Customer-owned banks continue to fly the flag of dedication to their members amid large-scale consolidation, tough competition from the majors and a complex regulatory environment

In a lush Cafe Sydney dining room overlooking the iconic Darling Harbour on a sunny February afternoon, MPA brought together six of Australia’s leading customer-owned banks (COBs) and two brokerages for a deep dive into this unique part of the banking sector.

Joining MPA were leaders from some of Australia’s premier COBs, namely Gateway Bank, Beyond Bank, Teachers Mutual Bank, P&N Bank, People First Bank and Bank Australia. Brokers from Waves Mortgage Brokers and Nectar Mortgages also took part to field questions and provide their insights into the state of the mortgage market.

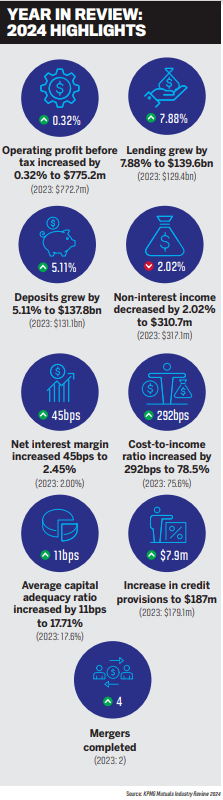

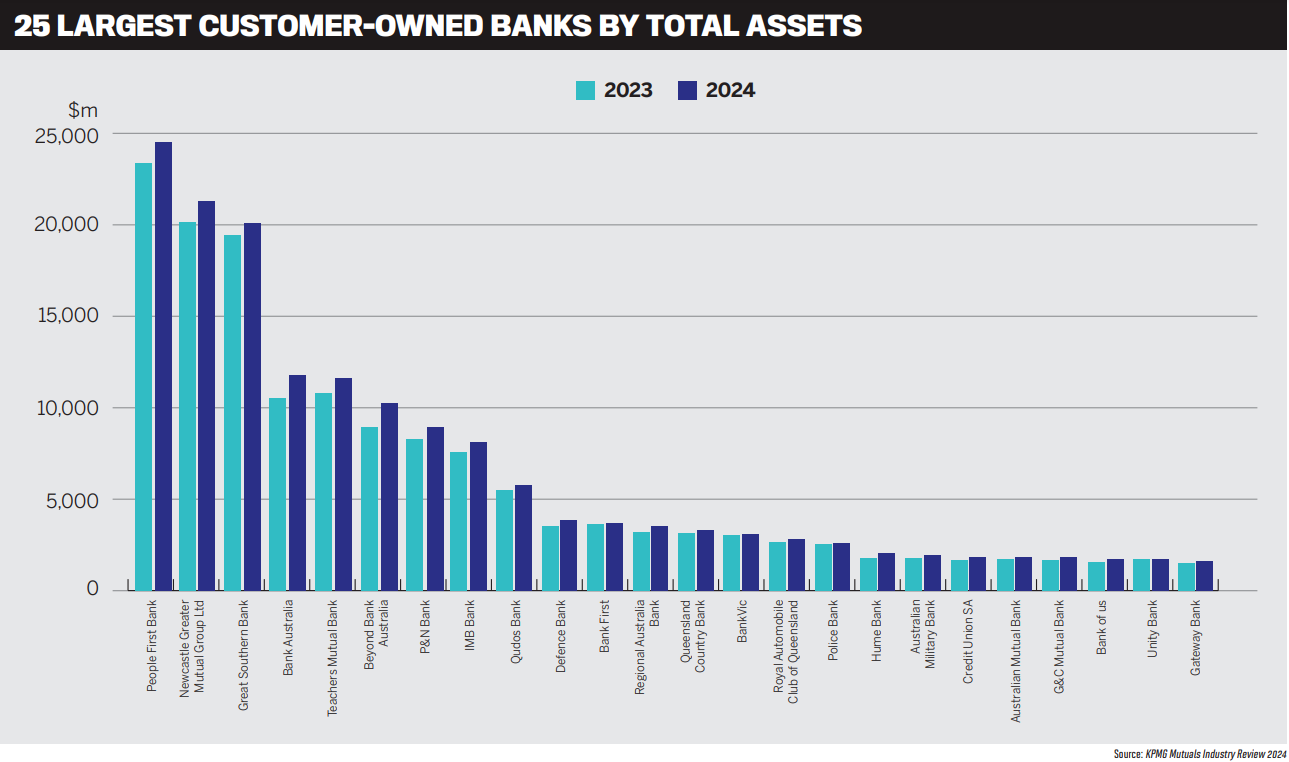

Two recently merged entities – People First Bank and Newcastle Greater Mutual Group – took the top position and second place respectively as the two largest COBs by total assets. This result provided the perfect illustration of a sector in the throes of widespread consolidation, which provided further fuel for roundtable discussion.

