Aggregators roundtable discusses market share, serviceability, payroll tax and more

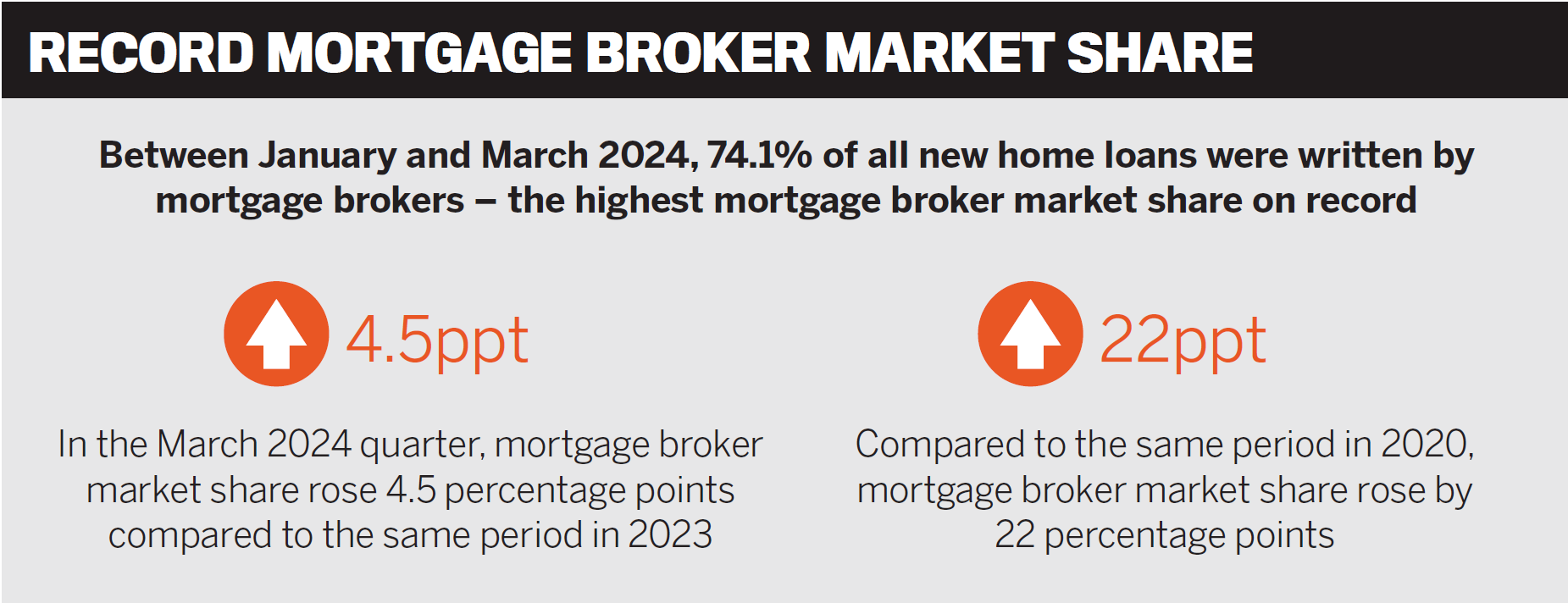

The mortgage broking industry is enjoying unprecedented levels of support from the Australian public. The latest MFAA figures show that in the March 2024 quarter, 74.1% of all new home loans were written by mortgage brokers – a record figure, which has surpassed the previous record of 71.8% for the October to December 2023 quarter.

Australians are increasingly placing their faith in the skills and knowledge of brokers to help them buy their first home, refinance for a better deal or purchase an investment property.

But that doesn’t mean everything is rosy in the world of broking. Five increases to the Reserve Bank’s official cash rate since the beginning of 2023 and a higher cost of living mean reduced borrowing capacity, with some people unable to refinance due to serviceability constraints.

Brokers are working harder than ever for customers in a competitive market, and the level of refinancing has fallen since the peak about 12 months ago, with fewer lenders offering cashbacks.

This means diversification into areas such as commercial and asset fi nance will become increasingly important for brokers as they look to cover all their clients’ finance needs.

The issue of payroll tax also looms large after the NSW Supreme Court found that LMG was liable for payroll tax, albeit with exemptions, with ramifi cations for the way brokerages are structured and operate.

