Third party heads from leading non-bank lenders joined MPA's annual industry roundtable

Despite the challenges of a constrained economy, the value proposition of non-banks hasn’t changed. Non-bank lenders continue to offer flexible finance solutions that banks don’t provide, focusing on clients such as the self-employed and small business owners, who often don’t fit the narrow credit criteria that banks apply.

In a cost of living crisis, and with mortgage holders feeling the effects of higher interest rates, you could argue that this is where nonbanks come into their own.

Brokers working with non-bank lenders understand their value proposition and how they can assist brokers in servicing a wider range of customers beyond the vanilla. This benefits broker businesses, enabling them to provide more lending options and strengthen client relationships.

Non-banks rely heavily on their broker partners to funnel customers their way, and as the sector grows, it appears more brokers are realising the value of these lenders, boosting growth in this market.

It’s clear that non-banks compete with banks on solution rather than price, and brokers understand this. But in a competitive lending environment, which can be complex and challenging, non-banks can’t stand still. They need to constantly review their products, policies and processes to ensure they adapt and keep pace with the needs of brokers and their clients.

Turnaround times, technology and cybersecurity are all important areas that non-banks are working on. They will also need to be prepared to pivot when the RBA moves to cut the official cash rate some time in 2025.

To discuss these and other crucial matters for the sector, MPA recently held the 2024 Non-Banks Roundtable at Nobu in Sydney, bringing together third party leaders from many of Australia’s non-bank lenders, as well as Top 100 Brokers 2024 winner Stephen Michaels, managing director of Catalyst Advisers.

Participants included Jason Arnold, group executive – origination, Pallas Capital; Cory Bannister, senior vice president and chief lending officer, La Trobe Financial; Royden D’Vaz, general manager distribution and partnerships, Assetline Capital; Tim Lemon, national sales manager, MA Money; Tony MacRae, chief commercial officer, Bluestone Home Loans; Chris Paterson, general manager distribution, Resimac; Lee Prior, director of distribution, ORDE Financial; Barry Saoud, general manager mortgage and commercial lending, Pepper Money; David Smith, chief distribution officer, Liberty; and Belinda Wright, head of partnerships and distribution, Thinktank.

How has the non-bank sector adapted to changing economic conditions over the past 12 months? What have been the key challenges and opportunities for brokers and their clients, and how have you worked with them?

MacRae said it has been an interesting period in the non-bank sector because as the economy has changed, more customers are now falling outside the traditional bank space, providing more opportunities for non-banks.

“At Bluestone, we’ve seen it as a wonderful 12 months of opportunity where we’ve been able to work really closely with brokers, not product flogging but educating in the non-standard space, including near prime, specialist and SMSF lending, to help brokers actually grow their business,” MacRae said.

Bluestone looks at the economic circumstances as an opportunity to push itself forward. “We think the market that falls into the space that we specifically cater for is growing, and being able to provide solutions has seen us significantly increase our volumes over that 12-month period.”

Prior said the changing economy and trends in customer engagement have highlighted an opportunity to further support brokers with more proactive, rather than reactive, strategies.

He said previously brokers were understandably focused on responding to customer needs, such as requests for more competitive rates and cashbacks. However, after that initial focus, economic changes slowed that growth.

“We’ve got a segment of brokers that have had a reduced need to rely on proactive strategies,” said Prior.

“While the changing economy does have its challenges, there’s also a lot of opportunities for brokers who can successfully navigate this period. ORDE is focused on providing brokers with the support and education they need to better service their clients and grow their business. That means support not just with products and customer engagement but with referrers and internal processes as well.”

D’Vaz said he believes the current challenge for brokers is not high interest rates or the housing market but more informed customers with higher expectations, which some would say are unrealistic.

However, “for them [customers], those expectations are not unrealistic,” he said. “For a broker, just sticking to one product is not enough any more. Diversifying and broadening your expertise and exploring a full range of opportunities is what’s needed to stay competitive.”

D’Vaz said all non-bank lenders around the table were trying to enhance their offerings and improve policies, given that brokers have access to so many lending options.

