Savings, low unemployment, spending cutbacks all contribute

The level of arrears in the Australian residential mortgage-backed securities sector continues to remain low due to savings buffers, refinancing, borrowers cutting back on spending, and low levels of unemployment, according to the latest data from S&P Global Ratings.

The credit rating company’s RMBS Performance Watch: Australia Market Overview for Q1 2024 revealed that low mortgage arrears, albeit rising, were underpinned by low unemployment, savings buffers (for some), and refinancing opportunities.

The report also said borrowers also have been prudent in curtailing expenditures to service their debts, prioritising debt commitments over discretionary spending while interest rates remain high.

Wage rises were also highlighted in the S&P Global Ratings RMBS report as helping mortgage holders to cope with higher mortgage servicing costs, while federal government tax cuts to be applied from July would also help ease future debt serviceability burdens.

“The household savings ratio has been bolstered, modestly, by these factors rising to 3.2% in Q4 from 1.9% in Q3,” the report stated. “Despite the recent uptick, household savings are still well below their pandemic peaks of 24%.”

Unemployment was also predicted to rise, but forecast increases remain below pre-pandemic levels, S&P Global Ratings said.

“Higher unemployment will flow through to higher arrears. But as long as unemployment remains low overall, we don't expect these increases to be material.

“Property price growth also affords existing homeowners greater agency in self-managing their way out of any financial stress.”

Data as of March 2024. Source: S&P Global Ratings

Data as of March 2024. Source: S&P Global Ratings

Key RMBS arrears report observations

S&P Global Ratings director structured finance Erin Kitson (pictured above) said the arrears report covered residential mortgage backed securities.

These are bonds underpinned by residential mortgage pools, and the data represents about 10% to 12% of Australia’s total mortgage market, including loans provided by both banks and non-banks.

