50,000 places available – but research clients and criteria, says CEO

Brokers wanting to tap into the 50,000 new places released for the Australian government’s Home Guarantee Scheme need to do extensive research and understand the eligibility criteria inside and out before offering it to their clients.

That’s the view of Alan Hemmings (pictured above), CEO of Sydney brokerage Home Loan Experts, which assists many first-home buyer customers, and uses its brokers’ expertise to access both the federal scheme and various housing schemes offered by the states for its clients.

Hemmings spoke to MPA about the Home Guarantee Scheme (HGS), including the restrictions on income, and property price caps, as the government announced that as of July 1, 50,000 more places had been made available through the scheme for the 2024-25 financial year.

“We do talk to a lot of first-home buyers, so for our team it’s being aware there are any number of schemes for first-time buyers at state and federal level,” said Hemmings.

“Understanding how the schemes operate and how first-home buyers can benefit is really important because you may miss an opportunity.

“We pride ourselves on doing business with clients that find it hard to get their deals done and some first time buyers fall into that category … we have to be across all the schemes.”

Read more: How mortgage professionals can help first time buyers get that new home

Three parts to the Home Guarantee Scheme

The Home Guarantee Scheme (HGS), which has been running since January 2020, is designed to help eligible home buyers to buy a home sooner, including first home buyers, single parents and people in regional areas.

The 50,000 new places available for the 2024-25 financial year include:

- 35,000 places for the First Home Guarantee

- 10,000 places for the Regional First Home Buyer Guarantee

- 5,000 places for the Family Home Guarantee

Thirty-two lenders are part of the HGS, which is administered by Housing Australia, has supported more than 160,000 people to buy or build their own home.

First Home Guarantee

Under the First Home Guarantee Scheme, applicants must provide a minimum 5% deposit, with Housing Australia providing a guarantee of up to 15% of the home loan value to the lender.

Applicants must be first home buyers or previous homeowners who haven’t owned a property in Australia in the past 10 years, Australian citizens or permanent residents, and individual or joint applications who are at least 18 years of age. They can’t earn more than $125,000 for individuals or $200,000 for joint applicants.

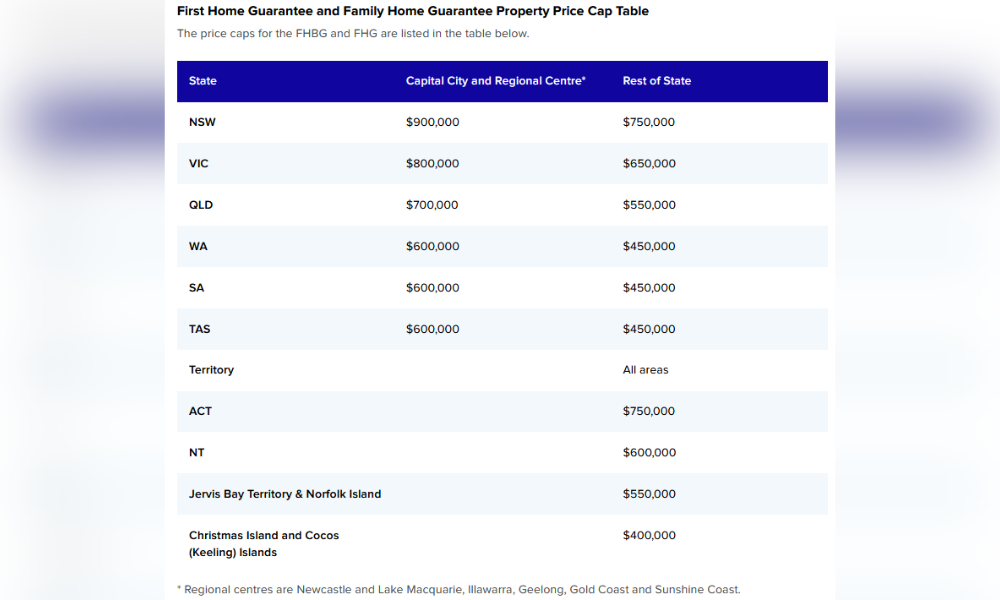

There are also property price caps which vary depending on where you live (see table below)