“If you look at our business [Assetline Capital], we’ve been one of the leaders in that short-term development and construction space, but we realise that we have to keep moving and be dynamic and agile and offer more solutions for the brokers.” He encouraged brokers to diversify.

Picking up on D’Vaz’s comment about customer expectations, Michaels said what he wants to do is keep striving forward. He gave the example of a customer who had banked with a major bank for 10 years but had not received the credit answer they wanted from the bank, despite being in a good, creditworthy financial position.

“If you don’t have that option in your toolbelt where you can tell them, ‘now we’re going to our mid-tiers and our non-bank lenders’, then you’re just going to be left behind,” said Michaels.

Previously, Catalyst Advisers brokers would catch up with referral partners for lunch, and “you would just shake the tree and deals would fall out”, but now there had to be a specific reason behind the conversation. “And that reason might be, I spoke to you six months ago, and I couldn’t help that client out. Now we’ve got a different non-bank that can provide that solution that wasn’t there six months ago.” Michaels said.

“Non-banks give us a reason to, a, keep servicing our clients, but also, b, a reason to keep servicing our referral partners too.” Diversifying is key for brokers in the construction space, Arnold said. Cost increases have made it a particularly tough market for development finance.

“Valuations have come off in certain segments, cap rates have softened, builders have fallen over, so we’ve never worked more closely with our broker partners,” he said. This includes working through issues such as when feasibility don’t stack up on building projects.

Arnold said that for those brokers looking to diversify away from the banks, needing extra leverage, such as senior and mezzanine finance as well as lower presales, the non-bank sector offers that diversity. “That’s something that will help brokers offer more options to their clients.”

Bannister argued that not a lot had changed in the last 12 months. “In my view, if you’ve only just adapted to current market conditions recently in the last 12 months, you’ve missed a significant opportunity,” he said.

“The market dislocation started off three or four years ago around COVID time, and it’s been the perfect market for a non-bank for a whole host of reasons.”

Bannister said the opportunities for nonbanks had started when banks “pulled in” when it came to finance. “That’s our traditional market. In the last three years, our addressable market has increased significantly on the back of that.”

For non-banks and brokers, it was not about adapting in the last 12 months but continuing to show their value propositions.

Bannister agreed that there were more brokers attempting to use non-banks for the first time, but 80% of La Trobe Financial’s business came from brokers who had discovered the benefits of using its services a lot longer than 12 months ago.

Saoud said, “The non-bank sector plays a vital role in the Australian financial system, fostering financial inclusion in a market where the real-life needs of borrowers are not always met by mainstream banks.” He said he had seen a continuous improvement in the market for non-bank lending since COVID.

“There’s been a strong continuation of the changing demographics of your traditional borrower,” Saoud said. “For us, it’s all about a purpose-led solution. How do we continue to fill the gap where the banks aren’t? How do we continue to innovate in the space – whether it’s through our product, through policy, service or experience?”

Pepper Money, like other non-banks, wants to maintain an agile nature as a competitive advantage – developing products, working with brokers, understanding the gaps and providing holistic solutions.

Prior said experienced brokers had seen their businesses continue to grow in the post-COVID period, but the last 12 months were an opportunity to stop and reflect on their business and make some changes.

“That’s an area where we have supported brokers. We [ORDE Financial] are working with a couple of big groups on how we could help them speak to their referrer networks about valuable new opportunities or solutions that have become available since the last time they were in contact,” he said.

Smith said Liberty had seen a significant number of new brokers sending business its way.

“The focus for us in recent times has been education – responding to that first-time broker user,” he said. “It means that the sales conversation out in the market is a longer but a deeper conversation, rather than, as Stephen says, shake the tree and the deals will come; now it’s an education conversation.”

D’Vaz said the onus is also on the broker to find out more. “We’re providing the platforms for them to come and learn, and trying to get them to do that can be difficult. We can enhance our products, policies and pricing, but they’ve got to be proactive.

“They need to say, ‘I want to diversify my proposition; I want to learn more. What are you guys offering?’ They’ve got so many options and so much choice now.”

Smith said that because non-bank deals are often less frequent for brokers, the challenge is to maintain visibility and recall. “We have to work harder to stay front of mind like a major might for a straightforward deal.”