This was never more evident than when the roundtable participants were asked:

Q: What role is the broker channel playing in securing market share growth in 2025?

Gemma Piscioneri, head of retail distribution at P&N Bank, kicked the discussion off: “Brokers are a crucial part of ourmultichannel approach, working seamlessly alongside our branches, mobile bankers, contact centres, virtual lending teams and digital platforms. This integration ensures we can meet our customers wherever they want, providing the flexibility and convenience they need to choose how they engage with us,” Piscioneri said.

“We operate in one of the most competitive channels in banking, and we know we must listen to our customers to remain relevant. Since the launch of our broker strategy some three years ago, P&N Group has delivered a range of improvements based on broker and customer feedback.”

Mark Middleton, head of third party distribution at Teachers Mutual Bank (TMBL), continued: “The broker channel remains crucial in driving growth, as brokers connect with a wide range of borrowers and play a key advisory role in the loan process.

“There will be underserved segments that brokers traditionally haven’t focused on. From our perspective, we have many segments – whether that be the health sector or education – that we’ve catered to in the past, but I’m seeing more offerings being introduced by my competitors and the broader market. By strengthening relationships with brokers and providing transparent, consistent and competitive offerings, customer-owned banks such as TMBL will be looking to leverage the broker channel to attract customers who might otherwise go to larger banks.

“In 2025, TMBL is envisioning that our broker partnerships are expected to be a key driver for reaching underserved or niche customer segments, particularly first home buyers and refinancers.”

“In 2025, TMBL is envisioning that our broker partnerships are expected to be a key driver for reaching underserved or niche customer segments, particularly first home buyers and refinancers.”

“We’re prepared for the next flow of volume that will come with an interest rate reduction. We’ve been positioning ourselves for growth in 2025 to take advantage of a stronger market as confidence returns.

“The broker market has also helped Beyond expand into regions where we traditionally didn’t have a branch presence. We have branches across Australia, but in NSW and Victoria, where we had little presence, brokers have helped us penetrate those markets. They are now our strongest growth states, and we’re also seeing strong momentum in Queensland.”

Beyond Bank is also participating in the government’s First Home Guarantee scheme and is watching what happens with interest rates. McLeod said, “The election will also have a big impact on how these products are positioned going forward.

Michael Sancilio, head of connected channels and partnerships at recently unified mutual People First Bank, added, “What we are starting to see in areas where we haven’t had a strong brand presence before is strong interest from brokers for an alternative product to really challenge the majors.”

Bank Australia’s John Leveque, regional manager for Victoria, SA, WA and Tasmania, said brokers “are an extremely important part of our business”. He highlighted that, per the latest statistics, nearly 75% of borrowers are seeking out brokers to help them with their loans; some estimates have this figure rising to 80% by the end of 2025.

“That said, at Bank Australia there are two ways to get a home loan – through a broker or online,” said Leveque. “You can’t apply through a branch. We find that a lot of customers that apply online tend to need help, and that’s where brokers can be a great help guiding our customers in the right direction.

“The role for our team then is to make sure that the brokers are provided all the support to ensure the right products and prices are put forward to our customers.

“As I said, customers who embark online may get through it halfway, then they want to speak to someone and they can’t, so this is why the broker channel is starting to expand and why it’s becoming more important to us.” Gateway Bank’s chief operating officer, Zeb Drummond, said, “The broker channel is absolutely critical for us.” He explained that the bank’s third party channel far exceeds the market average, with 90% of all loans originating through brokers.

The latest MFAA statistics show that 74% is the current market average, although some industry experts expect that number to clock in at closer to 80% by the end of 2025. “Over time, we’ve seen this trend increase, and it’s clear that that’s the customer’s choice. We embrace that,” Drummond said. “Brokers are our partners in delivering the best outcomes for customers, which will in turn be our members.

