Broker pay debate rages on after latest MFAA data

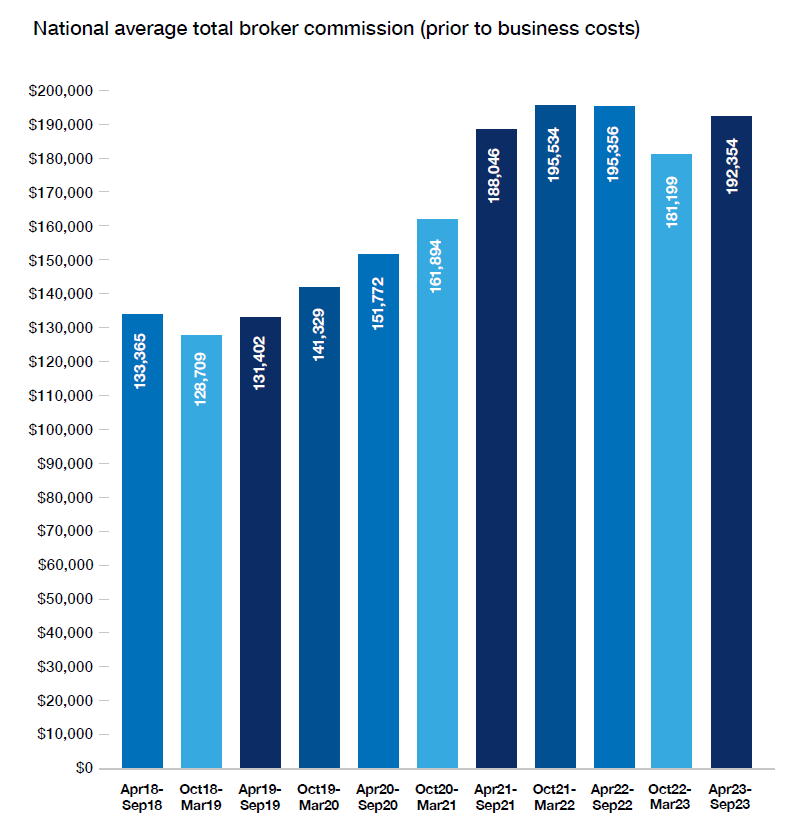

As the debate rages over what bankers dealing with mortgage customers are paid compared to their broker counterparts, data from the latest MFAA Industry Intelligence Service report showed that national average total broker commission declined 1.54%.

The MFAA’s 17th edition IIS report, which covers the six-month period from April 1, 2023, to September 30, 2023, revealed that the total annual commission for brokers, prior to costs, came to $192,354, down $3,002 from $195,356 in the prior corresponding period.

However, when compared to the previous six-month period, there was a 6.16% increase in total broker commission prior to business costs.

The mortgage broking industry reacted angrily last week when CommBank CEO Matt Comyn and Westpac CEO Peter King, appearing before the House of Representatives standing committee, defended bonuses paid to bank staff who serve mortgage customers.

The pair said that brokers were not subject to the same restrictions on bonuses that bank employees are, that they don’t have the same controls as bankers do, and that brokers pose a greater risk than bankers.

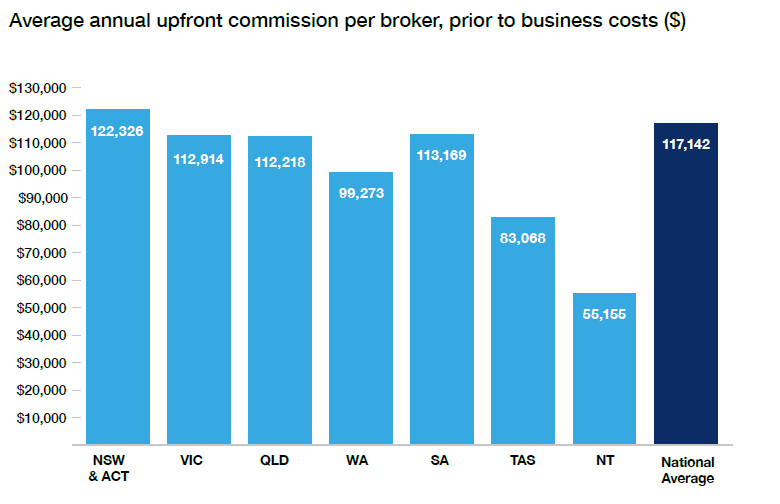

The latest MFAA report showed that year-on-year, the national average annual upfront commission (prior to business costs) per broker from April to September 2023 decreased by $6,661, or 5.38%, to $117,142.