MacRae said Bluestone has seen a rising appetite for brokers wanting to learn and diversify. “We’ve seen what we call active brokers double in the last 12 months.”

Since Bluestone launched SMSF lending about 18 months ago, more than half of the brokers that had written SMSF loans with the non-bank had not written deals with Bluestone previously. “All of those, on average, have brought us another non-SMSF deal, so they are expanding and using it as entry points,” said MacRae.

Wright said diversification had been around for a long time, but there had been no change to “how we talk about commercial and SMSF”. She said she was aware of this, having worked in the residential space for 22 years and then moved into commercial and SMSF at Thinktank.

“At first, commercial may seem complex, but it’s simply a self-employed loan with a different type of security, while SMSF has become a straightforward, repeatable loan product to access. Once we break it all down and explain it, brokers quickly grasp it,” Wright said.

“That’s why we’re focused on broker education, changing the way we communicate with brokers, demystifying SMSF and commercial and really helping them along that journey.”

Lemon said five years ago when talking to a broker, most of them would say, “I don’t write non-bank”.

“Today, it would be very hard to find a broker that would say, ‘I haven’t written a non-bank deal in the last 12 months’,” he said. ‘That’s probably the best part for all of us.”

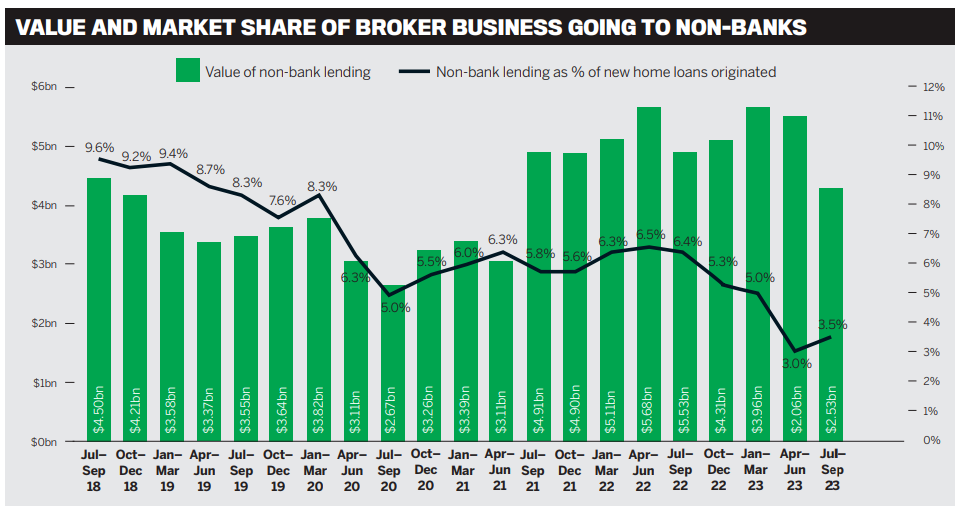

The MFAA Industry Intelligence Service’s latest report shows that non-bank market share was up 0.5%, rising to 3.5% for the quarter, but the value of non-bank loans fell by 19.6%. From your own data and observations, how are non-banks faring when it comes to competing with banks for broker share of loans, and how are you differentiating your offering in terms of products, pricing and service to brokers and clients?

Paterson said it’s important for non-banks to have diverse options, such as product niches, policies and serviceability criteria, that can help secure finance to meet customers’ needs.

“There are more customers falling outside the square [of banks], and as a broker, if you can educate and provide a solution, there’s more competition in the non-bank space than there ever has been,” he said.

“There’s a lot of different options for brokers and customers to consider, and I think that’s where non-bank growth will continue to come – writing those products and policies that the banks don’t.”

Prior said it was difficult to quantify and compare ORDE Financial’s data compared to the MFAA’s findings, as the company has seen positive growth since its launch four years ago. Since 2020, ORDE Financial has settled around $6 billion and is still in a growth phase, with broker use and volumes increasing.

As a new entrant to the market, Pallas Capital’s growth over the last few years has been significant, Arnold said. The non-bank has enjoyed good brand awareness among brokers and has also ensured its products and pricing are flexible enough to attract brokers.