New technology and ongoing training are necessary to ensure brokers can continue to serve their customers well and grow their businesses. The support of aggregators remains crucial as brokers navigate both the challenges and opportunities of the market in 2024.

MPA invited leading aggregators to join its annual roundtable at Sydney’s Nobu restaurant. Attending the event were Blake Buchanan, general manager, SFG; Brad Cramb, chief distribution officer, Lendi Group; Gerald Foley, managing director, nMB; Them Lam, head of sales and distribution, AFG; Daniel Marsi, CEO, Liberty Network Services; Tanya Sale, CEO, outsource Financial; Aaron Slater, general manager distribution, REA Group (Mortgage Choice), and Sam White, executive chairman, LMG.

Two brokers also attended: Kristie Gould, franchisee, Mortgage Choice Warners Bay, and Adriana King, principal finance broker, Expand Equity.

Q: How have aggregators worked closely alongside their broker members to support them and their customers in a challenging lending environment?

There have been a variety of challenges for mortgage brokers over the last 12 months, with fewer customers borrowing for property purchases and refinances dropping, while interest rate rises and infl ation have affected borrowing capacity and serviceability, with borrowers rolling off low fixed rate loans onto much higher rates.

The aggregators said serviceability was one of the biggest challenges, but all shared a sense of optimism about the future, with a focus on supporting brokers through 2024 to adapt to a changing market.

Sale (pictured below) said the challenges hadn’t just been interest rate rises or lender policies.

“I think it’s about the brokers getting guidance and education on sticking close to the consumer,” she said. “I think that’s been the challenge all the way through the turmoil with these interest rate rises.

“I think the lending’s going well. There’s now more competition outside of the majors, which I feel brings some balance within our industry.”

Sale said the industry had to stop giving such a large percentage of loan business to the major banks.

“The non-majors and other lenders have got to step up so we have a very vibrant, dynamic and competitive industry.”

White said, from LMG’s perspective, loan serviceability had been one of the biggest challenges for brokers, and hopefully that would change next year.

“In the last 12 months, brokers are probably working harder than they ever have for probably the same, maybe slightly less in some cases,” he said.

Brokers had put a lot of energy into looking after customers in an environment in which it’s been difficult to get serviceability. “The implications are having to stay in contact with clients for longer, deals taking longer.”

White (pictured below) said LMG was training brokers in this area, including “engaging customers beyond the transaction”.

Sale said it wasn’t the lending policies that were a challenge, it was the serviceability.

Lam noted that wage growth hadn’t caught up, and unemployment had risen slightly. He said AFG’s focus was on its broker members and their customers. “We’re looking at the whole broker business and ways to help our brokers improve profi tability, given that some are not settling as much, or loans are taking longer to settle.”

Everyone was talking about broker diversification, he said, and AFG was educating brokers to “take that first step to identify the customer” that needs diverse services.

Lam said AFG not only led the charge in introducing approved policies to enable brokers to utilise (1%) serviceability buffers for their “mortgage prisoner” customers, but had also created a brand-new product including the 40-year interest-only (ever-green) loan for mature-age borrowers looking for greater repayment flexibility as they transitioned into retirement.

White said the value of brokers was on display when it came to tackling serviceability.

“You need to have niches, you need to understand where your product is. It just goes to show why broker market share is going to keep growing, because the tighter it gets, the more customers are going to need an adviser, and that’s been a real upside this year for the industry.”

Foley (pictured below) agreed with White and said the value of brokers was that they were across all the lenders’ activity when it came loans.

“The banks seem to be revisiting their mix more frequently now,” Foley said. “They see an opening – they’ll price to win and get a good inflow. Then they’ll tighten a bit or someone else will come in.”

He said one of the major banks had been almost “double sharing” off the back of policy and pricing changes, which was good for brokers and their customers.

Sale said it was a challenge to ensure the major banks didn’t dominate again. “At one stage in the industry, we got to a really nice balance, where the [loan] percentages were a really nice spread. We need the other lenders to lift so it can become a very balanced environment.”

Slater agreed and said that with the changing market, a diverse lender panel really came into play.

“That product innovation you’ve spoken around is really important,” Slater said. “That’s why we [Mortgage Choice] were so excited to enter into a partnership with Athena Home Loans to create the white label product suite, Mortgage Choice Freedom. Athena’s serviceability model is really powerful, and we’ve had great customer outcomes.”

