Helia is repositioning LMI as an enabler that empowers home buyers to enter the market sooner

This article was produced in partnership with Helia

The Paradigm shift

In an ever-evolving landscape of mortgage lending, one thing that is constant is change. Over the years, mortgage brokers have witnessed the transformation of the industry including regulatory frameworks, changing market dynamic with a rising property market and interest rate environment along with higher customer expectations.

Today, mortgage brokers play a crucial role in helping home buyers enter the property market, but rising house prices make saving a 20% deposit challenging. To overcome this, home buyers explore alternative pathways like Lenders Mortgage Insurance (LMI) to achieve home ownership sooner.

Why LMI?

The traditional view that LMI is a necessary burden is shifting. LMI is being repositioned as an enabler, a turn-key that empowers home buyers to enter the market sooner.

According to Helia Spotlight 20241, more first home buyers are using LMI to buy a property with 55% of first home buyers using LMI to buy their first property (increase from 36% in 2023). LMI awareness is also on the rise with 65% of first home buyers aware of LMI (increase from 56% in 2023).

Greg McAweeney, Chief Commercial Officer at Helia, commented: “Changes in the property market such as fluctuations in property prices, interest rates and housing supply can impact the demand for LMI.”

Despite the advantages LMI can provide, concerns and misconceptions endure. Helia found that even for those who have heard of LMI, only 38% accurately identified LMI as an insurance to protect the lender and that it allows the buyer to purchase a property with less than a 20% deposit (decrease from 52% in 2023).

Rethinking education

Helia is focused on bringing educational resources and tools to life for mortgage brokers to support more confident conversations with their clients.

Educate, empower with video: Education is vital to help more clients understand the value and benefits of LMI. By demystifying LMI, mortgage brokers can help home buyers access home ownership with a smaller deposit. This can be particularly beneficial for first time buyers or those with limited savings and positions LMI as key to making home ownership more accessible.

Helia has developed a series of educational resources to help reframe LMI to home buyers including a new video.

Titled “Better, Sooner, Brighter”, the video features two couples, armed with the same deposit amount and seeking homes in the same area. One couple secures a better, larger home with a smaller deposit, by paying for LMI, while the other couple buys a smaller property with their 20% deposit, unaware of the option of LMI.

Fast-forward 4 years, and both homes have risen in value (based on a desktop valuation), but the bigger home saw a larger dollar increase, larger than the initial LMI fee paid. This video illustrates how a well-informed decision by home buyers, guided by a trusted mortgage broker, can significantly impact their home ownership journey.

Educate, engage with data: One of the most common questions posed to mortgage brokers by aspiring home owners is “should I wait and save or buy now?”

In places where property prices increase more rapidly than home buyers can save a deposit, home buyers may be better off buying their home sooner with a smaller deposit if they pay for the LMI premium, rather than waiting to save a larger deposit.

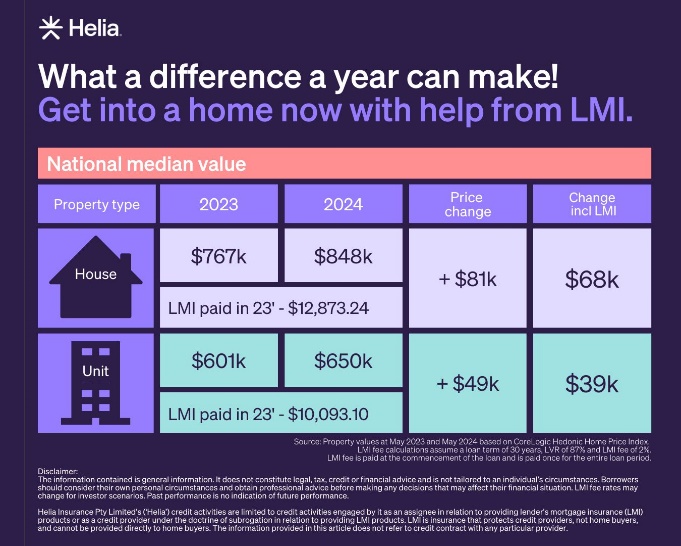

Helia is supporting mortgage brokers to have these discussions by crunching the numbers and enabling data driven discussions to confidently position LMI. Our ‘What a difference a year can make’ is about showcasing year on year national median house and unit prices and LMI.

Educate, enable with translated resources: Australia is home to many languages and cultures, with the 2021 Census data finding over 22% of the population speak a language other than English at home. In response Helia has translated LMI factsheets and infographics into Punjabi, Arabic and Simplified Chinese.

McAweeney explains: “Entering the property market can be challenging enough, without the added complexity of a language barrier thrown into the equation. At Helia, we want to ensure that every person, no matter their background, understands their options when it comes to buying their dream home. Our translated resources are just one of the many ways we’re looking to do that.”

Mortgage brokers should leverage educational resources to elevate conversations about LMI, boost client confidence in making informed decisions and expedite their journey to home ownership.

Helia Spotlight -July 20241 – based on research commissioned by Helia and conducted by CoreData on 1015 home buyers (608 prospective home buyers and 407 recent home buyers).

Disclaimer:

The information in the article is general information. It does not constitute legal, tax, credit or financial advice and is not tailored to an individual's circumstances. Home buyers should consider their own personal circumstances and obtain professional advice before making any decisions that may impact their financial situation. The ‘What a difference a year can make’ example assumes a rising property market, and that the outcome may differ in a falling property market.

Helia Insurance Pty Limited's ('Helia') credit activities are limited to credit activities engaged by it as an assignee in relation to providing lender's mortgage insurance (LMI) products or as a credit provider under the doctrine of subrogation in relation to providing LMI products. LMI is insurance that protects credit providers, not home buyers, and cannot be provided directly to home buyers. The information provided in the video and this article does not refer to a credit contract with any particular credit provider.

About Helia

Helia is Australia’s leading LMI provider. Our purpose is to work with our customers to help home buyers achieve their dream of home ownership sooner and so be able to accelerate their financial wellbeing through home ownership.

In 2023, we helped over 42,000 home buyers into homes sooner, as well as assisting with over 9,000 hardship requests to enable home buyers to stay in their homes when they faced difficulties.