Higher interest rates and affordability pressures drive market into a cyclical downturn

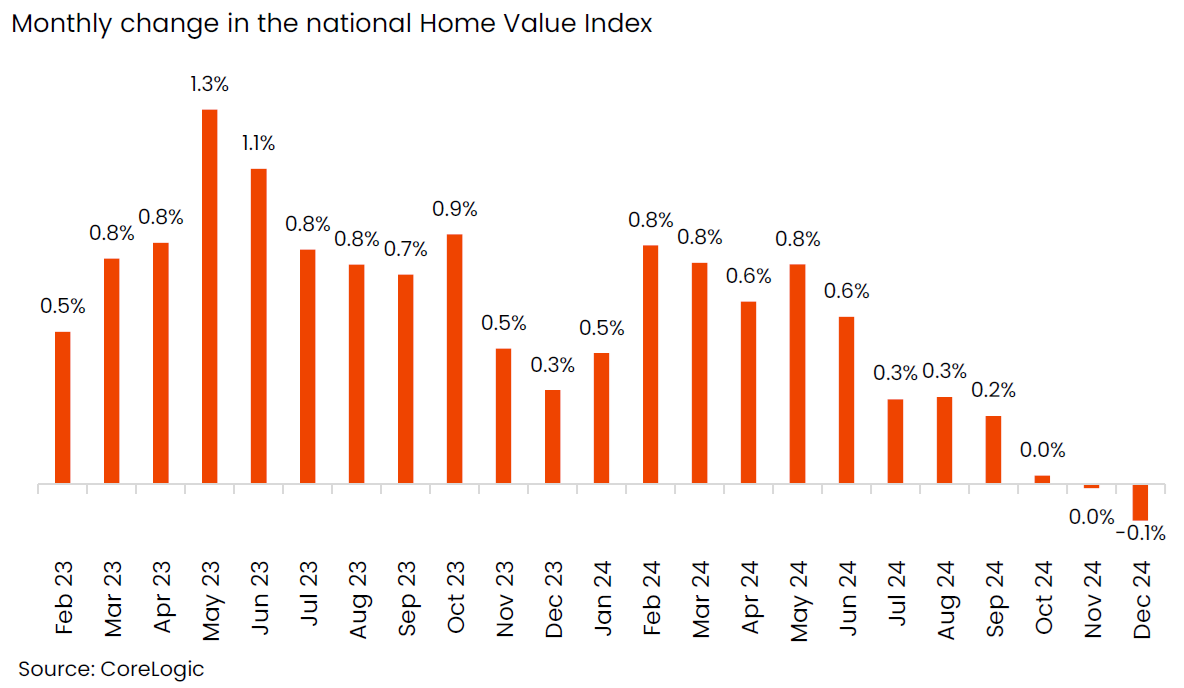

Australia’s housing market has entered a downturn after 21 consecutive months of growth, according to CoreLogic’s national Home Value Index (HVI).

Following a peak in October 2024, the index recorded a marginal decline of 0.01% in November and a further 0.1% drop in December. This marks the first sustained fall in home values since the market’s growth phase began, which saw prices climb 14.3%.

“This result represents the housing market catching up with the reality of market dynamics,” said Tim Lawless (pictured above), research director at CoreLogic. “Growth in housing values has been consistently weakening through the second half of the year, as affordability constraints weighed on buyer demand and advertised supply levels trended higher.”

Several key indicators, including rising listing volumes and extended selling times, suggest a cooling market. Total property listings at the end of 2024 were 5.0% higher than a year earlier, while the average selling time increased to 33 days in December, up from 28 days a year ago.

Affordability constraints dampening demand

Housing affordability remains a key issue, with high interest rates and stagnant wage growth limiting purchasing power. CoreLogic estimates that a median-income household in Australia can afford a home priced at $513,000 — significantly below the national median dwelling value of $815,000.

The affordability gap has been sustained by wealthier buyers, including those using profits from property resales or higher disposable incomes. Some buyers may have also anticipated lower interest rates, which have yet to materialise. As a result, housing demand appears to be waning even among these groups.

Seasonal slowdown or broader trend?

The downturn coincides with the typically quiet holiday season, a period when housing values often stagnate or decline slightly. However, seasonally adjusted data still suggests a broader cooling trend. While the seasonally adjusted HVI ticked up 0.1% in December, this was significantly lower than the average monthly growth rate of 0.6% seen in early 2024.

Price declines were most notable in Sydney, Melbourne, and Canberra, with falls of 0.6%, 0.7%, and 0.5%, respectively. These cities, which account for a significant share of Australia’s housing stock and value, have been the primary drivers of the national downturn.

In contrast, other regions have shown resilience. Regional South Australia recorded the strongest price growth in December at 1.2%, while Adelaide posted the highest quarterly growth among capital cities at 2.1%.

Broader declines likely in 2025

While the downturn has so far been concentrated in a few major markets, analysts predict price falls will spread more widely in 2025. At the suburb level, the proportion of markets recording quarterly price declines rose from 20% in late 2023 to 38% by the end of 2024.

Despite this, any downturn is expected to be relatively shallow and short-lived. Historical data shows national housing value declines tend to be smaller and shorter than growth periods. The largest recorded fall was just 7.7% between October 1982 and March 1983.

According to CoreLogic, key factors supporting the market include a tight labour market, limited signs of distressed sales, and a fundamental shortage of housing relative to population growth. Additionally, moderating inflation and potential interest rate cuts could improve borrowing capacity and buyer demand later in 2025.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.