Slater said it was about finding the right lender for the scenario and ensuring that broker members realised they had a lending panel for a reason.

“Brokers can vote with their feet, even under a best interests duty … so the more innovation lenders deliver for brokers, the more we see brokers recommending those lenders to their customers.”

MPA raised the issue of serviceability constraints and the challenges brokers faced with customers rolling off fixed rates.

Cramb (pictured below) said Lendi Group had approached these issues from an industry advocacy perspective, setting up and publishing a ‘loyalty tax index’ 18 months ago, which looks at front-book and back-book pricing.

“The great news is … customer awareness of this then drove a reduction in that index,” said Cramb. “We were at 70 points only 18 months ago, between back book and front book; we’re now tracking at 10. So that tells me that the customers are finding ways through the broker proposition to move forward.”

Cramb also acknowledged the advocacy of the MFAA and FBAA on home loan discharge timing and the home loan price enquiry.

He said Lendi Group had contributed to the MFAA’s white paper that it recently submitted to the federal government, which recommended ways to streamline and speed up loan discharges. Cramb said the aggre-gator provided data that shined a light on lender practices and helped lead to better customer outcomes.

One of the challenges for brokers was finding customers, so the group had been helping brokers generate new customers through tactical campaigns such as its recent Great Aussie Giveaway campaign, which had driven the “biggest appointments ever”.

Cramb said the network had also been working with brokers to scale up their brokerages and reduce costs, assisting franchisees to “become CEOs of their businesses”.

Slater (pictured below) said at Mortgage Choice brokers were at different stages in their careers, and market dynamics were constantly changing.

“Sometimes franchise owners are seeking additional support with lead gen, sometimes with back-book retention, sometimes with loan processing,” Slater said. “Our role as an aggregator is to be working and innovating to match where our business owners are at. We need to be match fit for the market – wherever that shifts.”

Marsi said with challenge comes opportunity. “It’s an opportunity for brokers to further elevate their efforts and differentiate themselves, in terms of sales, prospecting and marketing.”

He said LNS valued keeping brokers informed about the current market and potential trends. “That way you’re upscaling and empowering brokers to feel confident and knowledgeable, which enables them to effectively educate their customers. I think that’s crucial.”

Buchanan (pictured below) said that at SFG education was paramount, and brokers were provided access to great content.

“The best investment a brokerage can make is in education. The good ones are always learning, adapting, evolving, and it’s because education becomes knowledge, and with that knowledge you identify opportunities and assist people.”

When it came to market share, Buchanan said it was important to remember that “without competition we don’t exist”, and there were many benefits that consumers enjoyed due to this competition. In uncertain economic times, customers rushed back to safety, and that safety had always been the big banks.

“It’s disappointing to see big bank market share grow across the industry, and sometimes that comes from complacent conversations. I’m sitting with a customer, they’re banking with big bank B, it’s easy for me to keep them there rather than have that different conversation of it’s a wider world out there and let’s explore those options.”

On refinancing, Buchanan maintained his views from last year. “If you’re in the system and fundamentally nothing has changed, and you’ve got 27 years to go of your 30-year term, and you can refinance to a cheaper rate, why do you have to jump through those serviceability hoops?”

If nothing had changed on affordability and the bank was willing to accept the risk, the regulator should step in and allow it to occur, Buchanan said.

Lam said that, pleasingly, innovation was occurring, with some lenders offering simple refinances at a lower buffer, and AFG had a compliance policy to help brokers facilitate this type of loan.

But Buchanan said this did put brokers at risk by not validating income documentation and making sure the loan could be serviced.

He said when it came to competition, there were a number of lenders heavily scrutinising deals, trying to get to a ‘no’, and there were others, particularly second-tier lenders, trying to get a ‘yes’, and their market share was increasing.

Q: With residential mortgage broker market share at a record 74.1% and aggregators’ growing focus on diversification into commercial and asset finance lending, how are you equipping your brokers to take advantage of this sector and grow their businesses?

Sale said outsource Financial had identified that commercial and asset fi nance was going to be the “next big thing” for brokers about two and a half years ago.

With a focus on training and education, she said outsource had created mentoring programs for its members, enabling resi-dential brokers to get into commercial and asset finance. “We worked with the lenders on this, and that’s been extremely successful. We’re seeing a much more diverse broker out there.”