Bannister said the first point to make about La Trobe Financial was that, like other non-banks, it doesn’t try to compete with the banks. “We know where we sit in the market – we target those overlooked or underserved niches,” he said.

The total addressable market for nonbanks has increased significantly, and there are a few reasons for that, Bannister said. These include regulations on banks, and banks choosing to go after automatable mortgages.

While non-bank lending volumes at the top-line level might have fallen, this is market-driven, he said.

“It’s been a pretty quiet period in terms of sales and purchases in the market over the last 12 months,” Bannister said. “We’re at the peak of the rate cycle; people’s hands are in their pockets, but I think generally, as a proportion, non-banks are certainly doing well.”

D’Vaz said the MFAA figures don’t quite match what is happening. “Looking at the non-bank sector, I think we do a pretty good job. We’ve got a very high-touch strategy – the BDMs do a great job of getting brokers engaged and hold their hands and walk them through the process and workshop a deal.

“We don’t ever compete with the banks; we don’t want to. What we do, we do it very well.”

Smith said the MFAA provides a lens into the sector, but perhaps not the widest of lenses. The non-banks represented at the table were a diversified group, competing across a wide range of asset classes.

“If you look at that fuller picture, I’d say the share of voice that the non-bank sector has claimed over the last 12 to 24 months would have increased much more significantly than half a per cent,” Smith said.

Bannister said non-banks also increase the size of the pie available for mortgages written in Australia. “Without the non-banks writing what they write, the pie just shrinks.”

La Trobe Financial is not interested in shifting the pie by heading to a broker’s office and asking what other non-bank lenders are doing and trying to claim a slice of that. Instead, Bannister said it is laser-focused on that’s where your competitive advantage lies,” Arnold said.

At Thinktank, it’s all about understanding the customers it serves, 95% of whom are selfemployed, Wright said.

“It’s about listening to brokers to innovate with products and enhance our policy. When you’re working with self-employed people, it’s about understanding that they all have unique circumstances and needs, and being able to offer that broad range of solutions, whether it be commercial lending, SMSF, residential or our latest private lending offering … and delivering service for the broker as well.”

Lemon said MA Money also focuses on technology – to make sure brokers provide an answer to the customer as quickly as possible. And it’s important to look at postsettlement services, such as internet banking and free features that can be offered to ensure customer retention

“The longer that customer stays with you, the happier the broker,” he said. Prior said non-banks should also focus on talking to brokers about products or services that are missing and what gaps they can fill. “Education has been spoken about, but it comes back to experience,” he said. That means non-banks having the “right people taking the right phone calls and sending the right emails” to ensure that brokers are aware of the difference between non-banks and the banks.

Michaels highlighted some of the ways non-banks do things differently from banks, especially as one in 25 deals is a non-bank deal. He said the service brokers receive from non-banks is completely different to that of the banks. “It’s because non-banks appreciate that you are having to deliver a service before you then deliver a loan product.

Non-banks market their products in a more personable way than the big banks, Michaels said. “As a broker, you feel like you’re actually dealing with a human being.”

With banks, relationship managers change often, creating a lack of consistency. “As soon as you submit your deal to the bank, you lose all control,” Michaels said. “It’s the scariest thing in the world when you hit submit.”

Conversely, with a non-bank such as MA Money, he said he had known Lemon and written deals with him for 12 years and knew what to expect, compared with a bank BDM he had never met.

Paterson said the strength of non-banks’ BDM teams helps brokers. “Resimac’s view is to help a broker grow their business. We spend time with them getting an understanding of their business and customers. Our BDMs support and educate when it comes to writing that next loan, streamlining the application and credit experience, helping brokers to spot applications likely to get approved or not.

“But also, if they’re faced with a hurdle, the BDM often goes in to bat for their broker.”

Smith said, in answer to Michaels’ question, it was important to note that what the market saw as non-traditional lending a few years ago, and sees now, could become mainstream tomorrow and vice versa. The employment economy is shifting so rapidly that non-banks need to adapt.