The decrease was driven by the decline in the value of new home loans settled by brokers in the reporting period which was 3.3% lower year-on-year.

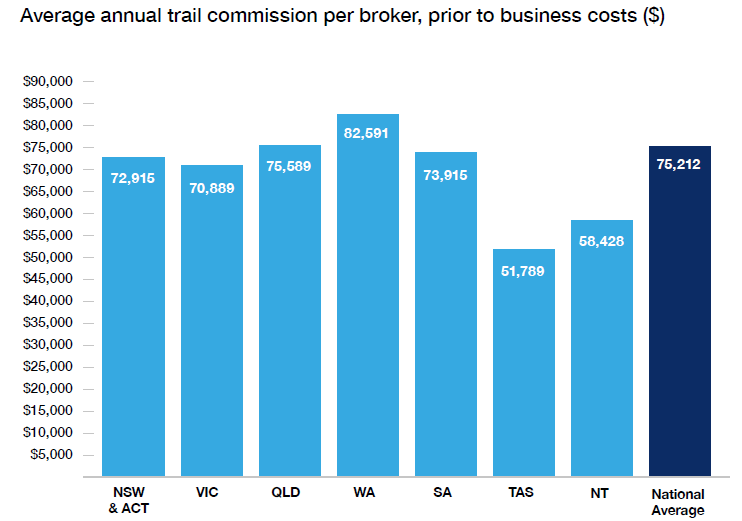

The average annual national trail commission (prior to costs) for this period increased $3,659, or 4.86%, to $75,212 year on year. Period-on-period, the national average increased $2,116, or 2.89%.

Gross commission is the total amount that lenders pay for the loan origination services

provided by brokers. Out of these gross commission figures, brokers have to pay their own salaries, all their fixed costs of doing business, premises, and fees paid to aggregators, marketing and communications expenses, support staff salaries and wages, and other costs.

Source: MFAA Industry Intelligence Service 17th edition report, April 1, 2023, to September 30, 2024

MFAA CEO’s views on broker remuneration

MFAA CEO Anja Pannek (pictured above left), said there were a number of factors that affected brokers, their businesses and business revenue overall.

She said there was a high correlation to property prices in Australia, how fiercely banks competed, levels of refinancing and home purchases across the nation.

“These factors create both risks and opportunities for brokers through economic cycles – as with all businesses,” Pannek said.

“Our latest IIS highlights average total annual commission, prior to costs, for mortgage brokers in Australia is $192,354. This is an average, and of course there is variation, across the country.

While total settlements for brokers were down 3.3% year on year, settlements for brokers in the September 2022 period were at an all-time record at over $181 billion.

“Naturally upfront commission was higher at that point in time. If you remember what the market was like then – it was very buoyant but with many brokers feeling the pressure and burn out,” said Pannek

“It’s also worth noting that average trail income – which is always a good measure of the value a broker is creating in their business – has increased by just over 5% year-on-year.”

Taking a long-term look, Pannek said average total commission for a broker increased from $151,772 for the six months to September 2020 to $192,354 in the latest report – up 27%.

“This is a marked increase – but we know this has come about with a lot of hard work and effort by brokers supporting their clients through some very challenging times.

Source: MFAA Industry Intelligence Service 17th edition report, April 1, 2023, to September 30, 2024

Economy and refinancing

Pannek said looking at the economy more broadly – many small businesses were struggling as consumers reined in their discretionary spending and looked for ways to tighten their household budgets.

“Small business insolvencies are also at record levels – we’re seeing the opposite in the broking industry.”

Pannek said the industry has just come through a cycle of unprecedented levels of refinancing. “The vast majority of brokers I speak to are extremely busy with high inquiry levels.”

Mortgage broker market share continued to grow, standing above 74%, as more Australians sought out a mortgage broker – because they trusted their broker and saw immense value in the guidance they provided.

“All of this highlights that the industry overall is in a strong position and brokers can be confident about their future,” Pannek said.

Source: MFAA Industry Intelligence Service 17th edition report, April 1, 2023, to September 30, 2024

Cashbacks and clawbacks

When it came to fairness in broker commissions, Pannek said everyone could agree that cash incentives by lenders to grab market share drove borrowers to ‘churn’ their lenders.

“Cashbacks were at levels that weren’t economically sustainable for the mortgage industry – and we can see this now with lenders reporting margin squeeze – this is without a doubt due to the lag effect of these lender cashback offers,” she said.

“We saw brokers really hurt with clawbacks through this period – I’m pleased sense has prevailed with cashbacks.”

