After another year of tightening credit policies and campaigning for the future of mortgage brokers, non-banks have really stepped up their game

After another year of tightening credit policies and campaigning for the future of mortgage brokers, non-banks have really stepped up their game and taken back some of the home loan market share. MPA asked brokers what these lenders have done particularly well and where they still need to improve

As credit policies have shifted, the non-banks have moved in where the larger banks are now unable to service the borrowers they used to. No longer are non-banks the alternative lenders; they are offering the service, turnaround times and products that brokers are choosing to go to first.

According to figures from the MFAA, duiring the period April to September 2018 the share of broker-originated loans grew to 9.6%. This coincided with a drop in the proportion of loans going to the major banks. Looking at the results of MPA’s Brokers on Non-Banks survey, it’s no wonder why. Brokers are reporting that non-banks are offering easier access to credit assessors, faster turnaround times and more suitable products for a wider range of borrowers.

As time moves forward and even more lenders step in where the banks are moving back, we may find that one day this survey will have to expand what the industry terms as ‘non-banks’.

When asked which non-banks brokers would like added to their aggregators’ panels, a few listed fintechs, and as these lenders take on more mainstream clients, perhaps this will happen in the future.

The MPA survey asked brokers to rank each bank from 1 (very poor) to 5 (very good) in 10 different categories of service. The non-bank with the highest average rating won the title of Non-Bank of the Year.

In certain categories we asked brokers to tell us a little more, such as their thoughts on turnaround times, products and support. We also asked them to tell us their favourite non-bank product, and the results are revealed later in this report.

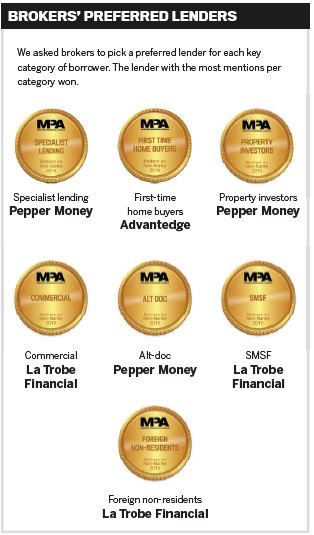

For the third year in a row we included seven additional awards for the preferred lender in different borrowing categories: specialist lending, first home buyers, property investors, commercial, alt-doc, SMSF and foreign non-residents.

This survey is an important resource not just for MPA and its readers to discover how the non-banks are doing, but for the non-banks themselves. Brokers are their main distribution source, and the nonbanks are therefore keen to know how they are performing and how they can continue to improve, particularly as they are growing and expanding in the current environment.

Read on to see the full results and which lender fared best in each category. Thanks to everyone who took the time to take part in the survey; it would not be possible to run these reports without you.

FINAL RESULTS

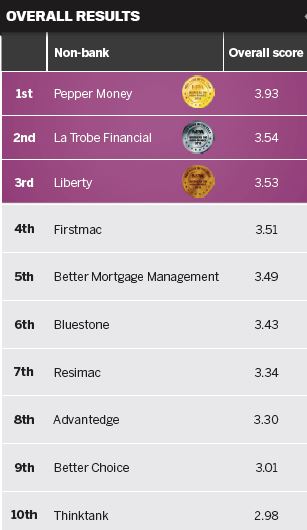

While last year’s winner has retained its top spot, 2019 saw some big changes in the top 10, including last year’s seventh place medallist taking the silver this year

WHY USE A NON-BANK?

The complaint has been the same all year: the banks are pulling back from some borrower segments and making it harder to get deals through.

Since the royal commission in which the banks were called out for bad practices, lending to households has continued to fall. According to the ABS data for June 2019, the value of lending for dwellings, excluding refinancing, dropped by 18% year-on-year in trend terms.

With concerns raised about banks relying too heavily on the Household Expenditure Measure benchmark, the banks are now running a much closer eye over borrowers’ living expenses. In a report by UBS last year, the group said that if banks were to do this it could reduce mortgage borrowing limits by 35%, which is possibly a reason behind the drop in lending values.

