Brokers will make or break upstart's success

Has there been an erosion of fairness in the Australian property market? It is hardly a hot take to say absolutely, unequivocally, yes.

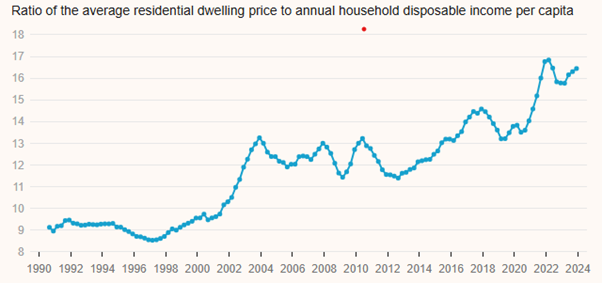

Take any graph of average income levels, stack it up against house prices, and you’ll see why so many younger Australians are finding it nearly impossible to get so much as a toenail on the property ladder.

One such graph (below) reveals that the average house cost nine times the average salary in 1990. That ratio shot past 16-times the average salary in 2021 and has stuck there ever since.

Graph credit: The Guardian

While government schemes like First Home Buyers Assistance have alleviated some of the pressure on homebuyers, these schemes are looking increasingly out of sync with the ever-rising price of the average home.

Sprinkle in exceptionally high assessment criteria and it paints a glum picture.

It is in this challenging environment that Mario Emmanuel (pictured, centre) co-founded Sucasa, a non-bank lender which promises low rates, low upfront fees and no LMI.

What’s the catch?

Starting from 6.05%, Sucasa’s rates are indeed competitive, while LVRs as high as 98% are on the cards.

Anyone with half a brain would ask: What’s the catch? Coming to market with an eye-catchingly good offering, at high LVRs, without LMI naturally begs the question: Can it be true?

The classic Uber model of “come to market with a lossmaker, steal a huge chunk of the market, then jack your fees up” sprang to this reporter’s mind.

Emmanuel baulked at the prospect when discussing Sucasa with MPA. “We've got serious funders that are behind us, and they're all looking for us to build a model that's sustainable,” he said. “There's nothing that's loss-leading about our product.”

While it is true that Sucasa does not charge LMI, it does charge a risk fee, which Emmanuel contends is cheaper for the customer. His contention is not without justification – risk fees are commonplace among alternative lenders, while Mortgage Choice states that they can indeed be lower than LMI.

“Whether it's an insurance policy or interest rate or fees, a lender’s job is to get an adequate return for the risk that you're taking,” Emmanuel said of Sucasa’s business structure.

“We're trying to give great loans to great borrowers,” he said. Often, these great borrowers are relatively affluent professionals that don’t have the bank of mum and dad at their disposal, but do have a large capital base.

They’re looking to buy a house within their income bracket, but don’t have a spare $200,000 kicking around to make it happen.

It may sound altruistic, giving cheap loans to deserving people, but it is as much a business strategy as anything else. Emmanuel believes this is where the gap in the market lies for Sucasa to squeeze itself into.

He criticised the banking majors for prioritising “high-throughput” lending products that leave deserving homeowners by the wayside.

“The opportunity for people who are willing to think outside of the box and offer products to people who desperately need them is there,” he said.

Make or break

It is clear that Emmanuel didn’t just pluck the idea for Sucasa out of thin air.

A first-generation migrant with a background in investment banking, he loves Australia’s culture of upward mobility, the ability for its citizens to make something of themselves no matter where they come from.

But he has also seen that culture “sort of get chipped away” over the past 15 years as Australians find it harder and harder to get a set of house keys in their hands.

“So how do we achieve the objective of leveling this playing ground?” Emmanuel said. “That has to be our objective, and so that's kind of the mindset that we take to every product that we create, and every decision that we make.”

Undoubtedly, he wouldn’t mind earning a pretty penny along the way.

It is early days. Sucasa is not on any lender panels, meaning the vast majority of distribution is selling direct to customers, plus a handful of strategic accredited brokerages.

That is a limited market that won’t yield the growth Emmanuel clearly wants. This cold fact led him to bring David Ewens (pictured, left) in as head of distribution last month. Paul Coloe (pictured, right) was concurrently brought in as head of credit and underwriting.

Ewens’ CV includes sales and management roles at Bankwest, Mortgage Choice and BOQ. His mandate is to sell Sucasa to brokers and aggregators.

So far, “we’ve had extremely positive discussions” with brokers and aggregators, said Emmanuel. “We are really comfortable that our product has a place in this market and that there is serious value to be given to a whole bunch of really great Australian borrowers by us getting this product into their hands, and so the next challenge for us is getting that distribution out there.”

Sure, Sucasa may have winning rates, but its success rests on convincing Australia’s brokers that it is the right fit for homeowners.