What should borrowers watch out for next year?

In its latest report, S&P Global Ratings has forecasted a potential reduction in industry risks within the Australian banking system over the next two years, citing the possibilities of a diminished risk appetite or a lower likelihood of significant regulatory lapses.

The S&P Global Ratings’ global banks country-by-country outlook for 2024, titled “Forewarned is Forearmed”, indicated that factors such as the simplification of business models for larger Australian banks could contribute to this improvement.

“Industry risks could also diminish if we believe the financial sector's net external liabilities are likely to remain well below 20% of domestic customer loans,” said Nico DeLange (pictured above), primary credit analyst.

On credit losses

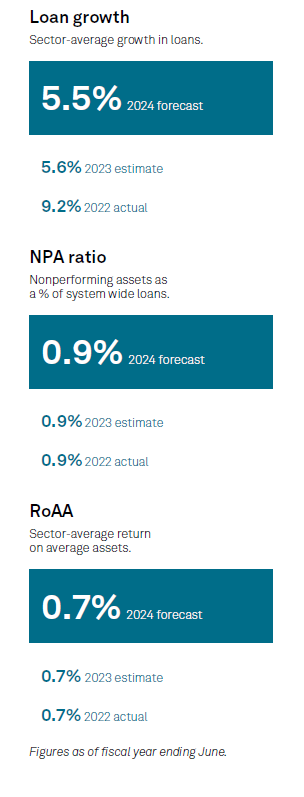

S&P Global Ratings is expecting credit losses for Australian banks to remain low, around pre-COVID levels of 15 basis points, over the next two years. Factors such as low unemployment levels, modest economic growth, and evolving spending patterns are expected to shield borrowers against rising interest burdens, as their lower fixed mortgage rates expire and roll off to higher variable rates.

On house price growth

S&P Global Ratings noted an acceleration in house price growth over the past six months, driven by immigration-driven population growth and limited new housing supply.

“On the flip side, higher interest rates, rising consumer prices, and fragile business, and consumer sentiment could stifle growth,” DeLange said.

On lending standards

S&P Global Ratings is expecting banks to maintain conservative lending standards and to continue pricing rationally for risks, providing the sector with a buffer for unexpected situations.

“The earnings of Australian banks should stay strong relative to global peers,” DeLange said.

What to watch out for in 2024

Diverse uncertainties pose risks

Australian banks are exposed to risks stemming from increasing consumer prices, elevated interest rates, delicate business and consumer confidence, and an uncertain global economic outlook.

“Given the large increase in interest rates and prices in the past year, we consider that some households and businesses will struggle to service their debt,” DeLange said.

Especially susceptible to the industry risks are those who experience job loss or income reduction, are highly leveraged, and borrowed during the peak of house prices.

“Nevertheless, we consider such borrowers form a small part of the banks' loan books,” DeLange said.

Technology risks to escalate

Australian banks remain exposed to cyber threats, with the escalation of these risks attributed to the accelerated pace of digitalisation. This heightened vulnerability could potentially result in more severe cyberattacks, leading to increased financial losses.

Download S&P Global Ratings’ Global Banks Country-By-Country Outlook 2024.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.