He said Michaels will be seeing different customers now to the ones he saw five years ago. “There used to be a quarter of a per cent of the economy represented by those customers, and now there’s 10 times that, and in a couple of years’ time it’ll be five times that again.”

Michaels said he always tells his Catalyst team that, due to the changing nature of rates, policies and property markets, if they are using the same sales pitch and approach to a client that they had used three months ago, it will be stale.

Customers are also changing how and when they communicate, with Michaels’ clients preferring WhatsApp to emails. “I’m taking phone calls at 8.45 p.m. at night because our clients are really busy professionals. You’ve got to just shift with your customers.”

Brokers need to be dynamic, shifting with the changing market and serving customers’ needs accordingly, Michaels said.

He pointed out that, as a Catalyst broker, he has more in common with non-banks than banks. “Non-banks are thinking, ‘I want to be customer-focused, I want to be agile, and I want a service where no other lender can service’ – that’s a broker; you might as well be a broker.”

Prior said this was the second time he had heard a broker compare their own business to a non-bank’s.

How are you investing in technology and AI to improve credit decisioning, loan processing and turnaround times? What role does broker feedback play in improving tech and your overall offering?

Lemon said that, in response to broker feedback, MA Money had invested heavily in technology to make sure turnaround times were as quick as possible. Its use of AI is in its early stages, but this will ramp up in 2025, with MA Money focusing on data collection and storage.

“We know that feeding AI with the right type of data is most important … so that when we do roll out [in the] AI world, we’re better equipped,” Lemon said.

D’Vaz, who has been in the non-bank sector for a number of years, said he had a different view when it came to technology.

“We differentiate ourselves with the human element,” he said. “I think it’s important to have both. We are constantly improving and building our technology offering, but that human element is what makes us different.

We look at every deal on its merits, individual characteristics of the borrower, how can we make this into a deal? No matter what data we feed into our technology platforms, you’re not going to replace an assessor looking at the deal.”

Wright said it was about balancing people and technology. “We’re looking at what technology we have now or upcoming that can provide our customers and brokers outstanding service and how that can complement the incredible people we have in our business.

While there is a lot of focus on tech in the residential space, Wright said the commercial process also needs attention, especially if nonbanks want to see more residential brokers diversifying into commercial lending.

“We’re in the process of a deep dive on how we take learnings from the residential side of the business and implement those into the commercial and SMSF parts of the business to make it easier and faster for brokers to do business with us.”

Wright added that the feedback from brokers was that by giving commercial business to banks instead of non-banks, they could also lose the client when it came to residential loans.

Arnold said there were big opportunities for non-banks to use AI and process-driven systems implemented in the smaller SME non-construction space, where standardisation could occur.

Pallas Capital’s strength, when working with large construction projects and pre-development products, is in providing bespoke, dealby-deal tailored solutions managed by skilled staff, he said, because those transactions can be particularly tricky. He added that using AI was a long way off for structured finance and senior mezzanine transactions.

Wright said that as an industry we should be looking closely at the amount of customer data being communicated via email, in terms of security.

Saoud agreed that it was all about balance, with non-banks growing due to the human connection. In its approach to technology, Pepper Money considers the most important touchpoints that brokers and customers value. That means looking at the human elements that need to be maintained and leveraged, such as credit assessments and engagement between credit and brokers, and using technology to automate or leverage AI to support efficiency and process in non-value tasks.

“We believe that brokers want confidence and certainty in that credit assessment process,” said Saoud.

MacRae said Bluestone had been on a journey for the last 12 months, with the first part known as “eliminate and simplify”.

“There’s no doubt we asked for too much information, and our processes were too complex,” he said. “So we spent about six months just stripping that stuff out, and that’s allowed us to more than halve our turnaround times.”

Bluestone is about to embark on the digitisation process, re-platforming its origination system in partnership with companies that provide AI solutions. “That will allow us to make quicker ‘yes’ decisions,” MacRae said. “What I don’t want to do, though, is lose the relationship element of our business because, at the end of day, we’re all in the relationship business.”