“What we do from a niche perspective [is] to help them tap into markets that perhaps previously haven’t been tapped where you know where perhaps the majors can’t play. For example, we cater to environmentally conscious customers who don’t want to feel as though there’s a third-party stakeholder in their loan being a shareholder of a big bank. That’s a key differentiator for us.

“And that’s the stuff we need to focus on: getting it right the first time and avoiding changes or moving the goalposts halfway through the transaction. Truly listening to brokers and responding to their needs is what will drive future growth. With brokers representing customers 74% of the time, that share is only going to grow.”

A running theme throughout the afternoon’s conversation was what impact the effects of monetary easing will have on the mortgage industry. At the time of the roundtable, odds were on the Reserve Bank of Australia opting to cut the cash rate by 25 basis points at the impending February call – a forecast that proved accurate.

The RBA had undoubtedly lagged behind its global Western counterparts prior to this long-awaited rate cut. Attention has since turned to where the RBA is heading next. With that in mind, MPA asked the roundtable attendees:

Q: A light at the end of the tunnel is emerging for interest rates and borrowing capacity. How is the customer-owned banking sector priming itself for an uptick in dealmaking volumes?

Middleton said the 3% serviceability buffer has made it difficult for some borrowers to refinance, but with decreasing interest rates, new opportunities will emerge. “Potential borrowers will also be reassessing their long-term financial goals that are likely to incorporate investment property opportunities as servicing improves,” he added.

Also on the policy front, Middleton noted that the federal government is seeking to expand the Housing Australia Home Guarantee Scheme options. “These schemes have already assisted circa 44,000 people, according to the Housing Australia Trends and Insights Report. As the federal government proceeds with the share-equity scheme, it will be interesting to see how both the financial and broker industries embrace the opportunity,” he said.

No kickbacks here, but NextGen’s and Simpology’s settlement software platforms were routinely name-dropped by participants. Also apparent was the importance of robust e-sign and digital verification capabilities.

But while these technologies undoubtedly make life easier for the broker channel, there needs to be a solid foundation of business principles to build them on. As Piscioneri said, “Our focus remains on getting the basics right. That means delivering standout customer experiences, increasing our lending product portfolio based on customer demand and broker feedback, delivering consistent turnaround times and continuing to build broker relationships.

“From faster and more consistent turnaround times, upfront valuation ordering, case management, the integration of web chat, [to] increasing the size of our BDM and support teams and giving our brokers access to speak directly with decision-makers, these initiatives all form part of our continuous improvement journey, and we are committed to investing in the channel in the months and years ahead.”

Piscioneri added that P&N speaks to around 100 brokers a month, “which has led to a 95% retention success rate”.

“From our perspective,” Drummond said, “we’ve been focusing on productivity – how we can tune productivity to better service what we anticipate will be a higher volume of home loan applications. We’ve invested heavily in technology and integrations to allow systems to do what systems do well and let people do what people do best – connect process so that when discussing an application – whether it’s an approval or a decline – the broker can have a direct discussion with the underwriter responsible for their file.

There’s no handoff – it’s a single underwriter handling a single file the whole way through.” Drummond also cited a strong focus on the escalation process. “Instead of having escalations when things aren’t going right, we have an escalation process for requests to decline. A loan won’t be declined at Gateway without going up through the ranks to assess the decline reason as opposed to going up just with mitigants to approve. This ensures we don’t have broker experiences where they feel we have moved those goalposts.”

McLeod explained that Beyond Bank has spent the past year and a half working with NextGen and First Mortgage Services to get its lending procedures battle-ready. He said, “We did a campaign last year that really tested our capabilities on service, and we still managed, even though we were writing record volumes, to maintain a consistent service level of three to four days during that rate campaign. In some cases, we were able to get our docs out within 24 hours.

“So we’re sort of primed and ready for whatever is going to happen because we’ve been doing that over the last 18 months. “We’ve also upskilled our broker support team, so brokers get to deal with the same person from start to finish, so [there’s] file ownership,” McLeod added. “When a file comes in, they deal with the same support person until the application settles.

“And they’re state based, so brokers get to know not only their BDM but also their broker support team. For example, if you’re in NSW, you get to deal with someone in NSW – it’s the same people, so there’s that consistency. So yeah, we’re ready for whatever happens with rates this year.”