Residential brokers moving into this space usually started off with asset finance, Sale said. More and more brokers were diversifying, so working with lenders on the mentoring program and accreditation process gave them some comfort.

“They’re not going to just go around accrediting brokers with zero experience, so we have to build around it. We’ve got to create that path for them.”

King (pictured below) said clients weren’t getting what they needed from business banking.

“They traditionally always just went to their existing bank, and in this changing environment, they have to go elsewhere for solutions,” she said. “The major banks don’t return phone calls, you can’t get a small business banker, you can’t get someone to do something small, because it’s not worth it [to them] or their KPIs for that month.”

This was where the broker channel had to come to the fore. “They will be seen to be independent [and] have the right advice and solution for what the client needs instead of pigeonholing them to the one bank or saying often, ‘no, I can’t help you’, and the client accepting that from their business bank.”

Cramb said diversification was not only a growth strategy or new income stream for brokers but also a retention strategy. Brokers were learning that if they didn’t offer commercial and asset finance, someone else would.

“They’ve got to be able to offer that breadth of product range,” said Cramb. For Lendi Group, it was about providing brokers with options and support, whether they wanted to specialise, or have a referral arrangement if they didn’t want to do the deals themselves.

Foley said diversification meant “different things to different brokers at different times”.

“We’ve had some where their first diversification strategy was – use more lenders. Keep doing resi, you’re good at that, but you’re too focused [on particular lenders] and you’re falling into habits, so let’s diversify, and it’s worked.”

Foley said brokerages could also diversify by hiring someone from a different background to their team; for example, all-male brokerages bringing a female broker on board.

“You can also look for different types of clients. If they’re all owner-occupied resi, get into investors, get into SMSF.”

He said it was sometimes better to diversify this way before looking at commercial and asset finance.

Slater said it was all about changing a broker’s mindset away from focusing purely on residential. “Three years ago, it was just raining residential loans, but we’re in a different market now, and it’s important that brokers diversify their businesses.”

Mortgage Choice also focused on education, and it was important for brokers to share their diversification success stories, Slater said. “We put a big focus on knowledge-sharing because brokers often learn the most from their peers. As soon as they share their success stories, that’s when you see traction.”

Diversification was not new, Buchanan said. He remembered back in 2009 during the GFC when “everybody was screaming from the rooftops about diversification”.

“It’s OK for pundits to talk about diversifying and tell people to do it – [but] when the rubber hits the road, they need to know how, and that’s where education and training come in.”

White said LMG now has 60 people in its asset and commercial finance team and launched its first commercial tech platform within myCRM in April with significant investment in this space.

“We want to have a commercial, asset and resi platform together because, going forward, businesses are going to get bigger, there’s going to be less of them, and they’re going have to be multidisciplinary.”

White said what was missing was “how to get there”, and this would require technology, process and structure, with features such as online submissions and quoting tools.

Buchanan agreed and said that while there were some tech solutions, a lot of innovation was needed.

He said SFG had started focusing on diversification, including education and partnerships, a few years ago.

“Last year our commercial volumes went up 50% through our existing network, so you can tell that the education piece and the access piece actually works and translates to opportunities.”

Lam said education was also key at AFG, especially teaching the sales teams to be better business partners for brokers. “Understanding our brokers’ needs and focusing on profitability, analytics and insights is critical.”

He said AFG brokers had large customer bases with plenty of self-employed clients who they could tap into for diverse lending.

Using a McDonald’s analogy, Lam said: “They are the best in the world at what they do. When you go to Maccas, they will offer you a range of their products, including the fries and the Coke.

“It costs so much to acquire new customers. You’ve already helped them secure funding for their home or investment – why aren’t you considering all their needs? We call it life admin: it’s commercial, it’s asset, insur-ances, utilities.”

Lam said AFG had built the Partner Connect platform, which enables brokers to refer customers to different platforms for their needs, such as Fintelligence (Broli Finance) for asset finance, Marketplace Finance for commercial and AIA Financial Wellbeing for life and health insurance. “Our brokers have already seen the quick wins,” he said.

AFG brokers were also encouraged to segment customers depending on their life cycle. So, for clients over 50, brokers should ask if they could write the personal loan for their child’s first car. Lam said this built a more valuable, scalable business.

