Broad-based growth across capital cities and regional areas follows February rate cut

Australian property values rose in March, reversing a recent three-month downturn, according to CoreLogic’s national Home Value Index.

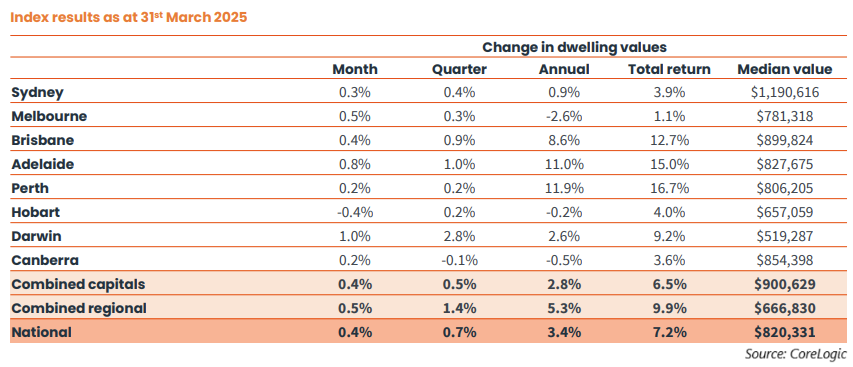

Values increased by 0.4% over the month, marking the second consecutive month of growth after a 0.5% decline from December to February.

The rise was widespread, with all capital cities except Hobart seeing gains, along with increases across regional areas. Darwin led the capital cities with a 1.0% monthly gain, while Hobart saw a decline of 0.4%.

Tim Lawless (pictured above), CoreLogic’s research director, attributed the rebound to “improved sentiment following the February rate cut,” adding that the cut had a direct impact by slightly boosting borrowing capacity and mortgage serviceability.

“With the rate-cutting cycle expected to be drawn out, it will be interesting to see if this positive inflection in values can last in the face of affordability constraints,” Lawless said.

Sydney and Melbourne, which carry the largest weight in the Home Value Index, posted gains over the past two months. Sydney values, which had dropped 2.2% between September 2024 and January 2025, remain 1.4% below their record highs. Melbourne, where values peaked in March 2022, remains 5.6% below its peak despite a 0.9% increase over the last two months.

While mid-sized capital cities are still seeing gains, the pace has slowed, particularly in Perth. Values there, after recent downward revisions, now sit 0.05% below their October 2024 peak. Despite this, Perth has led the five-year growth cycle among capital cities, with home values surging by 75.4% since March 2020.

House price growth across different value tiers is also showing signs of convergence. While the lower quartile had been outperforming since mid-2023, the rate of change is now levelling out, particularly in Sydney. Over the past three months, upper quartile values in Sydney have risen by 0.6%, compared to 0.3% growth in the lower quartile. Historically, higher-value markets, particularly in Sydney and Melbourne, have responded more strongly to lower interest rates, although most other capitals still show stronger growth in the lower quartile.

Regional markets continue to outperform capital cities, with the combined regional index up 0.5% in March, compared to a 0.4% increase across combined capitals. However, the growth trend is beginning to converge as capital city growth accelerates while regional gains remain steady.

Among regional submarkets, Western Australia and Queensland continue to lead growth. The Mid-West region of WA, including Geraldton, recorded the highest annual growth at 25.4%. Townsville (23.5%), Gladstone (22.2%), Central Highlands (21.8%), and Mackay (20.2%) in Queensland also saw strong gains.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.