Pannek said overall clawbacks run at around 5% of total commission revenue across the whole industry, and clawbacks had fallen from around 12% back to the more normal long-term average of 5%.

“Clawback as it’s currently structured is a source of frustration for our members,” she said. “While clawback is an integral part of the broker remuneration structure and consumer protections, I’ve been clear on the need for a fairer model.”

Pannek said she strongly encouraged all lenders to consider options to address the harsh cliff structure in place and move to a fairer model for brokers. “For example, a tiered down approach where the clawback reduces or amortises over time,” she said. “We have started to see lenders move on this – we would like to see all lenders consider this.”

Intense market competition

Given that broker market share is at a record level, MPA asked Pannek how brokers can continue to ensure their businesses grow.

Pannek said the value of a broker’s business was created through their clients and broking was fundamentally about people.

“This industry is built on relationships and brokers helping their clients,” she said. “Prioritising your client’s experience is key to the ongoing success of a broker’s business – from the moment a new client reaches out to you, how you stay in touch with them, building relationships that are lifelong.”

There were several other strategies Pannek recommended brokers could use to strengthen their businesses, and client relationships.

“First, having a business plan is essential,” she said. “Make it a habit to revisit and tweak that plan at least once a year. It’s a chance to step back, assess your business, and spot new opportunities.”

Secondly, was leverage your community – “that can be other brokers, your association, your aggregator support team,” she said.

Pannek said embracing digital tools and platforms, such as generative AI, could also really elevate the customer experience.

“Generative AI has so much potential to streamline processes, giving brokers more time to spend with their clients and enhancing – not taking over – what brokers do,” she said.

“Our discussion paper on AI released last month was all about how brokers can leverage AI in a safe and ethical way.”

Finally, Pannek said brokers should also think about how they stand out in the market – whether that’s by focusing on a specific client segment or expanding their range of services.

“There’s no one-size-fits-all approach, no right or wrong path. It’s about figuring out what works best for you and then using smart marketing and branding to highlight the value you bring to your clients,” she said.

Industry leader reacts to bank comments on broker pay

The comments from Comyn and King complaining that brokers are not subject to the same controls or restrictions on pay that bank mortgage lenders are drew sharp criticism from mortgage industry players include LMG executive chairman Sam White, the MFAA and FBAA managing director Peter White.

Also weighing in to defend brokers was Joseph Battaglia (pictured above right), the CEO and founder of diversified financial services company Aria Financial Group, which offers finance broking services covering mortgages and construction and property development finance, and includes Aria Real Estate and Aria Capital Advisory.

Battaglia, a former broker, said he couldn’t believe the banks’ stance on the issue, given “75% of their productivity comes through the broker channel”.

He said as a financial services professional and a former employee of both CBA and Westpac, he fully supported the position taken by Sam White LMG, in defending mortgage brokers.

“The notion that brokers are somehow a greater risk than bankers simply because they do not have the same restrictions on bonuses is misleading and does not reflect the reality of the mortgage broker profession or the value it provides to consumers,” Battaglia said.

“Mortgage brokers are legally bound by a Best Interests Duty (BID) to put their client’s needs first. This is a higher standard of accountability than that applied to bank employees, whose primary obligation is to their employer, not the customer.”

Battaglia said this fundamental difference ensured that brokers always prioritised the best possible outcomes for their clients.

“In contrast, banks operate under a model where their employees are incentivised primarily to retain customers within the bank’s product suite, often limiting their ability to offer a genuinely unbiased recommendation.

“Bank employees work for the bank and are therefore guided by the bank’s profit-driven objectives. The suggestion by the bank CEOs that brokers pose a greater risk ignores this conflict of interest inherent in the banking model.”

Battaglia also pointed out that despite brokers handling 75% of all new home loans in Australia complaints against brokers were minimal, accounting for just 0.3% of all complaints, according to AFCA.

“This is a clear indication of the high standards maintained by brokers and the satisfaction of their clients. Meanwhile, complaints against banks are significantly higher, reflecting ongoing customer dissatisfaction with bank services and practices,” he said.

To ensure a fairer playing field, and improve outcomes for bank customers, Battaglia suggested a number of measures, including holding banks to the same BID as mortgage brokers.

He also said that just as brokers were transparent about their commissions and were subject to clawbacks, banks should be also required to disclose all incentives and bonuses paid to employees who handle mortgage transactions.

The third step would involve independent monitoring and public reporting of complaint data for both brokers and banks.

“By making this information easily accessible, consumers can see where their interests are most likely to be safeguarded and who consistently provides the best service …it’s time for banks to step up and prioritise customers over profits, as brokers do,” he said.