He added that if brokers didn’t want to be experts in asset or commercial, they should find the customers first and then partner with someone through a spot and refer.

Cramb said in the future there would be fewer brokerages, but these would be more sophisticated, boasting breadth and quality of service.

“We’re now a significant industry, and we have significant operators. It’s great for the customer, great for the broker and ultimately great for the industry as well.”

Marsi (pictured below) said diversification had been a cornerstone of LNS’s value proposition for the last 13 years. “For us, it extends beyond commercial and asset finance to include self-managed super fund lending, business finance and personal loans.

“Our discussions with our advisers are around cash flow management versus book building. Training and education is crucial. We invest a significant amount of time in the training and education of our adviser network.”

Sale said she totally disagreed with spot and refer, and outsource Financial had spent a lot of time and money on educating brokers to diversify.

“That’s what training and education is all about. More and more brokers don’t want to do spot and refer because they’re a business owner. They want to educate themselves, not build up Joe Blow over the road.”

Brokers didn’t want to give their clients to another person because they could lose the clients, said Sale.

Both aggregators and lenders needed to be on the journey with the broker, helping them to learn how to write commercial and asset finance.

White said LMG offered over 300 courses on Brokerversity, and asset finance was always in the top five. More brokers were looking to asset and commercial finance to maximise their revenue and expand their services to customers.

Broker question from Kristie Gould (pictured below): In the current challenging market, what are aggregators doing to support existing franchisees and broker members to achieve their business goals and grow their existing businesses

Sale said outsource Financial had a major focus on training and education.

“We as an industry want to encourage new entrants to come into our industry; we want to keep it vibrant. But what we saw is other groups charging all this money for so-called mentoring, and that mentoring just wasn’t there.”

So, outsource built its own complimentary mentoring programs for broker members. The programs educate new brokers about being a business owner, with a focus on lending, products, compliance, technology and marketing. Sale said they had been highly successful.

“We work with those new entrants; we sit down and do a broker business review, and we help them build to where they want to go. They need support like that, not to pay someone $5,000 and get zero support. The stories that I’ve heard … [are] an embarrassment for our industry.”

Foley said it wasn’t as bad as it had been in the past. “I agree [with Sale], but I feel like we’ve evolved through that largely to a more structured approach”.

Buchanan said he hadn’t seen any new data, but when half of all new-to-industry brokers failed in the first two years, “we’re not doing it well”.

“I think that the regulations around new entrants and mentoring procedures aren’t heavy enough; there’s not enough weight there,” he said.

Buchanan said people were attracted to broking by the thought of running their own business, but apart from completing their Cert IV or diploma, many hadn’t completed any business courses.

“I’d encourage further coursework in business ownership in particular, but it’s also our job to work with the partners and try to understand what they [the brokers] are trying to achieve and then shine the light on to the things that they don’t see,” he said.

“This whole thing of growing for the sake of growth, and I’ve always got to do more, doesn’t apply in every case.”

Buchanan said aggregators saw how thousands of broker businesses operated, and each business was unique.

“It’s about understanding the cost and journey to that growth. No decision is made today and then remunerated tomorrow; it’s actually a journey and needs patience and understanding.”

Slater said Mortgage Choice operated a Broker Success Program to address the two-year dropout. It provided support with the broker’s business and other key areas such as marketing, data and technology.

He said it was important to remember that while investment in new brokers to establish best practice was important, so was providing support further down the track.

Acknowledging that broker support had to keep evolving and innovating to keep pace with where the business owners wanted to go, Mortgage Choice had also recently set up the Peloton program.

“Using a cycling analogy, just think of it as the ‘chasing pack’, ” Slater said. “We’ve identified like-minded businesses, who may be at different stages but which are all ready for growth, and brought them together.”

About 65 businesses are involved in the Peloton program, including Gould’s. While the program includes structured content, sessions are predominantly focused on facilitating insightful conversations between members.

Foley said the Cert IV and diploma qualifications were like a learner’s permit. “It doesn’t mean you know how to drive a car. You don’t learn until you’re actually in business and doing it.”

White said LMG did not admit new-to-industry brokers; they had to work for a broker first. “Mentorship needs to be from a business owner, not from a mentor,” he said.

“We also recognise business owners want to grow – the biggest challenge is recruiting and managing staff.”