Banks were also criticised for their treatment of business borrowers, and brokers have seen a decline in the number of banks offering their business customers finance.

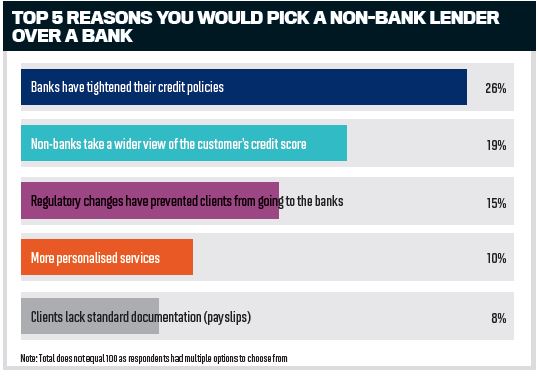

The changes to banks’ credit policies seen in the last year are reflected in this year’s survey, with 26% of brokers saying they have turned to non-bank lenders as a result.

“Non-banks see the deal for what it is rather than what appears on the client’s credit file,” said a broker from Victoria.

“Non-banks see the deal for what it is rather than what appears on the client’s credit file,” said a broker from Victoria.

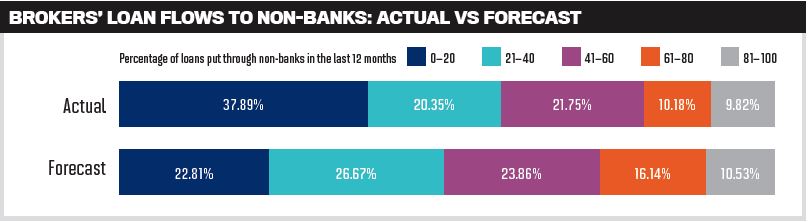

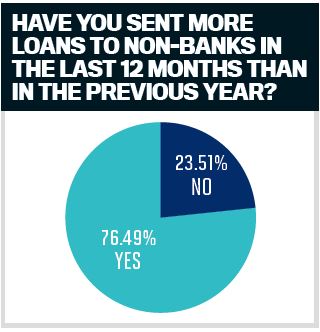

It was therefore no surprise to see that the number of brokers sending more loans to nonbanks in the past year had risen to 76%, up from 69% last year.

The proportion of brokers who put less than 40% of loans through to non-banks dropped by roughly 10% over the last 12 months, as more brokers turned to these lenders. One in five brokers sent more than 60% of loans to nonbanks in the past year.

As one broker from NSW said in this year’s survey, “The banks tightened their appetites this year, forcing more business to the nonbank market. The non-banks have expanded quickly to cope with the new volume.”

It’s good news for the non-banks that brokers also seem to be keen to send more business their way in the year ahead. Around 50% of brokers expect to put more than 40% of loans through to non-banks in the future.

PRODUCT AND PRICING

Brokers’ biggest barrier to sending loans to non-banks is their higher rates and fees, while brand awareness has become less of a concern for customers over the last year

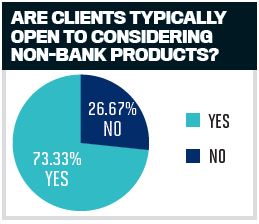

Although brokers have submitted more loans to non-bank lenders over the past 12 months, their customers are not as convinced as they were a year ago. Twentysix per cent of brokers said their clients were typically not open to considering non-bank products, a considerable increase from just 10% last year.

Although brokers have submitted more loans to non-bank lenders over the past 12 months, their customers are not as convinced as they were a year ago. Twentysix per cent of brokers said their clients were typically not open to considering non-bank products, a considerable increase from just 10% last year.

