It is 2% lower than the figures in June

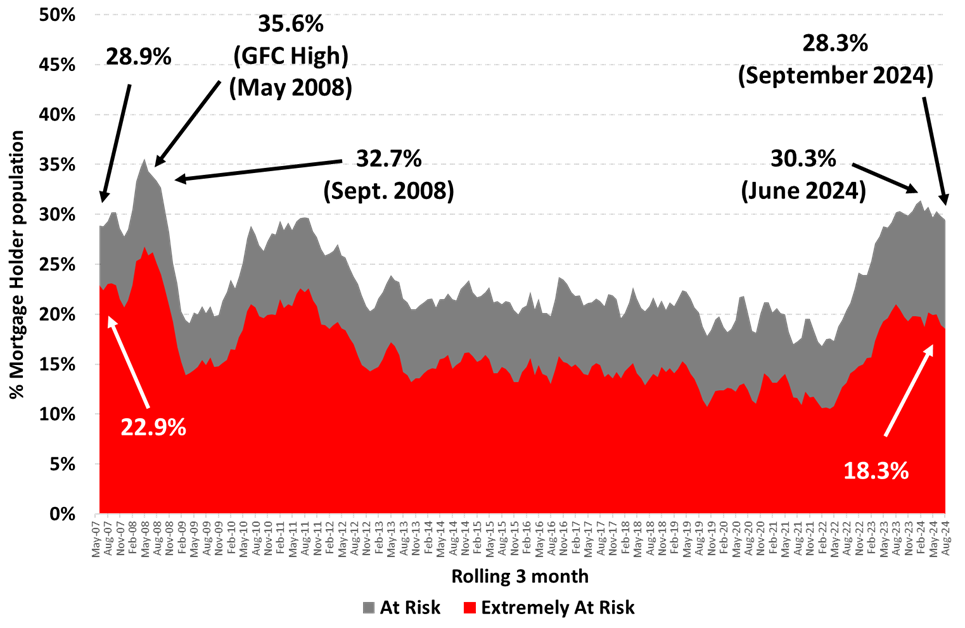

The risk of mortgage stress among mortgage holders has continued its easing streak for the third month in a row, according to research by Roy Morgan.

The study found that only 28.3% of mortgage holders were at risk of mortgage stress, which was 2% lower than the figures recorded in June before the Stage 3 tax cuts which increased the household income of Australians.

The number of Australians that were at risk of experiencing mortgage stress rose by 917,000 since May 2022, which was around the time the Reserve Bank of Australia (RBA) began to increase the interest rate.

“The figures for September 2024 represent an increase of 917,000 considered ‘at risk’ since the RBA began raising interest rates in May 2022. The figures take into account 13 rate increases which raised interest rates by a total of 4.25% points to 4.35%,” said Roy Morgan CEO Michele Levine (pictured).

With the official interest rates now at 4.35%, there was not a total of 1,082,000 Australians that were considered to be extremely at risk. This made up 18.3% of mortgage holders and is higher than the long-term average of 14.6% in the past decade.

The study also found that in the previous month, there were a total of 28.3% of mortgage holders that were considered as at risk of mortgage stress. With the number amounting to 1,724,000 at the time, Roy Morgan believed that it will increase by 27,000 in November if the RBA increased the interest rates by 0.25% to 4.60% during Melbourne Cup Day.

The considerations regarding the risk of mortgage stress in mortgage holders involve either their mortgage repayments being greater than the percentage of their household income, which depends on their income and spendings, or if their interest only revolves a specific proportion of their household income.

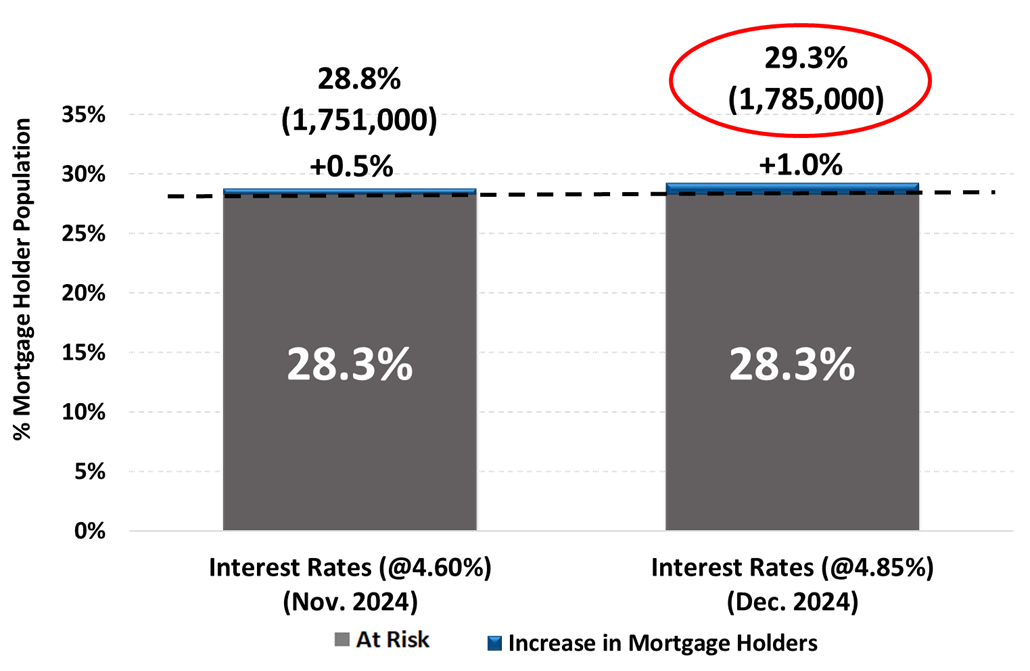

“The crucial September quarter inflation figures are due out next week. These figures are expected to have a significant influence on the Reserve Bank’s decisions relating to interest rates over the remainder of the year and at their meetings in early November and December,” said Levine.