LMG helps brokerages screen and recruit brokers through its TalentForce service, then onboard, upskill and manage them through Brokerversity.

White said that when one of LMG’s brokers completed a Cert IV or diploma through Brokerversity, “they were actually qualified on the tools, know what AOL [is], know how to submit a loan, know what LVR is”.

“We get them out where they’re ready to rock and roll.”

White said LMG was also helping brokers with a profitability analysis service.

Cramb said benchmarking was “where the real science occurs, because not all businesses are created the same, but you can find like-minded businesses in the peer-to-peer”.

“How am I performing where I am in my journey is really important,” he said.

Aussie is also looking at benchmarks but from a franchise viewpoint and offers the Grow and Plus supported model, which involves a customer acquisition model or Aussie brokers were supplied with qualified appointments, and the loan packaging was done for them.

“So the broker can focus on earning quickly. The first eight weeks of being a broker, they’re submitting over eight to 10 lodgements because they have a fully supportive model.”

To White’s point, Cramb said the B2B problem was trying to bring in new talent and retain them, so this was Aussie’s response. “We’ve definitely seen a step change in the way that this has allowed the franchisee to bring in a new broker and keep that broker.”

White said LMG had found that the best pathway for new brokers was to start off as a customer service manager and then transition to being a broker.

He said leads were also becoming a bigger challenge for brokers coming into the industry.

“Where am I finding the next customer? We’re finding we’re having more and more discussions about marketing than we’ve had in the last few years.”

Foley said the refinancing frenzy had also disappeared, which made it harder for brokers.

Lam said most brokers started out thinking they wanted to be a self-employed broker, not thinking, “I’m going to be a business owner one day, and the GM, the counsellor, the HR manager and accountant”.

HR strategy was critical to the success of any business, he said. “So, when you’re looking for new talent, [it’s about] understanding where you want to be as a business over five years, the customer experience that you want to deliver, the process underlining all of that, and then plugging in the people.”

AFG focuses on helping broker members find the right people for their business. “If you need an ops manager or sales manager in five years, bring them in as a rookie and train them for five years,” Lam said.

Building a sustainable business came down to the contractor versus employee model, he said. “Our members, rightly so, are hesitant with the initial upfront costs of the employee model, but longer term, it could improve the valuation of your business.”

Lam said AFG had created a learning and development service enabling any of its broker member groups to brand their own learning portal “based on their content and our content”.

“To your point, Tanya, there’s some different set-ups out there,” Lam said. “We have a struc-tured approach to mentoring and have part-nerships with a panel of mentors, such as Mr Mentor, who we vet and approve.”

He said AFG tried to help all brokers and their team members, for example mums returning to work who “might be great at operations but don’t want to be brokers”. “What you’re trying to do is grow a business that one day you want to sell hopefully not at multiple of trail but a multiple of EBITDA.”

Broker question from Adriana King: What is the next game changer or enhancement to your offer in the pipeline?

White said LMG had recently launched Smart Data, which was “a chance to really help brokers save time”. It was based on open banking and getting an application to a vendor using permission data rather than documents.

“We’ve seen it cut down the file time by three days … our biggest thing at the moment is how do we help our brokers save time on an application, and then through that, how we help them grow their profitability.”

Cramb said a technologyled experience was at the core of Lendi Group’s proposition, and the group was working on Approval Confidence, which provided direct integra-tion with the lenders.

“Our vision is that that will give us real-time approval,” Cramb said. Saving time and providing a better customer experience were the aims.

He said the group was also using AI for lender policy and pricing that searched in real time and provided more accurate and timely results. And phone-based brokers were being assisted with phone scripting and scoring when talking to customers, which also saved time and was valuable as a training tool.

Cramb said AI, data and open banking were the next big frontiers in broking. Aussie had also just launched a new app that provided customers with property valuations and reports but “also have the broker business in their pocket”, allowing brokers to interact with customers.

“We’re very close to being able to do the processing of the loan through that app as well,” said Cramb. Slater said realestate.com.au played a huge role in powering Mortgage Choice’s engagement of customers and consumers.

“Mortgage Choice is a lead gen business in its own right, so adding the leads from the Mortgage Choice website with those coming through from realestate.com.au now drives about 10% of value from a settlements perspective,” Slater said.

