Record loan originations as market share grows

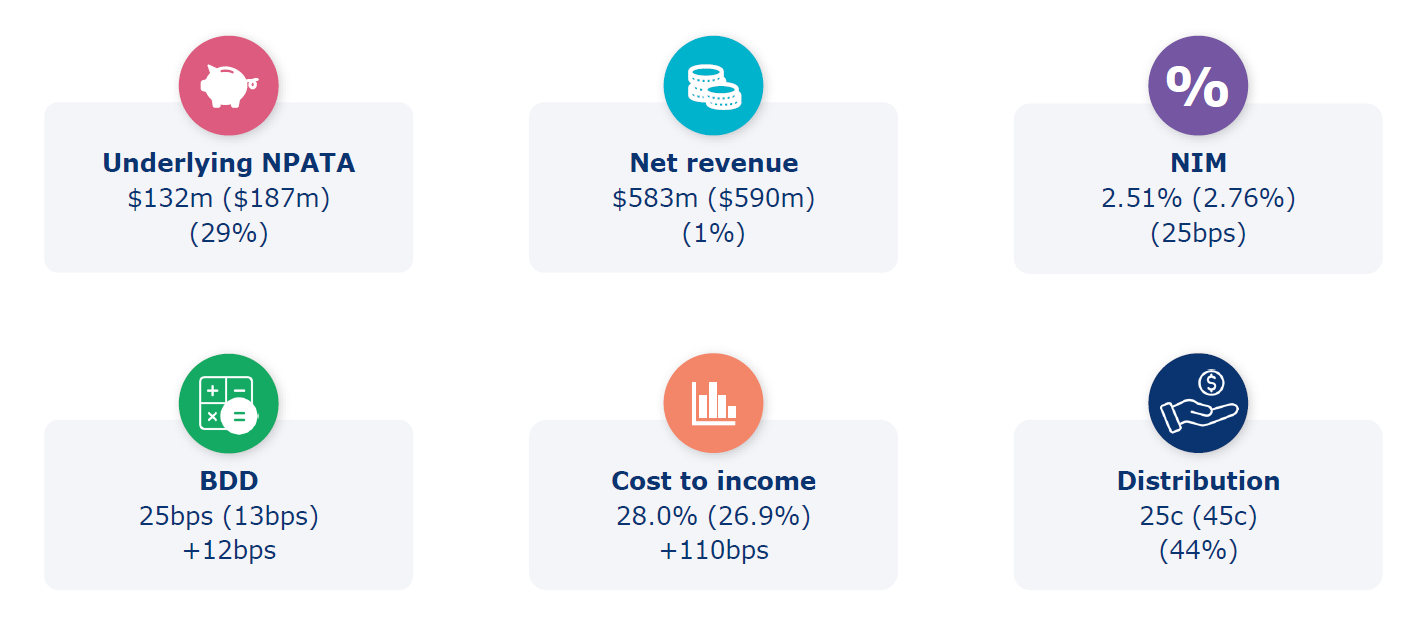

Liberty Financial Group says it has achieved record new loan originations in the 2024 financial year, increased its financial assets and kept loan losses low, while also experiencing a 29% drop in underlying net profit after tax to $132 million and a 25-basis point fall in net interest margin.

Liberty today (Monday, August 26) released its financial results for the year ended June 30, 2024, to the Australian Stock Exchange.

The non-bank lender’s CEO, James Boyle (pictured above left), said the reduction in underlying NPATA reflected the impact of trading through economic uncertainty and elevated competitive activity.

“Importantly during this time we have managed to help more customers, increase our financial assets, improve our team’s efficiency and our loan losses remain low,” Boyle said in a media release.

While Liberty’s NIM for FY24 was 2.51%, down from 2.76% in FY23, the figure continued to be industry leading compared to banks and other non-banks and it was anticipated to stabilise in the future.

