Extra training, forms and finding clients have deterred many brokers from writing commercial loans, but not for much longer, explains La Trobe Financial

Extra training, forms and finding clients have deterred many brokers from writing commercial loans, but not for much longer, explains La Trobe Financial

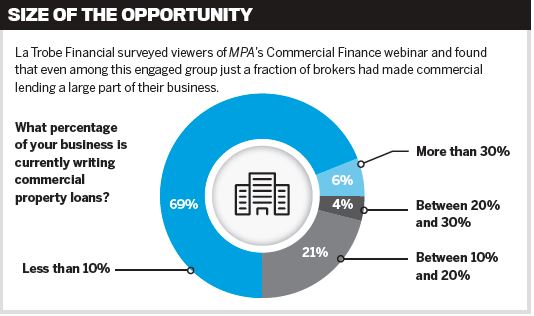

Brokers have been writing commercial loans as long as they’ve been writing residential loans. Lenders increasingly see brokers as a vital distribution channel. Yet progress has been agonisingly slow. Around 2,400 mortgage brokers wrote a commercial loan in the six months to September 2016, according to the MFAA, out of a population of 15,400. Take-up ranges from 10% in some broker groups to 30% in others.

The main reason to diversify hasn’t changed, as La Trobe Financial vice president Cory Bannister explains. “The residential and commercial property markets can perform quite differently at the same point in an economic cycle, and therefore by ensuring you have deal flow you’re effectively insuring your business from any peaks and troughs.”

In fact brokers have more reasons now to write commercial loans as competition intensifies in residential lending. The MFAA also found that new entrants to broking are fast outpacing those leaving the industry, including in areas where the lending market is stagnant or declining. Franchise networks have been quick to react: ASX-listed Mortgage Choice, for example, has made diversification a core strategy for 2017/18.

Traditionally, many brokers have been deterred from writing commercial loans and have found it easier to refer these customers to other brokers or to lenders through a ‘spot and refer’ model. But this approach just doesn’t suit some brokers, Bannister says. “I know that there are brokers reluctant to do that because, obviously, is their customer safe? Does that involve a good consumer outcome?”

Five barriers

Bannister identifies five barriers to residential brokers writing commercial loans: training requirements, extra accreditation, paper lodgement, complex application forms, and lack of support from lenders. That’s even before you get to generating commercial leads. As La Trobe looks to challenge the banks in commercial lending, Bannister is determined to break down these barriers.

La Trobe doesn’t require any extra training for brokers writing commercial loans, Bannister explains. “It’s not that we don’t offer training; we certainly do, and we have a credit-skilled sales team, as well as giving you access to our credit staff here, right through the process, who can train you on the spot.” Other lenders are putting training online or providing it at professional development days.

Nor is extra accreditation necessary at La Trobe, Bannister adds. “If you’ve written a residential loan with La Trobe Financial you will be aware of the process for a commercial loan and can do so immediately.” This is possible because La Trobe uses the same application form for both residential and commercial loans.

When it comes to technology, commercial lending has lagged behind residential. NextGen’s Apply Online and other platforms only began to accept electronic lodgement of small commercial loans last year. But the shift is gathering pace: AFG launched an SME loan platform in August, and the Podium CRM system of Plan Australia, Choice and FAST has been updated to assist commercial lending. La Trobe also allows commercial applications online or through aggregator software platforms.

Although many sub-$2m commercial property applications are very similar to residential loans, others are more complicated, and Bannister is conscious that some brokers need extra support. “It can often be a sink-or-swim type approach, where you’re on your own and you’re expected to know the process all the way through,” he says. His solution is to make his credit team and senior staff available to advise brokers throughout the application process.

The clients you already have

With lenders removing or substantially reducing the barriers to brokers writing commercial loans, the onus moves onto brokers to find commercial clients. This can be done without spending a cent on marketing, because many of these clients are already in your database.

“The easiest way is generally to search around asset types, where you drill into your existing clients’ asset and liability position,” Bannister explains. He says brokers should be looking for “one, whether they hold commercial property; two, whether they’re self-employed, as if they are there may be an opportunity to purchase commercial property.”

Other potential clients include older property owners who may be looking to demolish large properties and replace them with several properties on the same block, using development finance. Bannister says “changes to urban areas means this is becoming an in-demand product”.