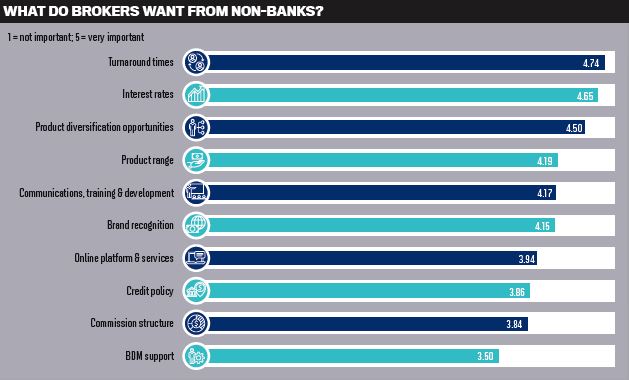

According to the survey, the biggest barrier to putting more business through the non-banks was their higher fees and rates, which 43% of brokers said was a problem.

Research by Canstar shows that the nonbanks’ average variable rate on a $400,000 home loan was 3.37% as of September 2019, whereas the average variable rate on the same loan offered by banks was 4.01%. The average three-year fixed rate on a nonbank loan was 3.39%, compared to the banks’ 3.46%.

While a lack of brand awareness topped the list of barriers to using non-banks last year at 38%, only 25% said it was an issue this year, which demonstrates either a greater public perception of the role played by non-banks, or that the views of the consumer are changing.

Pepper Money won three gold medals for product-related categories and was voted by 27% of brokers as having the best product. Many of the specific products highlighted in the survey fell into the specialist lending category, such as alt-doc loans or near prime products, but with Pepper joining the commercial space earlier this year, the lender was top of mind for many brokers.

One broker from NSW said, “The introduction of Pepper into the commercial space has provided overdue and much-needed competition to the market.”

Pepper Money also took the gold medal for its interest rates, which was an important win considering that higher rates and fees were one of the top barriers for sending loans to non-banks.

Interest rates was also the second-most important feature that brokers considered when choosing a lender, behind turnaround times, for which Pepper Money also claimed the top medal.

Only 5% of brokers said they had problems accessing non-banks because these lenders were not on their aggregators’ panels. Many survey respondents said they were very happy with the number of non-banks they had on their panels.

For those who wanted more choice, Liberty was the most sought-after non-bank.

The proportion of brokers saying that customers wanted a branch network has dropped consistently for the last two years, from 16% in 2017 to 11% in 2018, and now to 10% in 2019.

TECHNOLOGY, TURNAROUND AND SERVICE

With more work required to get deals through, one of brokers’ top priorities this year is faster turnaround times, and non-banks are keeping up with the demand

Brokers ranked turnaround times as their most important criteria this year with a score of 4.74 out of 5, showing just how crucial this factor has become in the past 12 months as home loan applications and processes are taking longer.

With the non-banks receiving more business from brokers – and having to comply with many of the same regulations as the banks – these lenders are at risk of seeing their turnaround times increase. However, brokers this year have actually reported seeing improved turnaround times, and this is painting a much better picture than in both 2017 and 2018.

Thirty-five per cent of brokers this year said turnaround times had improved or improved significantly, compared to just 24% last year. Only 28% of brokers this year said turnaround times were worse, whereas last year the proportion was 40%.

“Non-banks are keen to grow their market share and are investing in the appropriate areas in order to cater for the increase in business,” said one broker from NSW.

Those who did report seeing worse turnaround times said they had experienced this across the board, at banks as well as non-banks, thanks to extra checks and increased workloads.

Pepper Money, which took out the gold medal for turnaround times, was specifically praised by brokers for sticking to great times. Last year the lender did not appear in the top three in this category, but as one broker from South Australia said, “There was a time when Pepper would take ages to answer phones; this has now drastically improved for brokers.”

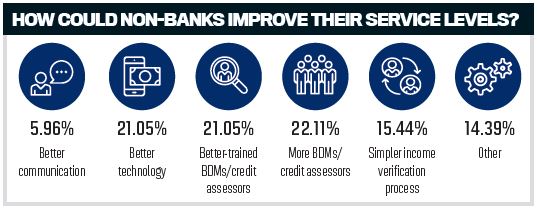

Another broker, from Western Australia, described the challenges experienced by banks and non-banks in greater detail, commenting that it was not just the royal commission that had led to an impact on service levels.