Bank Australia, too, has been fine-tuning the engine. Leveque said, “Similar to other customer-owned banks, we have updated our loan origination system. We’ve partnered with Cloudcase to enhance the experience for our customers and brokers, which leads to faster turnaround times. It also makes things more efficient for our lending team.

“We also know that trust remains important to consumers. Many prefer dealing with banks that exist for their customers and communities and not external shareholders.” Sancilio said, “There’s a real sense of excitement about what this year will bring for the broker market and for People First. For us, it’s very important to keep up the investment that we’re making to further improve our processes and our systems, to create a great customer experience that will drive our growth.

“By maintaining that investment in the end-to-end experience, to really focus on that, we can position ourselves as a clear alternative in the market. That will then increase how many applications we get through. We’re driving scale through a better experience, so that’s a really important element for us.”

Sancilio explained that People First is still building its technology systems following the People’s Choice and Heritage merger, “and while we’re navigating what that looks like, we have the opportunity to really leverage the benefits of increased scale and efficiencies”.

Q: What competitive edge do customer-owned banks have for securing broker partnerships against the banking giants?

The common theme of the responses was undoubtedly the tight customer experience that the COBs can provide in contrast to the majors, which are often hamstrung by onerous compliance procedures and excessive layers of middle management.

For Drummond, “it’s about focusing on niche strengths and celebrating the things that make us different”. While he acknowledged that Gateway isn’t the biggest brand in the market, “what we can do is leverage our strengths. We can move faster, adapt to technology; we can see something, hear something from the broker and adapt and change it”.

He continued: “You can change things really, really quickly in the mutual space; it doesn’t need to go through different departments and head office to make a difference and to make a change to the end member. So for me, the mutual space is critical to competition and good member outcomes, and I think also just the demonstrable effect the mutual sector has on community engagement and a sense of belonging. You bond with your customer base. That can’t be replicated in the majors.”

This sense of belonging among members was also a common theme of the discussion, and it evidently stems from the unique organ- isational structures inherent in the mutual banking space. As Middleton said, “The key differentiator for customer-owned banks is our unique value proposition. Unlike the big banks, we don’t have competing pressures from shareholders, allowing us to focus entirely on member service. There’s no conflict between maximising dividends and delivering the best products and services –we’re solely committed to our members. “Secondly, there is no bonus. Well, I know I don’t get a bonus, so I’m sure that’s the case with a lot of other people here.”

Middleton added that with TMBL and the wider mutuals sector, brokers experience reduced channel conflict. He said, “Mutuals in general don’t have the bricks-and-mortar infrastructure nationally. Of course, there are strategically placed branches that support the communities that mutuals are involved in, which ultimately assist our members, whilst [they] also align and support our broker network. Realistically this results in brokers not competing against our proprietary channels.”

McLeod brought it all the way back to the genesis of the mutual banking sector in Australia. “Credit unions and customer- owned banks were formed by like-minded people who weren’t being served by the bank industry at the time,” he said.

“It goes back to the ethos of [how] all of it started many years ago – back to the question, ‘why customer-owned banks?’ There were people that got together and decided they weren’t getting what they wanted from the financial system and market, and that’s how we started.

“So, carrying on that now many years later, that’s still to me one of our main points of difference and why people use us.”

Sancilio added: “What we’ve demon- strated over the years – and for People First that goes back 150 years – is that as a mutual we genuinely care about our customers. It’s in the People First name and embedded in everything we do.

“We can leverage that, and as was touched on earlier, size also plays a role. As a bank and as a sector, we are now big enough to make a real impact. However, we’re still small enough that we can evolve quickly where it makes sense, and that’s something we do focus on. We’re working with a lot of broker partners and technology partners so we can continue to improve.

“We may not have the massive budgets, but we deliver – that’s our commitment.”

Leveque said, “Customers like to feel like they’re part of something, and they want something different to the major banks. That’s our point of difference. Being a customer-owned bank, it’s all about customer service. We put our customers and communities first. We also pride ourselves on the type of customer service we deliver; it’s paramount as you can lose a customer as quickly as you win them.

At P&N Bank, Piscioneri said, “our customers are at the heart of everything we do. To support their financial journey, we’re committed to delivering more seamless and convenient banking experiences wherever people choose to bank with us.

For Piscioneri, this includes investing in technology and process enhancements to help deepen P&N’s customer relationships.

The roundtable also heard from guest broker Justine McDonald, franchise owner at Nectar Mortgages. McDonald wanted to know:

Q: How do customer-owned banks keep up with the budgets of the majors?

“It’s not easy,” said Sancilio. “But the important part is really making sure you invest what you have in the right areas. We’re focused on the customer and the broker. By investing in their experience, by pushing forward with that, that enables us to compete with the majors. We know we can’t spend what they do, but I think we do a pretty good job of delivering satisfaction.”

Middleton added, “The majors have significantly larger budgets, but this aligns realisti- cally to a larger customer base. They’ve got big budgets, but there’s also a lot of wastage in what they’re doing. I have worked in big banks. You do see some things that go on that don’t work out.”

He said TMBL is all about “getting the right outcome … But we’re also not the ones who are setting the way forward, so we’re looking at what’s happening at the market globally and we can see what has worked and what hasn’t worked. We can make decisions around where we do invest, but we can also leverage off what some of the other majors have done as well, which assists us in delivering at a reduced expense level”.

As an example, Middleton explained how TMBL leveraged off and implemented CommBank’s NameCheck technology “to further protect our members from scams and mistaken payments”.

“Overall, mutuals often share this kind of information, which helps us achieve cost savings while enhancing our member services. This is just one example of how we’re working to reduce costs effectively.”

Drummond said Gateway’s entire organisation is designed around the principle of “doing more with less”.

He explained: “In terms of technology, it means we don’t invest needlessly up front. Instead, we move quickly and experiment – we like to move quickly and break stuff. We try things, see if they work, and if they don’t, we scrap them quickly and move on.

“We don’t have any deadwood projects or unproductive people sitting around. If it’s not productive or it’s not delivering value for us, our brokers and membership, it’s out.”

“We reinvest our profits to offer our customers competitive rates, innovative products and exceptional customer service,” she added.

Echoing Piscioneri, McLeod said: “While we are certainly not in a position to post profit figures north of $10 billion per annum, the advantage that we have as customer-owned banks is that all of our profits are reinvested back into better services and offerings. “We don’t have that tension that exists for listed banks where decisions have to be balanced between what is best for the customer versus what is best for the shareholder. All of our investment decisions are focused solely on the customer, and they benefit greatly from that. This is reflected in many of the annual customer satisfaction awards that exist in Australian banking, where you often see customer-owned banks in many of the top rankings.”

What was evident throughout the discus- sion was that this dedication to the customer, made possible thanks to the eschewal of share- holders, truly sets COBs apart from the pack.

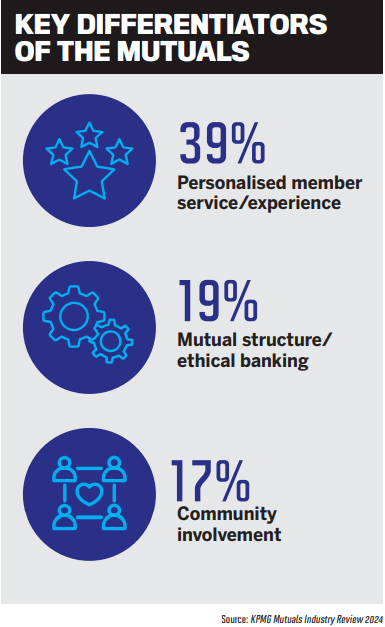

This was also highlighted in KPMG’s Mutuals Industry Review 2024 report. According to the industry-wide survey, ‘personalised member service/experience’ ranked as the number one key differentiator for the COBs compared with the majors, as mentioned by 37% of respondents.

‘Mutual structure/ethical banking’ emerged as the second key differentiator, as cited by 19% of respondents, while 17% cited ‘community involvement’.

There is no doubt that these results speak to an industry favoured by customers who don’t get the personal touch, or the ethical decision-making, from the majors. Yet no company model is without its own challenges, and mutuals are no different. COBs have a difficult balance to strike; a dual mandate that traditional lenders are not beholden to.

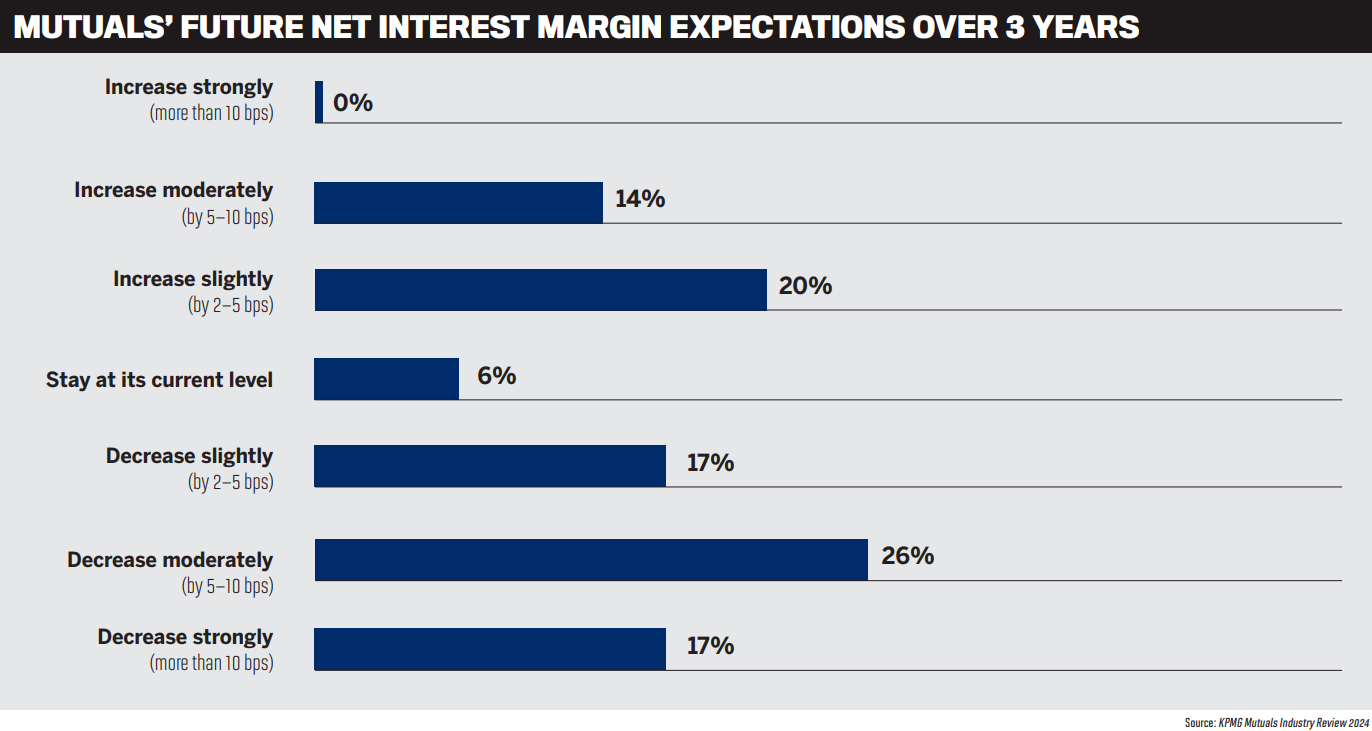

This could be particularly challenging in the coming years. Per the KPMG report, 17% of respondents in the mutuals industry expect their future NIMs to decrease ‘strongly’, while 26% expect their NIMs to decrease ‘moderately’. On the bright side, nearly half of respondents expect cost efficiency to ‘improve’ over the next three years, while 11% expect a ‘strong’ improvement.

With that in mind, MPA asked the question:

Q: Customer-owned banks are expected to balance the interests of their owners while sustaining healthyn operating margins. How are you striking this balance, and what do your customers care most about right now?

McLeod agreed that “it’s a delicate balance – finding the right level of profitability while returning value to our customers”.

“We survey all of our customers, and our satisfaction rate is 92%. A key part of that survey asks what’s most important to them. The topics that come up most are security, simplicity, easy access and having someone to talk to if they run into an issue. If customers have a problem with their banking or home loan, they want to be able to speak with someone who can help and knows what they’re talking about.”

“While having the right product is crucial, customers also need someone who can provide help when they need it,” he said.

Leveque added, “Many customers come to us because we’re values-aligned. We survey our customers and know their four main impact areas are climate change, nature and biodiversity, First Nations recognition and respect, and affordable housing.

“We know that cost of living is becoming extremely difficult, especially for first home buyers. We’re a member of all the govern- ment schemes, aiming to help first home buyers, and look to ensure that we always offer our customers the best rate possible. It’s important to us, and we talk about these values often.”