The goal is to automate, providing almost instant decisions for about half the non-bank’s loan deals. MacRae said data would be used to make better decisions but not to make quick ‘no’ decisions. “We’ll always look at the individual deal and assess it ... it’s fundamental to how we really differentiate ourselves in the marketplace, because the banks will have their 10-minute mortgage, but we’ll find the solution for that complex customer.

Smith said it would be difficult to find any financial services business that was not actively investing in technology, digitisation or AI. “We are entrusted with more data than just about any other industry, apart from maybe medicine … you can use that to harness what Tony’s alluding to, which is intelligent conversations.”

Broker feedback is crucial, Smith said, and all non-banks listen to it, but this feedback can also be gained en masse in data form. “You can leverage that for intelligent conversations with your broker partners, for your sales team to be better equipped to have a quality conversation. Secondly, you can use it to clean out the ‘$1 tasks’ from valuable humans’ working day, so that they can have the ‘$1,000 tasks’ in their in-tray.”

Prior said everyone was on the same page – it’s not about taking human interaction away but allowing more time for the people who need to talk a broker.

The digital team at ORDE Financial is the lender’s third-largest team, and the focus remains on providing fast solutions to brokers, Prior said. “If SLAs aren’t up to speed, if we’re making it difficult, then brokers will walk, and technology plays a critical role in this.”

Paterson said brokers and customers have a base framework of digital functionality that they expect businesses to use as a minimum. “If you don’t continue to evolve your tech, you’re going to get left behind fairly quickly. And what comes with that is continuous process review to improve efficiencies, speed to yes, those little bits of admin that frustrate brokers and customers.”

With brokers, it’s all about having the confidence that they can move on to the next deal, Paterson said, while customers want to be able to bid at an auction or get that property squared away.

At Resimac, digital functionality, process efficiencies and reviews and broker feedback all play key roles, he said. “We send brokers surveys monthly, and we capture that data across a number of different things – BDM activity and responsive time performance, credit assessment process; those sorts of insights and research are invaluable too.”

Wright said brokers were generally very candid in providing feedback. “They will tell you what you’re not doing well, and you can find common themes if you spend some time on the road with brokers. It’s great to know where we’re doing really well but also need to know where we must improve.”

Michaels said that as long as any project fed back to the customer, it was a good project. Some businesses have cool, high-tech ‘gamified’ interfaces for customers to enter data.

“The customer doesn’t want that,” Michaels says. “The customer wants an answer, and they want confidence to get to wherever they’re going.”

A fantastic technology investment gives salespeople more time to go out and see brokers and brokers more time to educate their referral partners and clients, achieve outcomes for clients and service their referral partners. “Keep drawing that line back to customers, and I think you’ll continue to do an amazing job in delivering that awesome service,” said Michaels.

On a different note, Bannister said one topic that hadn’t been discussed was cybersecurity. “A sizeable part of our tech investment now relates to cybersecurity and making sure that it’s as robust as it can be.” He said Wright had spoken about the security of PI data and the number of PDFs “that fly around” the industry between brokers, offices, customers and lenders, which puts the industry significantly at risk.

“The financial sector is the most targeted area for cybercriminals and cyberhackers. And the stats that you see come out of ASIO about the levels of attacks on Australian business and financial services is eyewatering, and it’s a real worry for all of us.”

Bannister said lenders are investing a lot of money in reallocating tech resources towards cybersecurity “to ensure we are as protected as we can be”. He pointed to recent examples of businesses that had been hacked, which put them offline for a considerable period, meaning they were unable to take calls and lost access to customers’ loan balances.

Equally important is protecting brokerages, putting in place secure portals to upload documents, said Bannister.

What will happen to non-bank lending activity when interest rates eventually start falling, and how will you pivot to this new environment?

Arnold said the answer was continued growth because nonbanks did not compete headon against banks on rates. “It’s flexibility, policy; it’s customer service, it’s efficiencies. There’s plenty of growth. If you compare Australia to rest of the globe, we’re still well behind, but we are catching up more recently when it comes to the nonbank sector.

“International investment into our non bank sector is stronger than ever. It’s a signal that there’s increasing interest and attention on Australia globally. Other players are waking up to the potential for growth here.”

