Customer-owned sector’s asset growth slows, but profits rose 27%

Australia’s mutual banks, building societies and credit unions, recorded a combined increase in lending of 6.1% to $129.4 billion, according to the KPMG Mutuals Industry Review 2023.

The KPMG report, released on November 23, also shows the mutuals sector, increased its total assets by 2.5% to $163.1bn in the 2023 financial year.

This compared favourably to last year’s 8.4% jump to $159.1bn.

The review of the customer-owned banks also showed overall operating profits before tax increased by 27% to $769.3 million, a turnaround from 2022 when they fell 18.1% to $605.7m.

Mutuals’ lending grew as it coped with ‘mortgage cliff’

According to the report, lending grew by 6.1% to $129.4bn, up from 2022 when it was $121.9bn, while deposits grew by 4.4% to $131.1bn having grown from $125.6bn in 2022.

KPMG national sector leader, mutuals, Darren Ball (pictured above) said many of the sector-wide challenges that the mutuals had been facing, such as the need to continue to invest in digital transformation, innovation and meeting the increasing regulatory compliance, whilst true for all banks, continued to impact the mutuals disproportionally due to their relatively small size.

“Despite this, it has been a positive year for the mutuals sector,” Ball said. “By and large, the sector has navigated the impact of the ‘fixed rate mortgage cliff’ with the first wave of fixed rate loans from 2020 and 2021 needing to be refinanced.”

“This has not had a significant impact on loan performance this year, however the concentration of residential lending within the sector means that this will continue to be a focus into 2024.”

According to the review, the increase in operating profits before tax was largely driven by the impact of increased interest rates and the flow through impact on net interest margins (NIM) as well as continued loan growth.

This has had a positive impact on the mutuals’ cost-to-income ratios which for the sector as a whole decreased to 73.7%.

The last three years have seen unprecedented disruption for the mutuals, from the impacts of COVID in 2020 and 2021 to the impact of the climate-weather events in 2022.

The KPMG report said these challenges continued into 2023 with softening economic conditions, high inflation levels contributing to further interest rate increases and the cost-of-living pressure continuing to have an impact on customers.

Key financial results for the mutual sector for the year are:

• Net assets increased by 4.2% to $11.7bn (2022: $11.3bn)

• Operating profits before tax increased by 27% to $769.3m (2022: $605.7m)

• Lending increased by 6.1%t to $129.4bn (2022: $121.9bn)

• Deposits grew by 4.4$% to $131.1bn (2022: $125.6bn)

• Non-interest income decreased by 17% to $317.1m (2022: $381.8m)

• Net interest margin increased by 18 bps to 2% (2022: 1.82%)

• Cost-to-income ratio decreased by 749 bps to 73.7% (2022: 81.2%)

• Average capital adequacy ratio increased by 204 bps to 18.25% (2022: 16.21%t)

• Increase in credit provisions of $23.6m (2022: writeback of $10.8m)

• Two mergers completed (2022: 2)

The report stated that the mutuals continue to remain positive in the face of ongoing market and economic uncertainty, with 73% of survey respondents revealing they feel confident in their three-year growth prospects.

Consolidation a hot topic for mutuals

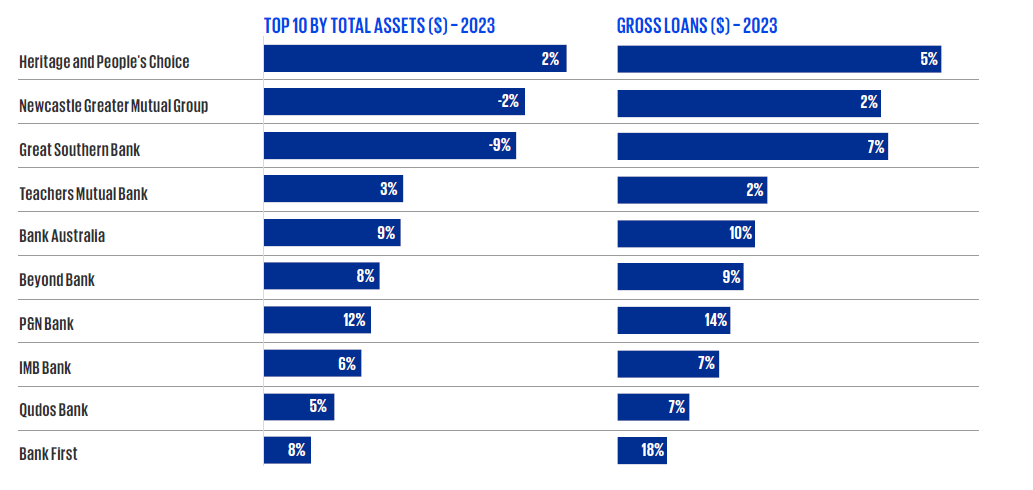

Consolidation remains a major topic in the sector, with two significant mergers completed during the year specifically between Greater Bank and Newcastle Permanent (renamed Newcastle Greater Mutual Group) as well as between Heritage Bank and People’s Choice Credit Union (renamed Heritage and People’s Choice).

The result of the mergers has seen a threefold increase in the number of mutuals with total assets in excess of $20 billion.

Ball said the challenge to the mutuals for a purposeful future was maintaining this year’s results in the face of increasing demands from members as they navigate the impact of sustained high inflation and significant cost-of-living pressures, demands from the regulator, and increasing community expectations on ESG and data protection.

“Mutuals that embrace these challenges and see opportunities through leveraging the strong connection to the community, sense of purpose and ability to embrace the possibilities of generative AI will continue to grow sustainably,” Ball said.

A report from KPMG released earlier this month showed the country’s major banks reported a combined cash profit after tax of $32.5bn, up 12.4% compared to FY22.

According to the KPMG Australian Major Banks Full Year 2023 Results Analysis, the RBA’s tightening of monetary policy was the key driver of NIM, which increased by an average of 9 basis points on FY22 across the major banks.

Were you surprised to see the mutuals perform so well in challenging times? Share your thoughts below: