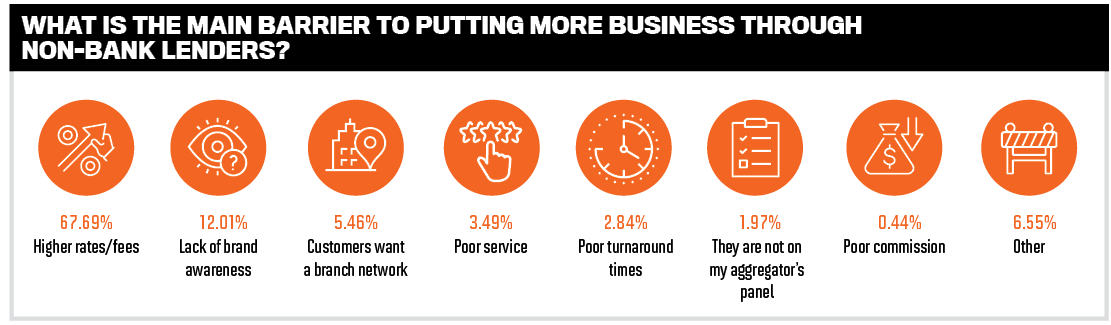

Interest rates are on one side of a double-edged sword for brokers doing business with non-banks, with 68% citing high rates and fees as the main barrier to flowing more business their way. This can send brokers and their clients to mainstream banks out of the sheer need for more affordable rates. Brokers appreciate the competitive edge non-banks bring to the market, but some have concerns:

Some brokers took a more nuanced approach to non-banks’ pricing, citing their innovative product offerings and flexibility as standout:

The second barrier to using non-banks was a lack of brand awareness, and while a consistent theme year after year, it ranked last on brokers’ importance scale in 2024. Non-bank brand awareness appears healthy, as just 12% of respondents noted it as a barrier this year, compared to 11% in 2023, 20% in 2022 and 27% in 2021.

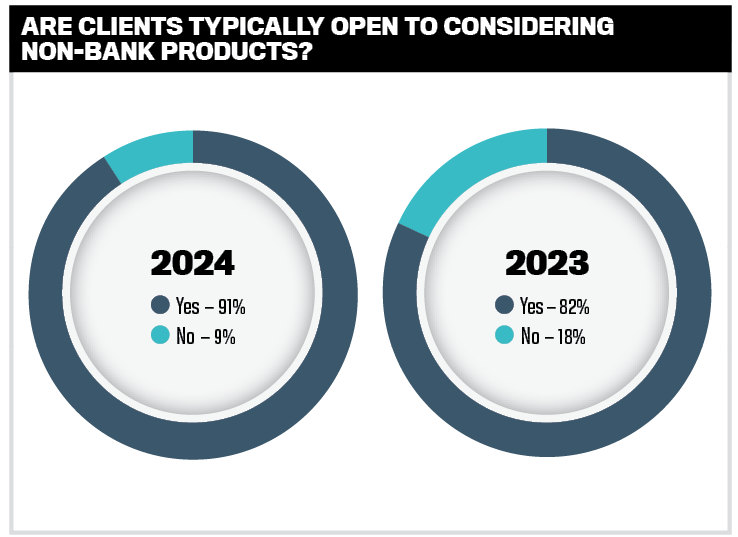

The number of brokers whose clients were typically open to considering non-bank products has dramatically reversed, rising to 91% and stemming a three-year decline. Last year, 82% expressed confidence in non-bank products, compared to a high of 90% in 2021.

Bluestone won the gold medal for credit policy as well as BDM support, underscoring its strong product and credit knowledge that brokers perceive as a frontrunner.

“Having easy access to a local credit team to back up the BDMs also helps to workshop scenarios to be confident that the answer in the discussion will match the final answer when the application is submitted,” says nMB’s Gerald Foley.

Loan Market’s David McQueen adds, “The role a BDM plays in non-bank lending is critical. Non-banks often support more complex client needs as they can explain what they can and can’t do and respond quickly and correctly on scenarios.”

The survey’s overall results show that brokers increasingly value personalised service and adaptable policies in the complex lending environment. Direct and practical support in helping them grow their businesses trumps a non-bank lender’s brand image.

Non-banks that prioritise operational efficiency while balancing leading-edge service offerings will maintain broker satisfaction.

Interest rates

Resimac

La Trobe Financial

Mortgage Ezy

Brand recognition

Pepper Money

Liberty

La Trobe Financial

Product range

Pepper Money

Bluestone

Liberty

Product diversification opportunities

Pepper Money

La Trobe Financial

Bluestone

A majority of brokers noted continued improvements in turnaround times, and there is a rising call for enhanced communication to process loans effectively

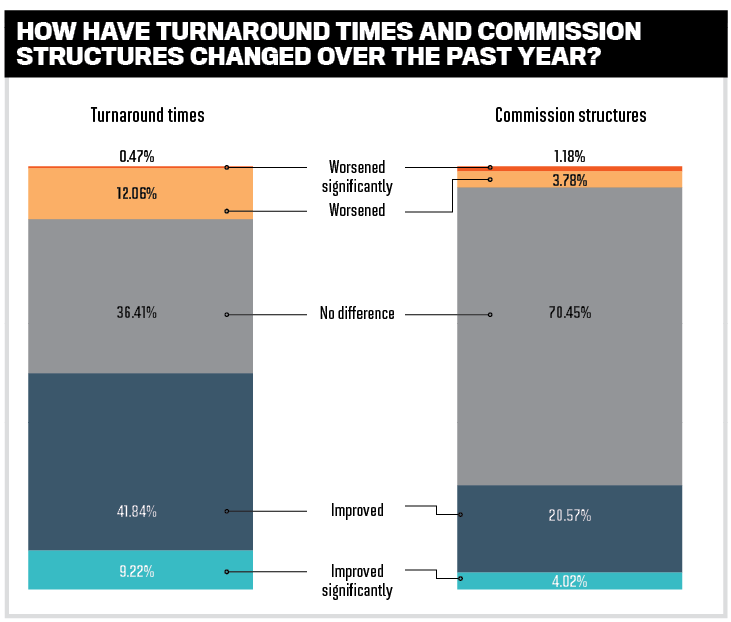

Non-bank lenders have heard brokers’ clarion call on turnaround times being crucial to making or breaking a deal. This year, a record-high majority of brokers – 87% – said turnaround times had improved or remained satisfactorily the same. Far fewer brokers than last year, 12% versus 17%, felt speed had worsened.

nMB’s Gerald Foley observes that most non-bank lenders deliver an acceptable turnaround time, making this factor much less of a differentiator than in previous years.

“Differences occur when an application needs more time to understand the transaction’s pros rather than simply finding reasons to say no,” he says. “With risk-based pricing, non-banks often have greater flexibility.”

Brokers credited enhanced support from top non-bank lenders’ BDMs in quickly executing deals, giving a general sense that more specialist lenders offer quicker turnaround times on assessments, approvals and settlements.

Non-banks have strengthened their processes, resulting in faster turnaround times, as noted by brokers:

Brokers among the small group who believed that times had worsened noted the increased complexity of some deals and lenders’ operational inefficiencies as reasons for this:

Bluestone won gold in the turnaround times category with a hefty margin above its nearest competitor. Brokers mentioned the non-bank specifically for “its BDM support”, which consistently helps speed and efficiency.

Again this year, La Trobe Financial did not rank well for turnaround times. Still, it picked up four medals, including silver for interest rates and bronze for credit policy. Brokers also named La Trobe Financial as their preferred lender for foreign non-residents and commercial categories, niches in which it dominates.

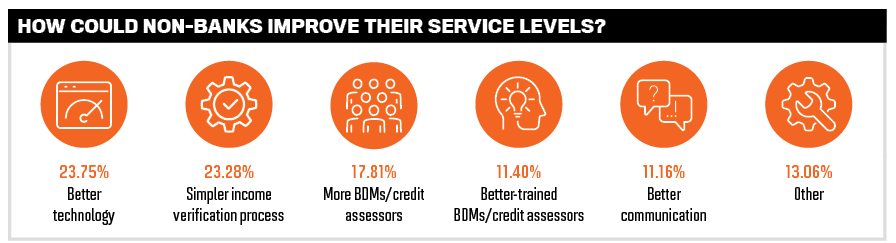

Brokers’ suggestions for how non-banks could improve their service remain consistent with last year’s. However, slightly fewer brokers said simpler income verification and better-trained BDMs and credit assessors were problematic, demonstrating the progress non-banks have made in these areas.

This year, there was a moderate rise in the number of brokers seeking better communication as a component of exceptional service. Feedback from survey respondents included:

The proportion of brokers who believed better technology could boost service levels remained consistent with 2023 at 24%, suggesting that the steady improvements non-banks had made hadn’t shifted brokers’ perceptions one way or the other.

None of this year’s top non-banks cracked four out of five marks from brokers for their online platform and services, underscoring the need to embrace new and emerging technologies to create seamless and broker-centric processes, stay at the cutting edge and increase market share.

Turnaround times

Bluestone

RedZed and Prospa

MA Money

Communications, training and development

Bluestone

Pepper Money

RedZed

Online platform and services

Bluestone

Liberty

Pepper Money

Do you think the non-banks have provided enough competition to the banks over the last year? Why/why not?

Bluestone stormed to victory in Brokers on Non-Banks 2024, with medals in eight out of 10 categories and voted as brokers’ preferred specialist lender

“With a focus on digitisation, we’re investing in new technology to improve and further streamline our approval processes and speed up decisions,” says Bluestone’s chief commercial officer, Tony MacRae. “We aim to achieve same-day, and often instant, approval for over half of the applications we receive.”

Bluestone’s winning strategy involved supporting brokers with the right people in the right roles.

The non-bank grew its BDM team by 33% and introduced a state-based leadership model with senior people on the ground. An education-first approach gave brokers access to industry-leading experts.

“This was evident in the work we did in the SMSF space, providing market-leading education on the set-up and working of SMSFs and borrowing within such structures,” MacRae says. “We aim to help brokers grow their business, ensuring they can help a broader range of customers.”

Simplifying processes and eliminating unnecessary documents underscored Bluestone’s top performance, cutting the time to unconditional approval by more than half in the last 12 months.

“Through smart technology, simplified processes, access to credit decision-makers, and BDMs focused on helping brokers grow their business, we can continue to help more brokers and their customers deliver upon their financial and homeownership goals,” MacRae says.

Specialist lending

Bluestone

First home buyers

Firstmac

Foreign non-residents

La Trobe Financial

Commercial

La Trobe Financial

Alt doc

Bluestone

SMSF

Pepper Money

Property investors

Pepper Money

In this year’s survey, brokers were asked to rank non-bank lenders across 10 categories: BDM support; brand recognition; commission structure; communications, training and development; credit policy; interest rates; online platform and services; product diversification opportunities; product range; and turnaround times. Brokers could rank the non-banks with a score out of five in each category.

Only those institutions that achieved a response rate of at least 10% of brokers for each non-bank were included in the final list.

The survey also recorded broker responses on their preferred non-banks in these areas: specialist lending; first home buyers; property investors; commercial; alt doc; SMSF; and foreign non-residents.

MPA asked the brokers a series of questions relating to their business with non-bank lenders, as well as which non-bank they would like to see added to their aggregator’s panel, but these did not influence the overall score.

MPA: What strategies or practices set Pepper Money apart in winning gold medals for product range, product diversification opportunities and brand recognition?

Barry Saoud, general manager mortgage and commercial lending:

Our strategy focuses on being the first-choice and leading non-bank, enabling our customers and brokers to succeed. We’ve achieved this through the invaluable feedback we’ve received from brokers and customers, and we’re extremely gratified by the positive reception we have consistently received from brokers and our aggregator partners.

Adapting to the ever-changing market landscape demands agility, innovative product offerings and a deep understanding of each customer’s unique situation. This is precisely why, throughout our 23-year history, we have continuously refined and enhanced our products and processes at Pepper Money.

However, our emphasis on diversification of credit policy, industry-leading technology and effective BDM support has enabled us to provide brokers with the necessary tools and knowledge to help a greater number of customers succeed.

Pepper Money’s success is firmly rooted in our robust credit policy. We take the time to understand our customers’ evolving needs and circumstances, offering diverse products and policy options.

Our bespoke Cascading Credit Model and our purpose-built technology aim to streamline and automate the broker and customer experience. The Pepper Product Selector (PPS) allows a single application to be tested against multiple solutions within minutes.

We’ve further automated our credit assessment processes, streamlined our accreditation experience and activated application status updates pushed to brokers via SMS.

We are known for our industry-leading turnaround times. Our efficiency is a result of our adoption of innovative technology and automation. Our commitment to market-leading response times reflects our dedication to providing exceptional service to our brokers.

We understand that providing a swift and appropriate credit decision is crucial for brokers. This consistency enables brokers to confidently recommend us as a lender, knowing their clients will receive a prompt and suitable outcome.

Our consistency and transparency of decisions provide brokers and customers with greater confidence in determining whether the customer will (or will not) be approved. When you engage with Pepper Money, whether for a home, commercial, construction or SMSF loan, you can expect a higher likelihood of conversion due to our credit policies. This means brokers can make the most efficient use of their customers’ time and maximise their time by ensuring the deal goes through.

The product and credit knowledge of Pepper Money’s BDMs to best inform and support brokers to serve the diverse needs of their clients is backed by a locally based customer service team, which supports customers not just through the application but over the life of their journey with us.

We’ve built strong alliances with our brokers, who trust our brand implicitly. We’re proud to have earned this trust over more than two decades. Our transparency is key to this trust; brokers rely on Pepper Money to get the deal done.

MPA: Given your impressive achievements, how do you plan to build on this momentum to drive even greater success?

BS: Pepper Money never stands still, and that’s true in our approach to evolving our offering to move with the market. Continuous innovation and enhancement of our product offerings and policies are at the heart of our operations.

Across the past 12 months, we’ve introduced new loan products and policy enhancements tailored to meet the needs of evolving market segments or emerging trends.