Source: Housing Australia

Regional First Home Buyer Guarantee

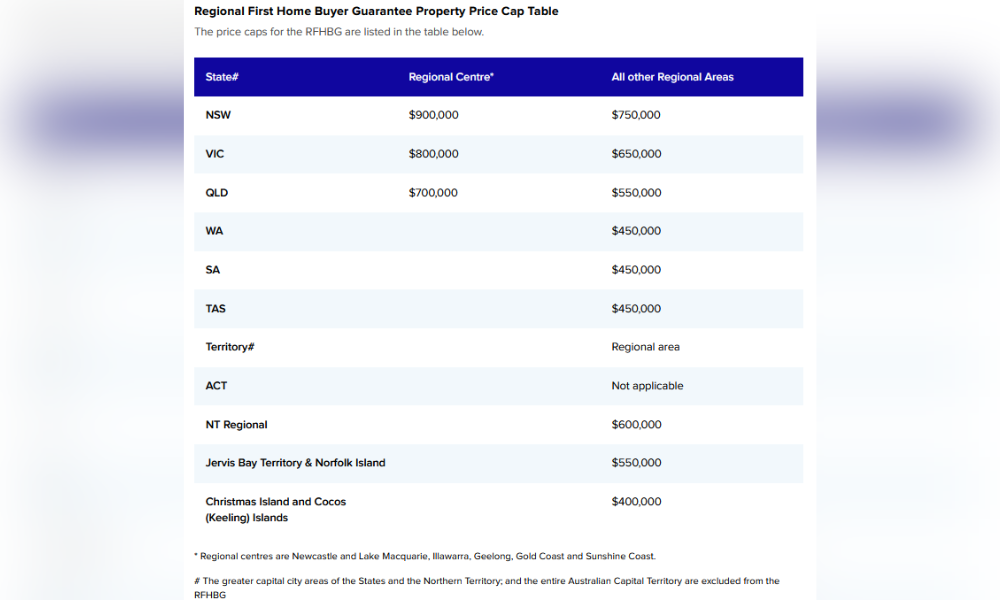

The criteria for the Regional First Home Buyer Guarantee is the same as the First Home Guarantee except it is aimed at applicants purchasing property in regional areas only. The applicants must have lived in the regional area or adjacent regional area they are purchasing in for the preceding 12-month period to date of the home loan agreement.

Source: Housing Australia

Family Home Guarantee

Under the Family Home Guarantee, the minimum deposit is 2%. The criteria is the same as the First Home Guarantee, except it’s only open to single parents or a single legal guardian of at least one dependent.

Applicants cannot currently own a property or do not intend to own a separate property when they settle on the home.

Brokers need to understand schemes

Hemmings said the good thing about the HGS was that customers could get into the property market with as little as 5% deposit, “without the need to go to mum and dad”.

“Understanding all of the various schemes is important for brokers who want to play in that space, because if they don't get it right, a, it can end up with a customer complaint that can turn nasty if it gets to AFCA, and b, you might just miss the opportunity.”

While the HGS mean participants don’t need LMI, Hemmings said there were other ways to avoid LMI, including a gift, or a family guarantee.

Home Loan Experts (HLE), which has a team of 26 brokers, has assisted a small number of clients to access the HGS, including the First Home Guarantee and the Regional First Home Buyer Guarantee scheme.

Hemmings said HLE had assisted more clients with other state-based schemes.

The new HGS was harder to access because of the property price caps, which he said weren’t appropriate for the eastern seaboard capital cities.

These were $900,000 for Sydney and other NSW regional centres and $750,000 for rest of the state, while in Melbourne and Geelong it was $800,000 ($650,000 for the rest of Victoria); and $700,000 for Brisbane, the Gold Coast and Sunshine Coast and $550,000 for the rest of Queensland.

“You look at Sydney, Brisbane and Melbourne – there wouldn’t be too many properties you could buy these days that fit within the price cap,” said Hemmings. “All of these schemes need to be tied to what is happening with property prices.”

Because governments didn’t review the property price and income caps, it acted like tax creep, he said.

“Each year the customers that can actually qualify or the properties that are for sale that can qualify, reduce.”

Hemmings said these difficulties meant brokers needed to talk to their first home buyer clients about other options, including stamp duty exemptions and other schemes.

He said the Family Home Guarantee was even harder to access given the small pool of people eligible – those who had been out of homeownership for 10 years.

In terms of public awareness of the HGS, the brokers at HLE encountered two types of customers – those who had done their research and understood what was available and those “who had no idea”.

“They're the ones that you've got to coach through the process and talk to them about what they need to do.”

Advice for brokers

Hemmings said it was tough for first-home buyers right now, with servicing the biggest issue given the current level of interest rates.

“We did a quick calculation and for a single person at $125,000, they probably have [been] struggling to buy in Sydney, for example at the moment because of servicing issues. It’s hard. You look at what they’d need to service a debt of a million dollars and that’s more than $125k.”

Serviceability and interest rates were factors that sat outside of the first-home buyers schemes.

Hemmings encouraged brokers who were looking at the HGS or other schemes to be “clear and upfront with the client about what they can and can't do”.

“Don’t set false hope that they’re eligible. Actually do the research before you go back to the customer and get the information from the customer as soon as possible to help you do that assessment,” he said.

“The last thing you want to do is have a client come to you saying we're believe we're eligible, have the conversation and then, for example, you get tax returns and as a couple they're earning more than the $200,000 maximum – that means they’re no longer eligible for the Home Guarantee Scheme.”

Hemmings said it was important for brokers to be careful about the way they handled conversations with first-home buyer clients.

“They’re emotional – it’s their first home they’re trying to buy and they don't necessarily have all of the facts … you’re not working with someone who’s bought property before.”

What do you think of the Home Guarantee Scheme's criteria? Share your views by commenting below