Prime arrears

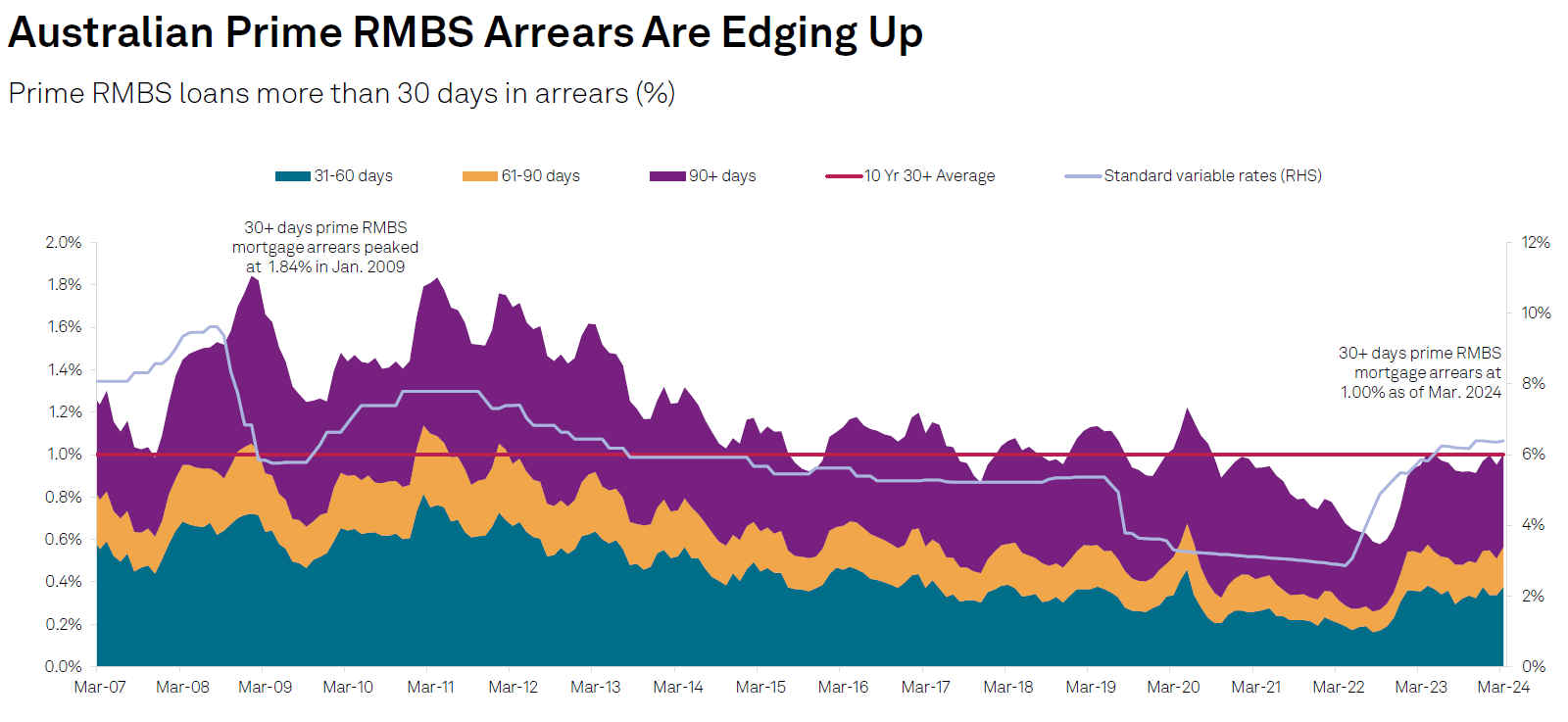

As of March 2024, prime RMBS arrear were at 1%, up from 0.95% a year earlier and a historic low of 0.58%.

“We expect upward pressure on arrears as the unemployment rate rises. Arrears increases are likely to be modest, though, because unemployment is forecast to remain low overall,” S&P Global Ratings said.

Prime RMBS arrears exclude noncapital market issuance transactions. Standard variable rates are based on outstanding mortgages. Sources: Reserve Bank of Australia, S&P Global Ratings

Non-conforming arrears

Non-conforming arrears involve a smaller set of loans, typically offered by non-bank lenders and are often larger, more highly leveraged loans taken out by self-employed borrowers.

Arrears in this sector hit 4.18% in Q1, up from 4.02% in Q4. S&P Global Ratings predicted non-conforming arrears would continue to grow faster than prime arrears, given the sector’s greater sensitivity to weaker economic conditions, but property price growth would help to minimise losses.

Investor versus owner-occupier prime arrears

The report revealed investor arrears were at 0.77% in Q1 compared with 1.12% for owner-occupiers.

“While we expect both investor and owner-occupier arrears to increase, investor arrears increases are likely to be buffeted by higher rentals to some extent.”

Why mortgage holders have remained resilient

Kitson said the data showed that mortgage arrears remained low overall.

“They have been increasing though, and that's not surprising given you've had consecutive rises in interest rates and a lot of mortgages in Australia are variable rate mortgages,” Kitson said.

There were a number of reasons for household resilience despite the significant increases in mortgage repayments.

“Unemployment, which causes loss of income, is a key cause of mortgage default. Unemployment has remained low at 4%.

“Other factors that are underpinning that resilience is those borrowers who have been able to save and build buffers. We saw that during the pandemic, the household savings ratio reached very high levels around 25%.

“Now that has come down quite a lot, as households have faced a lot more debt serviceability pressures, but those savings buffers clearly put a number of borrowers in a good position going into this rate rising cycle, being able to draw on those to help stay on top of mortgage repayments.”

Kitson said strong mortgage refinancing activity, which is now tapering off, had also helped to keep mortgage arrears low.

There had previously been intense competition among the big banks with cashback offers to attract borrowers to refinance their home loans.

“So that provided some debt serviceability easing as well because for borrowers that had a high rate, they could if they were reasonably good credit go and shop around for a better rate.

Kitson said mortgage-holders were also curtailing expenses, with discretionary consumer spending such as eating out, travel and gym memberships, falling significantly.

“You would expect in a rising interest rate or weakening economic environment for households to prioritise what they have to spend and clearly mortgage repayments are going to be a non-discretionary expense that will be prioritised over many other items.”

Improved property prices had also aided borrowers’ resilience.

“Following the interest rates kicking off back in 2022 property prices experienced a fairly short, sharp decline, but then they turned around.”

Now that property prices had improved, Kitson said borrowers who were feeling financially stretched, particularly those with an owner occupied mortgage and an investor mortgage, had an option to get out of arrears or avoid going into arrears, by selling their higher equity property without realising a loss.

Stubbornly high inflation

The latest consumer price index (CPI) figures for April 2024, show that inflation rose 3.6% in the 12 months to April, according to the Australian Bureau of Statistics, up from 3.5% in March

“Persistently higher inflation impacts households in a couple of different ways,” Kitson said. “Clearly for households, things are still more expensive and that adds constraints to household budgets.”