“Having access to realestate.com.au’s audience of 11 million Australians is really, really powerful for us. And we’re working to bring that audience together with Mortgage Choice’s brokers to help more consumers find and finance property in the one place.”

Slater said Mortgage Choice was empowering brokers with technology and focusing on driving efficiencies and connecting consumers with a broker at the right time.

“It’s all about making those franchises as profitable as possible. Data is a really big focus area for our business, and thanks to REA Group’s PropTrack, our brokers and their customers have access to rich property insights, reports and valuations.”

Lam said AFG’s view was that the best way to attract customers was to combine AI with humans. “The humans being our brokers, our broker being the champion, and providing them choice on the tools that they want to use.”

Lam said because tech was moving so fast, AFG was moving away from building one system for use. “It’s about what are the best tools in market and if they’re safe to use and we can vet them – how do we put that in our brokers’ hands?”

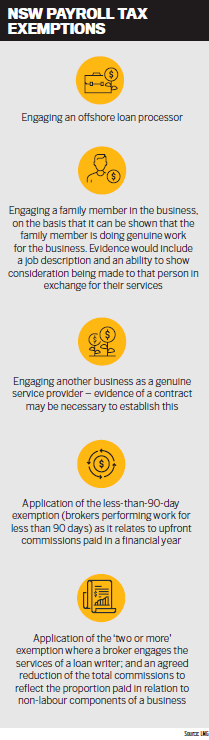

Q: What impact will the NSW Supreme Court’s decision that aggregators are liable for payroll tax have on you and your broker members? Do the exemptions go far enough in easing the burden on brokers?

White said the payroll tax exemptions didn’t go far enough. “I think it’s a reflection of the fact broking actually hasn’t changed much in 30 years. Technologies change, regula-tions change, but the fundamentals are still the same.

“We still don’t believe that it [payroll tax] should apply, but the judge in our case, Justice Richmond, decided that we were wrong.”

White said the implication of the Federal Court’s decision was that there would be fewer single-broker operations. “The government’s decided that people can’t be in busi-ness by themselves for themselves and need to be in business now with other people. I think that’s a sad indictment of what the government’s done.”

He said there would be more consolidation of brokerages, with the trend of bigger businesses continuing to accelerate. “People will employ more staff. There’ll be less businesses; they’ll be bigger. I think that will probably be good for customers. It’s not necessarily good for brokers who don’t choose to do that.”

White described it as sad day for individual brokers, who would be forced to consolidate with other businesses.

“The exemptions don’t go far enough,” he said. “No doubt there’ll be more legal cases coming up, and there’ll be more tests of this [law], and we’ll learn more as we go through.”

White said the NSW government was taking money out of the system – a system the industry had invested more in for customers and compliance.

“They went after doctors last year; they’re going after the gig economy.” King said, “We already pay 10% GST on our services and can’t claim a GST credit on the income we distribute to ourselves personally.

“The payroll tax shouldn’t exist at all and would add 5.45%. Adding to our personal tax rate is a prime example of government taking multiple clips along multiple lines of small business.”

Sale said the industry was not going to sit still on the issue of payroll tax. “We’re going to be going straight to the government; we’re going to lobby it big-time, just like we did in the royal commission. We’re just not going to leave Sam and a couple of others out on a limb; we’re all going to get in on this together.”

Sale said she believed the industry would come out of it all right because “the govern-ment has indicated to us that they support what we’re saying”.

Foley said the judge had stated that the payroll tax was capturing businesses it wasn’t intended to capture. White said LMG was keen to lobby on behalf of brokers on this issue.

“What’s frustrating is that it’s taking away the option from individuals to run the business the way that they should.”

He said LMG would have to employ extra people to deal with the tax.

Lam said that sadly this had the potential to be a national issue as tax regimes were largely harmonised across the states, meaning that if one state introduced or enforced a tax, the others generally follow suit.

Buchanan said the judge was quite objective around the rules. “It goes to show that we are a complex industry, and it takes a lot of learnings to understand it,” he said. “We’re vehemently against it [the tax].”

Regardless of the payroll tax, the rate of individual brokers joining brokerages had never been greater, Buchanan said. “I think we’re going to see more consolidations and bigger businesses. I think this ruling will give that a bit of shove along.”

