Nearly 30% of mortgage holders now "at risk"

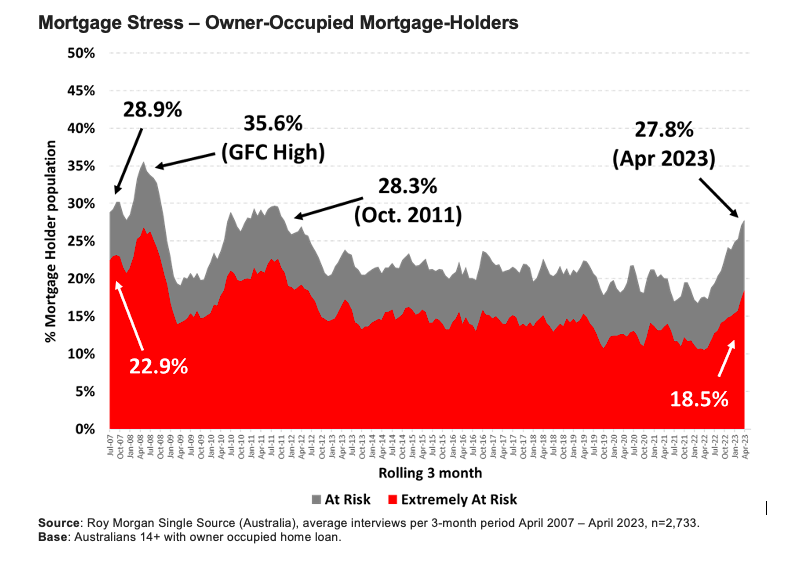

Mortgage stress in the Australian housing market has continued to increase with an estimated 1.38 million mortgage holders (27.8%) considered “at risk” in April – up 10.2% on a year ago before the Reserve Bank started its record-breaking series of interest rate hikes, Roy Morgan reported.

The April quarter saw the highest number (1.38 million) and the highest proportion (27.8%) of mortgage holders considered “at risk” since August 2008 and October 2011, respectively.

“The figures for April 2023 take into account the ten straight RBA interest rate increases which lifted official interest rates from 0.1% in May last year to 3.6% by April,” said Michele Levine (pictured above), Roy Morgan CEO. “Although the RBA did leave interest rates unchanged at their meeting in April, they subsequently increased interest rates again in the first week of May to 3.85% – just before the Albanese government’s first federal budget.”

Despite the sharp rise in the level of mortgage stress over the last year, it was still below the 35.6% (1,455,000 mortgage holders) recorded during the global finance crisis in early 2009 – although the level is set to be reached with further interest rate increases.

The three months to April 2023 also saw the number of mortgage holders identified as “extremely at risk” jump to 881,000, or 18.5% of mortgage holders, which was considerably more than the long-term average over the last 15 years of 661,000 (15.9%), Roy Morgan reported.

Roy Morgan considers mortgage holders “at risk” if their mortgage repayments are greater than a certain percentage of household income – depending on income and spending. Mortgage holders are considered “extremely at risk,” on the other hand, if even the “interest only” is more than a certain proportion of household income.

Mortgage risk to rise if RBA hikes rates in June

With the latest ABS CPI figures for April showing an annual inflation rate of 6.8% – well above the target rate of 2% to 3% – there is a fair chance that the OCR, which sits at a decade high of 3.85%, will rise by 0.25% in June, and perhaps by another 0.25% again in July.

“If the RBA does raise interest rates again next week by 0.25%, Roy Morgan forecasts mortgage stress is set to increase to over 1.4 million mortgage holders (29.2%) considered ‘at risk’ by June 2023,” Levine said.

“Of even more concern is the rise in mortgage holders considered ‘extremely at risk,’ now estimated at 881,000 (18.5%) in April 2023 – the highest for over a decade since October 2011 (21.4%). This is an increase of over 400,000 mortgage holders from a year ago (+8% points).”

If the RBA lifts rates by a further +0.25% in July to 4.35%, the proportion of mortgage holders “at risk” will increase by 2.4% to 30.2% (1,455,000 mortgage holders) in July, Roy Morgan’s modelling found.

Key factor on income and mortgage stress

There are other variables aside from interest rates that determine whether a mortgage holder is considered “at risk” – and the variable that has the largest impact is directly related to employment. After all, a person, or household’s ability to pay their mortgage is significantly impacted if they lose their main job or source of income.

“The latest figures show rising interest rates are causing a large increase in the number of mortgage holders considered ‘at risk’ and further increases will spike these numbers even further,” Levine said. “If there is a sharp rise in unemployment, mortgage stress is set to rise towards the record high of 35.6% of mortgage holders considered ‘at risk’ in May 2008 during the global financial crisis.”

The good news though, Levine said, is that the latest Roy Morgan employment estimates showed a record 13.8 million Australians were employed in April – that’s up by more than 600,000 from the same period in 2022 “indicating the strength of the labour market over the last year despite the RBA’s series of interest rate increases.”

Use the comment section below to tell us how you felt about this.