When it came to mortgage arrears, Kitson said higher inflation created challenges for central banks when it came to reducing the official cash rate and relieving mortgage stress.

“Will interest rates need to linger at these higher levels if inflation remains persistent and stubbornly high. The implication there is what does that mean for interest rates and mortgage repayment costs?”

Future arrears trends

Kitson said S&P Global Ratings was forecasting arrears to continue to increase “particularly as we're forecasting unemployment to increase to 4.4% this year”.

“Unemployment is particularly low in a historical context of where unemployment levels have sat,” Kitson said.

“Provided unemployment remains low overall, we’re expecting arrears to tick up but those increases to be relatively modest and not likely to cause any material dislocation in mortgage markets or property markets.”

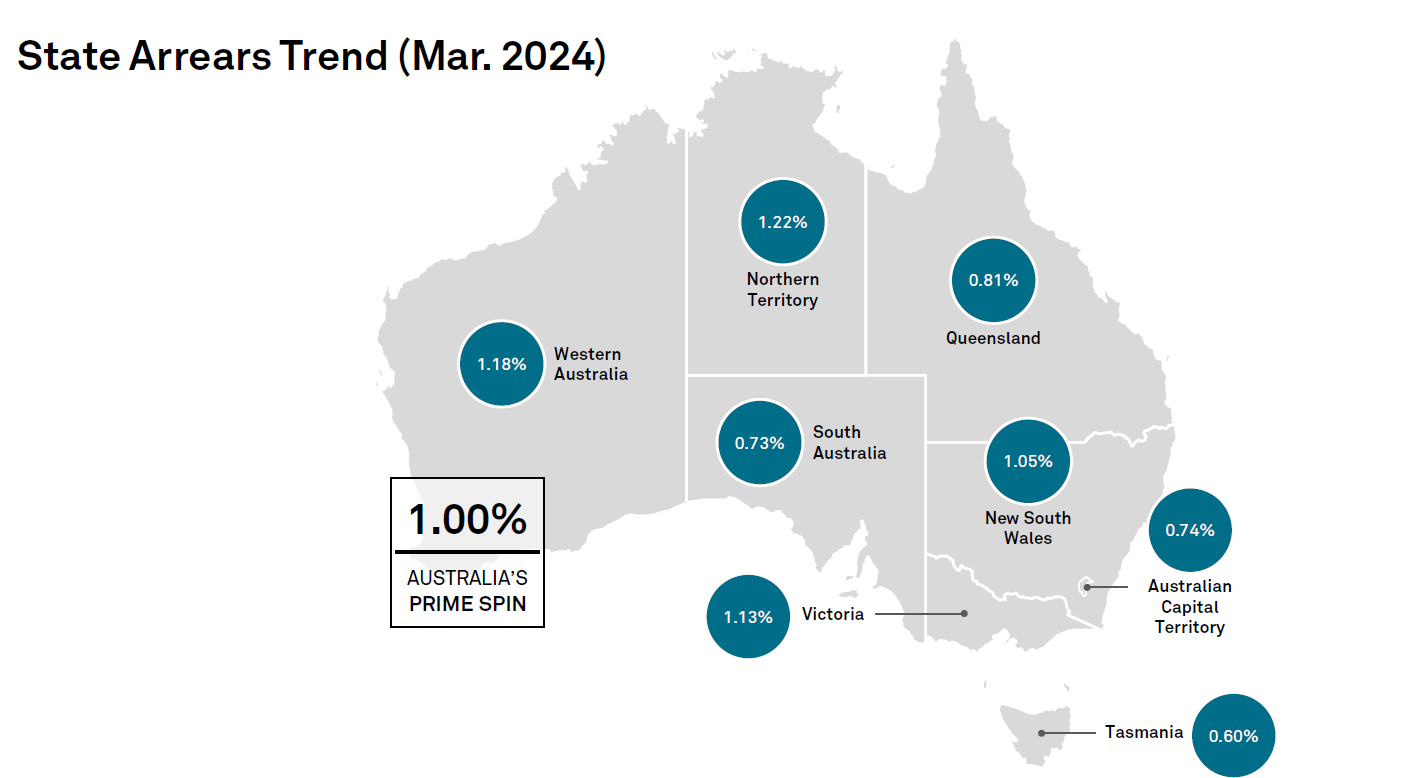

Data as of March 2024 based on prime RMBS loans (excluding non-capital market issuance) Source: S&P Global Ratings

As a broker, is there a low level of mortgage arrears among your clients, and if so, why? Comment below