SFG also didn’t accept new-to-industry brokers for a number of reasons, Buchanan said, and SFG brokerages were growing by proxy because of that.

“For businesses such as yours that are looking to scale up, get your model right now, get your offer ready, because they’re coming,” he said.

White said LMG was most worried about brokerage businesses that were on the payroll tax threshold in each state. He said these employed staff that had more than $1 million in commissions going out to other brokers.

“That’s where the liability is going to sit.” “What we’re trying to do is actually make sure that bigger businesses have the right structure in place to able to manage this going forward,” White said.

“If you’re a one-man band you get caught; if you’re in the sweet spot you’re OK; if you’re too big, you get caught.”

One of the payroll tax exemptions involved an LMG broker using outsourced services 10 times in one year.

Buchanan said that while White described the LMG court appeal against the payroll tax as a loss in some areas, there were many positives in the exemptions.

Q: As more and more brokers reach retirement age and plan to leave the industry, how are you assisting them in successfully exiting but also attracting, training and retaining new brokers to take their place?

Slater said succession planning looked different for every franchise owner, depending on their business, how it was structure and the owner’s goals.

“It could be a family transition, it could be a plan for retirement via expansion and then ultimately a sale, or a partial book sale into the network. We are active with our network on this subject, and it’s about planning ahead.”

Mortgage Choice’s recruitment team was always looking for new brokers who could play a role in retiring franchisees’ succession plans, Slater said. “When we find someone who is looking to buy a business, we can connect them with a franchisee who is opento a partner joining their business as part of their succession plan.”

Mortgage Choice’s recruitment team was always looking for new brokers who could play a role in retiring franchisees’ succession plans, Slater said. “When we find someone who is looking to buy a business, we can connect them with a franchisee who is opento a partner joining their business as part of their succession plan.”

The benefits of partnering with a broker meant the franchisee could scale back over an agreed time frame while the broker developed skills and business knowledge, learning from an experienced franchisee.

Cramb said the industry was going through a generational change. “There’s an opportunity to help older brokers bring in a new generation of brokers but at the same time have a different role in their business. So we’re trying to create platforms and pathways for that.”

Sale said outsource Financial took its position “as a true business partner to our brokers seriously and work with them to be successful, whatever stage their business is at”.

“Our state-based relationship managers have a very high-touch, engaged relationship with their brokers,” Sale said.

“When they identify a broker is considering growing their team, be it with brokers or support staff or they are considering their options to retire, we assist them in working out a strategy that is right for them, be it attracting talent to transition to owning the business or taking the pressure off so they can enjoy the semi-retirement that is so attractive to a lot of brokers – we help them implement the right strategy.”

Buchanan said there were many ways for brokers to plan their exit. “But the three most common that I see are sale, partnership and subsequent exit or succession. With each, SFG is able to assist, advise, value and even fund these acquisitions for our members.”

Marsi noted that while the industry offered flexibility and a lifestyle that allowed many brokers to work well into their 60s and beyond, it was an issue to be mindful of.

“We are focused on encouraging new entrants into the industry, whether through the establishment of new businesses or through succession planning strategies,” Marni said.

“We’re seeing an increase in the success of emerging family-owned businesses, which is a promising trend. But we can’t rely solely on this. Therefore we are placing a strong emphasis on calibrating our mentoring programs to provide comprehensive support and training to new brokers, ensuring they are well prepared to thrive in their roles.

“By fostering a supportive and educational environment, we aim to attract, train and retain the next generation of advisers who will continue to drive the industry forward.”

Lam said AFG offered a comprehensive suite of education and support programs for its brokers, designed to help them through the different stages of their business life.

“The retirement phase is no different. It takes time and considered planning to transition to retirement. We offer a buy/sell program and connect our retiring members with broker groups who are looking to grow, that meet the retiring brokers’ requirements.”

White emphasised LMG’s proactive approach in helping business owners realise the full potential of their businesses through a dedicated succession and profi t analysis team.

“From initial planning to eventual transition, this team partners closely with them, offering services ranging from creating information memorandums to managing the transaction itself and everything in between,” he said.

“Ultimately, LMG is committed to part-nering with businesses for their full life cycle, ensuring a seamless transition for brokers when they are ready to step out of their business, while attracting, training and retaining new talent to take their place.”

What do you think are the biggest issues for aggregatora and their broker members? Comment below