Beyond your database, existing referral partners can help promote your new offering. “Have a conversation or try find a partnership with an accountant or financial planner, who are often a really good referral source … once they learn your capability to address a client’s self-managed super fund, for instance, they can be a really strong lead-in,” Bannister says.

With the barriers pulled down and clients ready to go, it’s never been easier to add commercial lending to your business.

Brokers have been writing commercial loans as long as they’ve been writing residential loans. Lenders increasingly see brokers as a vital distribution channel. Yet progress has been agonisingly slow. Around 2,400 mortgage brokers wrote a commercial loan in the six months to September 2016, according to the MFAA, out of a population of 15,400. Take-up ranges from 10% in some broker groups to 30% in others.

The main reason to diversify hasn’t changed, as La Trobe Financial vice president Cory Bannister explains. “The residential and commercial property markets can perform quite differently at the same point in an economic cycle, and therefore by ensuring you have deal flow you’re effectively insuring your business from any peaks and troughs.”

In fact brokers have more reasons now to write commercial loans as competition intensifies in residential lending. The MFAA also found that new entrants to broking are fast outpacing those leaving the industry, including in areas where the lending market is stagnant or declining. Franchise networks have been quick to react: ASX-listed Mortgage Choice, for example, has made diversification a core strategy for 2017/18.

Traditionally, many brokers have been deterred from writing commercial loans and have found it easier to refer these customers to other brokers or to lenders through a ‘spot and refer’ model. But this approach just doesn’t suit some brokers, Bannister says. “I know that there are brokers reluctant to do that because, obviously, is their customer safe? Does that involve a good consumer outcome?”

Five barriers

Bannister identifies five barriers to residential brokers writing commercial loans: training requirements, extra accreditation, paper lodgement, complex application forms, and lack of support from lenders. That’s even before you get to generating commercial leads. As La Trobe looks to challenge the banks in commercial lending, Bannister is determined to break down these barriers.

La Trobe doesn’t require any extra training for brokers writing commercial loans, Bannister explains. “It’s not that we don’t offer training; we certainly do, and we have a credit-skilled sales team, as well as giving you access to our credit staff here, right through the process, who can train you on the spot.” Other lenders are putting training online or providing it at professional development days.

Nor is extra accreditation necessary at La Trobe, Bannister adds. “If you’ve written a residential loan with La Trobe Financial you will be aware of the process for a commercial loan and can do so immediately.” This is possible because La Trobe uses the same application form for both residential and commercial loans.

When it comes to technology, commercial lending has lagged behind residential. NextGen’s Apply Online and other platforms only began to accept electronic lodgement of small commercial loans last year. But the shift is gathering pace: AFG launched an SME loan platform in August, and the Podium CRM system of Plan Australia, Choice and FAST has been updated to assist commercial lending. La Trobe also allows commercial applications online or through aggregator software platforms.

Although many sub-$2m commercial property applications are very similar to residential loans, others are more complicated, and Bannister is conscious that some brokers need extra support. “It can often be a sink-or-swim type approach, where you’re on your own and you’re expected to know the process all the way through,” he says. His solution is to make his credit team and senior staff available to advise brokers throughout the application process.

.JPG)

“If you’ve written a residential loan with La Trobe Financial, you will be aware of the process for a commercial loan and can do so immediately” Cory Bannister, La Trobe Financial

With lenders removing or substantially reducing the barriers to brokers writing commercial loans, the onus moves onto brokers to find commercial clients. This can be done without spending a cent on marketing, because many of these clients are already in your database.

“The easiest way is generally to search around asset types, where you drill into your existing clients’ asset and liability position,” Bannister explains. He says brokers should be looking for “one, whether they hold commercial property; two, whether they’re self-employed, as if they are there may be an opportunity to purchase commercial property.”

Other potential clients include older property owners who may be looking to demolish large properties and replace them with several properties on the same block, using development finance. Bannister says “changes to urban areas means this is becoming an in-demand product”.

Beyond your database, existing referral partners can help promote your new offering. “Have a conversation or try find a partnership with an accountant or financial planner, who are often a really good referral source … once they learn your capability to address a client’s self-managed super fund, for instance, they can be a really strong lead-in,” Bannister says.

With the barriers pulled down and clients ready to go, it’s never been easier to add commercial lending to your business.