Sancilio agreed that “it’s a really hard balance” when juggling member values and the bottom line. “But the key point is that as a mutual, when we look at our operating margins, we’re reinvesting those back into our customers, who are the ones driving change and evolution.

“For example, a crucial element for us is enabling customers to choose how they want to bank with us – whether in person, at a branch, through a call centre, via brokers or online. Our goal is to deliver a consistent, excellent experience across all those channels. That’s what People First members are saying they want, said Sancilio. “And it’s how we shape our offerings. The balance is clear: we need sustainable profits, but the focus must always be on investing in what’s important to our customers.”

At Gateway Bank, striking the balance is “actually pretty simple because our purpose is ‘pocket and planet’”, said Drummond. “And that in itself is a balance. Our goal is to help Australians improve their financial situation while also supporting the planet.

“We aim to make going green more accessible, offering attractive interest rates to customers who are embarking on a green journey, whether they already have greenrated homes or assets.

“It doesn’t cost more to go green, and it shouldn’t cost more,” Drummond said. “Right now, consumers are focused on the cost of living, and we can help with that while also supporting their transition to more sustainable practices, without charging them a ‘green tax’ for doing something conscientious for the planet.”

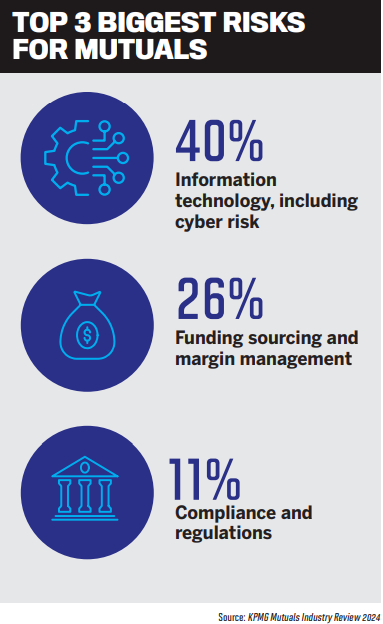

Piscioneri set a conversation in motion after mentioning that “when it comes to what matters most to our customers, the top priority we’re seeing is scams, which are becoming increasingly sophisticated”.

Indeed, the KPMG Mutuals Industry Review 2024 survey revealed ‘information technology, including cyber risk’ as the most pressing industry risk, as cited by 40% of respondents (this was followed by ‘funding sourcing and margin management’ and ‘compliance and regulations’).

Piscioneri said, “We all have a role to play to educate our customers and keep them safe, and P&N Group has implemented several initiatives as part of the Scam Safe Accord and will continue to invest in this critically important area.

“While there is a greater level of understanding of scams within the community, we do foresee the potential for increased customer friction across the industry due to the need to implement additional precautions to prevent customers from being targeted. The challenge lies in implementing additional protections without creating friction for customers in their everyday banking.”

Cybersecurity is also a prevalent concern at TMBL, with Middleton saying, “That’s why we adopted the name-checking capability as a key deliverable. Every day we’ve witnessed reports of people being scammed, and as a consequence our members’ security is a top priority. It’s crucial that we continue working on this.”

For Middleton, balancing member interests and profit margins “is achieved by focusing on efficiency, innovation and customer-centric policies. This is through investing in tech- nology to reduce costs, enhancing digital services and maintaining a lean operating model; customer-owned banks can offer competitive pricing without compromising margins and the member experience that mutuals are known for”.

While TMBL still has branches around Australia, Middleton acknowledged that they are seeing fewer visitors, while some have even closed up completely. This has put a greater emphasis on improving accessibility and service quality, particularly through digital platforms and broker networks. “We’re improving online services, including phone support, where TMBL’s call centre is highly respected by our members in addition to recognised Australian industry awards,” said Middleton.

Waves Mortgages director Andrew Diamond came in swinging with a hot-button topic that’s been an ongoing issue at his brokerage. He asked the COBs:

Q: From stamp duty exemptions to income thresholds, it’s becoming increasingly frustrating to see the misalignment of policies across both state and federal lines. What are you doing to make it easier for first home buyers entering the market, and what are some specific changes the government needs to make to help them?

For his part, Diamond had more than a few thoughts of his own to get off his chest. “I’m happy to go on the record and say that I think governments are more interested in media releases than in genuinely helping people enter the market,” he said.