Just as we do with our residential products, we also provide a near prime option for our commercial and SMSF offerings. This ensures we don’t limit our customers to only the prime category. We continue to implement a real-life approach to our products, considering the complexities of real-world financial situations across these varied asset types.

Our customer-centric policy enhancements provide greater accessibility and flexibility, particularly for underserved segments and those with non-traditional income sources. These initiatives underscore Pepper Money’s dedication to driving growth, market leadership and exceptional customer service.

We most recently introduced a series of policy changes designed to empower brokers to meet the unique needs of their clients, particularly those who are self-employed. The policy enhancements across prime, near prime and specialist options include reduced income verification, increased loan amounts and LVR limits, vacant land options and servicing calculator changes.

These product launches and improvements reflect Pepper Money’s commitment to adapting to the evolving financial landscape and providing tailored solutions to help brokers meet their clients’ unique needs.

MPA: RedZed achieved a tie for silver in turnaround times, a top-ranked broker priority, and a bronze in communications, training and development. What are the factors driving your high performance in these categories?

Calvin Cordle, managing director:

A great user experience and fast turnaround times have always been core to RedZed. In FY24, one of our key focuses was further improving operational efficiencies to deliver even better experiences.

We set about measuring key touchpoints, such as assessment turnaround times and the time it takes our teams to answer calls and emails, to track our progress and identify areas for improvement. This has helped take our service levels to new heights, and we’re thrilled that brokers have noticed and are enjoying the RedZed experience.

We’ve also been focused on developing educational resources to help brokers learn, grow and liberate the ambitions of their self-employed customers. Last September, we launched our Self-Employed Broker Academy, an online library of learning modules designed to help brokers tap into the self-employed market and better service their clients. This resource is free for all RedZed accredited brokers and aims to drive business growth for brokers while improving customer experiences.

The professional and personal development of brokers is also something we’re passionate about, and we regularly host PD sessions for brokers through our partnerships with the Melbourne Storm, Hobart Hurricanes and the North Melbourne Football Club.

Earlier this year, we held our Train Like a Roo event, which saw brokers go behind the scenes at North Melbourne and experience a training session with players and coaches.

Last month, we invited brokers to attend our RedZed x Storm Leadership Day, where they put their touch rugby skills to the test at AAMI Park. They also gained insights from Melbourne Storm players and coaches on leadership, innovation and building a winning culture.

Exceptional customer service, innovative educational resources and unique experiences are just some of the ways we support the third party distribution channel, a partnership we deeply value.

MPA: How do you plan to capitalise on your success and reach new heights?

CC: First, I want the RedZed team to pause and celebrate. This is great recognition of all the hard work over the last year, and my congratulations go to all RedZedders. I know that this will motivate the team to push on from here and renew our focus on our next set of strategic objectives. These results are proof that we’re on the right track.

The enhancements we’re making to our product and service offerings resonate with brokers and, by extension, Australian self-employed small business owners. The best part is that we’re only just getting started!

MPA: Resimac earned gold for its competitive interest rates, setting it apart in the market. What key approaches and strategies drive this standout performance?

Chris Paterson, general manager distribution and marketing:

Resimac is proud to have received this result and be recognised by brokers for our competitive interest rates. When it comes to recommending a lender to their customers, we know that competitive interest rates are a key consideration for brokers, forming an important part of the broader offering we provide.

We have a considered and targeted approach to pricing to ensure our rates are competitive for customer segments like self-employed or investor borrowers. By deeply understanding these customers, we can often provide options that other lenders may be unable to.

So many people are struggling with the pressure of higher living costs, and we want to play our part in helping them achieve their financial goals. Our talented BDMs work closely with brokers to workshop applications, investing the time to develop relevant and competitive customer solutions.

Here at Resimac, we’re always looking for more ways to say yes, and our competitive interest rates are one of the key success factors that can help us do just that.

MPA: How do you plan to leverage your current success and position Resimac for continued industry leadership?

CP: We are grateful to be recognised by brokers with whom we enjoy working every day. Our team is dedicated to the broker channel, and it’s great to hear we’re on the right track.

Brokers know Resimac as a flexible specialist lender. We’re often recognised for our tailored solutions for self-employed and credit-impaired borrowers. Our BDMs pride themselves on building genuine relationships with brokers; they have a great attitude and extensive industry experience.

There’s still plenty we want to focus on to be the non-bank lender of choice for brokers, and we can’t do that without critical feedback from brokers. We continually leverage insights from sources like Brokers on Non-Banks and our research to guide our focus and improve broker and customer experiences.

Some exciting work is underway to continually improve process consistency and decision-making speed while maintaining our flexible and agile approach. We’re also enhancing our digital solutions with more self-service options for brokers and customers to improve their experience.