Liberty FY24 financial highlights

Source: Liberty Financial Group FY24 Full Year Results, 26 August 2024

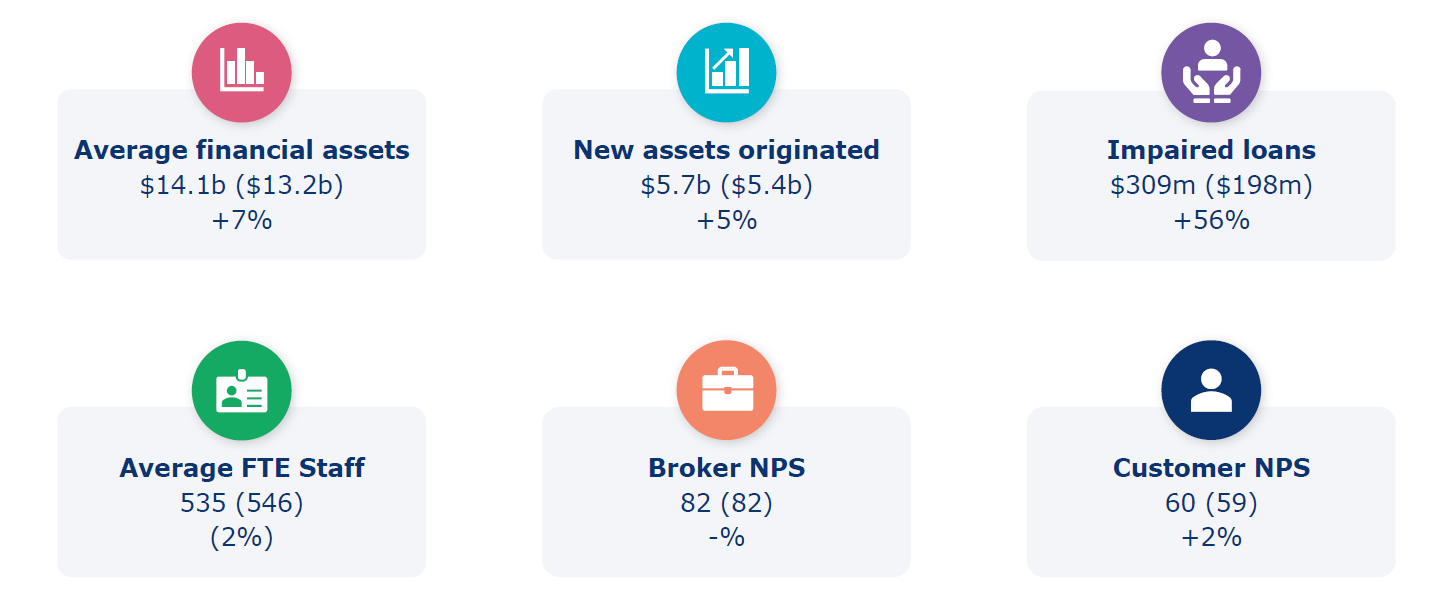

According to Liberty’s full-year results presentation, financial assets were up 8% to $14.6 billion in FY24, while the Group enjoyed record FY24 loan originations, totalling $5.7bn, up 4% from FY23.

Liberty chief financial officer Peter Riedel (pictured above right) said Liberty’s capital and liquidity position continued to be in a strong position to support customer growth.

“LFG raised $5.6 billion in funding in the 12 months to 30 June 2024 and Standard and Poor’s upgraded Liberty’s investment grade corporate rating to BBB (stable outlook),” Riedel said.

He also pointed to Liberty’s underlying cash return on equity of 11%, while maintaining a low leverage ratio of 13.2.

“Our market-leading net interest margin of 2.51% and return on equity results are a further demonstration of LFG’s focus on building durable business values across the banking and finance landscape,” said Riedel.’

Liberty announced a final unfranked actual distribution of 13c per Security. The FY24 distribution of 25c implies a yield of 7% (based on June 28, 2024, security price of $3.76

Liberty FY24 operating highlights

Source: Liberty Financial Group FY24 Full Year Results, 26 August 2024

Liberty’s record loan originations

While loan originations for the Group rose from $5.4bn to $5.7bn in total in FY24, the Financial Services section of LFG proved particularly strong, with a record $535m in originations, up 35% from FY24, driven by market share gain from other non-banks.

Financial Services includes personal loans offered by MoneyPlace; SME loans (Liberty); life insurance distribution (ALI Group) and broking services offered by Liberty Network Services.

Liberty’s Secured Finance, which includes motor vehicle loans and commercial finance (secured commercial property mortgages to SMEs and SMSFS for working capital, owner occupier loans and investment loans), was also up 5% to $2.1bn on FY23, while FY24 residential originations remained consistent with FY23 at $3bn.

Boyle said having achieved record new loan originations across existing and new businesses, along with an anticipated stabilising net interest margin, “we are optimistic about the opportunities the coming periods will present and will continue to invest in the business to generate future value”.

Other Liberty FY24 results

Among the other highlights revealed in Liberty Financial Group’s FY24 highlights were:

- Total revenue growth up 15% (2H24 vs 2H23) and up 3% (2H24 vs 1H24)

- Net revenue – up 1% (2H24 vs 2H23) due to higher net interest income and lending income partly offset by lower commission income

- Net revenue – down 1% (2H24 vs 1h24) driven by lower net interest income and stable lending and commission income

- Increase in impaired loan impairment of 11 bps in 2H23 to 13bps in 2H24

- Average asset growth 7% (2H24 vs 2H23) and 4% (2H24 vs 1H24) driven by Secured and Financial Services segments

What do you think of Liberty’s FY24 results? Comment below