“Take income thresholds, for example. Why is there an income cap for first home buyers to access these schemes? The govern- ment gave teachers a 13% pay raise last year, which pushed many of them above the eligi- bility limit. Come June 30 this year, a whole group of people will no longer qualify for existing schemes.”

Stamp duty exemptions are another issue, said Diamond. “Why are we capping them at unrealistic thresholds? Why even have a threshold for first home buyers in the first place?

“There’s also a misalignment between federal and state governments when it comes to price caps and income thresholds. There’s no clear, coordinated strategy to genuinely help people into homes. And we have to acknowledge that some of these schemes will inevitably push up home prices. You can’t have it both ways.

“There’s also a misalignment between federal and state governments when it comes to price caps and income thresholds. There’s no clear, coordinated strategy to genuinely help people into homes. And we have to acknowledge that some of these schemes will inevitably push up home prices. You can’t have it both ways.

“That said, there are things we can do better. The government needs to drive alignment across state and federal lines. I know of at least one lender that had to pull out of the market for first home buyer schemes because of the way these programs were structured on their books. It just wasn’t viable for them.”

Everyone around the table concurred that the various government schemes to get people into their first homes are simply too confusing and lack coherence across state lines. McLeod recalled a recent conversation he had with a Housing Australia representative who pressed him on what he thought could be improved, when the issue of complexity arose.

McLeod said, “The Housing Australia schemes are a great initiative, and they have helped a lot of people, but they can be complex at times, given the variety of different programs on offer. That’s why so many first home buyers go to a broker – they need guidance.

“Customers would no doubt benefit if they were a little easier to navigate and more streamlined. Take the shared-equity scheme, for example. While it’s a great idea, it’s also incredibly complex, and for brokers, the compliance and paperwork are becoming overwhelming. We need to keep these initiatives in play so that we can help more people get into the market, but if they can be simplified for all involved, then everyone will benefit.”

Sancilio added, “Simplicity is the key, but having consistency across the different assis- tance schemes is also really important. At the moment, it’s not only difficult to understand what’s required; it’s also challenging to maintain compliance with so many different programs.

“People have made the point about extending loan terms – and that’s a good discussion to have – but for me, the focus should be on consistency, to deliver a better outcome for the customer,” he said.

Regarding those loan terms, Middleton said: “The marketplace, which comprises both regulators and financial institutions, needs to be realistic about extending loan terms to improve serviceability. I believe this can occur through the consideration of extending loan terms to 40 years for potential niches such as essential service workers and first home buyers in particular. Realistically, how many home loans actually run the full 30 years?

“If we want to improve serviceability and affordability for first home buyers, we need to acknowledge that these buyers will be working beyond the current retirement age.

“If we truly want to assist these individuals with ongoing housing requirements, there needs to be a focus on the extension of loan terms, combined with equity schemes and other like programs that these segments can realistically financially service.

“The housing market today is not the same as when I purchased my first home. It’s very difficult for the younger generation.”

The roundtable concluded with an open discussion about the state of merger activity in the mutuals sector. It remains a prevalent topic considering that two big-ticket mergers have been signed off in recent years.

There was, of course, the Heritage and People’s Choice merger that resulted in the establishment of People First Bank (repre- sented at this roundtable by Sancilio) in November 2023. That same year, Greater Bank and Newcastle Permanent Building Society joined forces through a landmark merger to form Newcastle Greater Mutual Group.

But COB mergers have been going on for far longer than just a couple of years. Beyond Bank, for instance, has conducted 14 successful mergers since 1986, including two in 2024. In fact, back in the 1970s, there were some 700 customer-owned institutions in Australia. Today that number is less than 60. That is an immense rate of consolidation that could potentially keep pushing on in the years ahead.

Looking again at KPMG’s 2024 survey, 26% of respondents said they were considering the possibility of a merger, up from just 19% the previous year. ‘Mergers’ was cited as the fourth-biggest priority for the next three years, behind ‘new members and market share growth’, ‘digital transformation’ and ‘maintaining profitable and sustainable growth’.

Certainly, there was consensus around the MPA table that more mergers are in store in a highly competitive environment, which will create opportunities for the smaller players to forge ties with the big fish to keep themselves on strong footings.

Could we therefore see a drastically different line-up at MPA’s next customer-owned banks roundtable? We have a year to find out.

A closing piece of broker-side advice from McDonald: “Post-merger, it’s really important that brokers are brought up to speed with exactly what the new world looks like for the customer.”