MacRae said he agreed absolutely about not competing with the banks. “We don’t compete on price; we compete on solution. The economy and people’s employment habits will continue to change. We see more and more customers fall out of the mainstream, and, as long as we focus on solution first, the last conversation we ever have is price.”

Michaels said customers would become accustomed to rates that started with a six from a nonbank.

Customers for the last 10 years had only known rates that had gone down, exacerbated by COVID. “Everyone in this room probably knew that a 2% rate was not normal, but a lot of consumers didn’t know that.

Clients who had been used to a sub3% rate from 2019 are now shocked by interest rates that are double that.

“As soon as rates start to come down, the rates that are charged – which is the perceived risk of going outside of the box to find that solution – will just become more palatable,” Michaels said. “And it would be an even easier conversation to say, this is the right decision because of x, y and z.”

MacRae said this puts a real onus on non banks to work closely with brokers to help educate customers. “You’re right – consumers’ expectations will shift. I’ve got an entrepreneurial mate that has had a business for 12 months and thinks he should be getting a loan to buy a property in Sydney with a five in front of it.

“I told him he’s never going to get that, but the opportunity cost of waiting for two years to try and get something is huge.”

At Thinktank, more funders mean being able to increase loan limits, said Wright. “Brokers have said, ‘if you had this and this, you capture the market’.”

Having access to funds overseas helps keep the nonbank ahead of the banks. Wright said it means moving faster, meeting customers’ needs and helping brokers where there are gaps and traditional banking options aren’t available.

Wright said these funds are also being provided a lot more quickly than in the past.

The reduction in banks’ cost of funds is also good for nonbanks, said Arnold. He agreed there is more interest in nonbanks from funders offshore, and this would continue as nonbanks continued to grow in Australia.

“Recently, Pallas Capital dropped its rates by 50 to 70 basis points outside of any RBA movement. This is a result of consistent growth in our loan book over a number of years and a lot of work behind the scenes between our product team and our institutional capital partners to ensure we are continually providing brokers with one of the most competitive nonbank products in market,” Arnold said.

“It’s a good time to seek funding at the moment,” said MacRae. “Locally and internationally, the markets are keen to do business with people like ourselves.”

Lemon said 10 to 20 years ago, nothing ever changed when it came to loan policies and maximum loan amounts. “I remember maximum loans at $1.5 million for a long, long time in that nonbank space, and how quickly in the last three years it’s gone from $1.5 million, $2 million to $5 million.

“The next three years, there’ll be changes at breakneck speeds. It’s going to be very exciting, and we’re all going to benefit.”

Wright said it was important to keep brokers updated by having people out on the road having the right conversations and helping brokers build their businesses.

Michaels said the banks, particularly the big banks, have kept their margins on loans quite tight, and as the cost of funding and the cash rate come down, they probably won’t be able to offer such shiny, attractive rates to customers.

“Nonbanks are going to stay strong in that particular tickbox, because you don’t have to compromise.”

Wright said many customers get annoyed when the banks don’t reduce their rates in line with the cash rate. “We’re regularly hearing that the sentiment isn’t great with the largest players, so it’s an opportunity for us as nonbanks to talk to those customers about how we can help them.”

Bannister said it will be interesting to see what happens when interest rates start to fall. “Interest rates in isolation are not perfectly correlated to non-bank lending activity; in fact, we don’t compete on price and instead target underserved niches, so rates alone are unlikely to materially influence loan allocations.

“However, as rates start falling, we think market activity will increase as buyers that have been sitting idle become active quite quickly; you could also see borrowing power increase, which will be helpful, so there are some bright prospects ahead.”

Smith said that if a mild reduction in the cash rate were to occur, this would be positive because it would stimulate the purchase market. “But if we see a more substantial move from tightening through neutral into easing, that’s an orange light on the dashboard for every industry, because there’ll be an underlying driver as to why the RBA has moved to easing.”

The goal should be long-term stability, which is the RBA’s core mission, Smith said. “The consumer media’s focus on ‘everything will be fine when rates are all cut’ is not constructive and not well informed, but it’s what all of our respective customers are exposed to across a range of media all the time.”

The ideal is a middle ground that provides profitability and sustainability and an opportunity for a good level of lending activity.