“Many of the [non-banks] seem to have held their nerve particularly well, both in terms of lending appetite and credit policy, and whilst service levels have dropped due to difficulties keeping staffing levels in check, with increased demand and additional compliance, they have helped prop up the banking system as far as possible,” they said.

Commission structures have seen less of a change, with 75% of brokers saying there had been no difference in the last year.

Around 14% of brokers said commission structures were worse, which was the same as last year, but the proportion of respondents who said they had improved was up from 6% to 9%.

WHAT THEY HAD TO SAY

4TH: FIRSTMAC

MPA: Firstmac was particularly praised for its turnaround times. How have you worked to ensure brokers and borrowers are not waiting for decisions?

Kim Cannon, managing director, Firstmac: Firstmac has worked hard to build a culture of personal service that is focused on helping brokers get their deals across the line. We are a friendly, close-knit team where everyone works together, and the answer to any question takes moments, not days. We have no bureaucracy to get lost in.

If brokers choose us they can expect:

- A common-sense approach – At every stage, we work with brokers to make their deals succeed. Our aim is always to come up with a solution for the client.

- Consistency – We are consistent in all aspects of our service, credit and sales so the broker won’t have a deal fail unexpectedly.

- A real alternative – We give brokers an excellent option for customers who are not keen to borrow from a big bank.

We are careful to maintain a balanced number of office-based BDMs and on-the-road BDMs, which improves turnaround times because someone is always accessible to you. We also have a dedicated Sales Support Team. That means a dedicated person is committed to driving deals, from application to settlement.

3RD: LIBERTY

MPA: Liberty jumped from seventh place to third place this year. What has the non-bank been doing to work with brokers?

John Mohnacheff, group sales manager, Liberty: It’s our unrelenting focus on helping brokers and our broker partners build their businesses and help more customers get financial. The one thing we know is brokers value high-touch, personalised support. We have more BDMs than any other non-bank and non-major lender. We work with our brokers from scenario to settlement, and we continually do more sessions to equip and train brokers. Our customers are our brokers and, if you couple this with the relentless pursuit of having satisfied brokers, the situation becomes self-evident. Have we changed anything we have done? The answer is no. We have just increased our connectivity with our brokers. It’s not about the cheapest rate – it’s got to be a competitive rate. What the customer wants is a quick turnaround and to be satisfied in knowing they have a secure lender behind them that ticks all the boxes and provides them their home loan.

2ND: LA TROBE FINANCIAL

MPA: La Trobe Financial has jumped to second place from seventh last year. It was also listed as the preferred lender in three out of seven borrower groups (commercial, SMSF, foreign non-residents). What is behind the improvement?

Cory Bannister, senior vice president, chief of lending officer, La Trobe Financial: We’re delighted and honoured to receive such positive feedback. Recognition such as this is indicative of the great work performed by the whole team at La Trobe Financial, who all play a role in ensuring we provide financial solutions to underserved markets, making a tangible difference to people along the way.

Whilst we can’t be sure of why brokers voted for us, we can say we worked incredibly hard on the following three areas and are hopeful they made an impact:

- Increased broker footprint (+27%). In response to the strong demand from brokers to learn more about niche products, we expanded our Partnerships Team nationally to 30 people, in order to maintain our responsiveness and educational approach for brokers.

- Delivering a broad product suite. We strive to offer the broadest product set, allowing brokers a one-stop experience for mortgage credit, which means that we are relevant to brokers for scenarios on a daily basis.

- Providing stable product, price and policy settings in a complex and confusing market. We are often told by brokers that one of our greatest strengths is our stability. We have maintained product availability, a consistent credit policy and, above all else, a boutique personal service proposition that has been scaled with business growth, in a time when others have scaled back or withdrawn from market segments completely.

1ST: PEPPER'S BACK ON TOP

Going a step ahead of last year, Pepper Money has won eight out of 10 categories. Pepper’s Australia CEO, Mario Rehayem, explains the non-bank’s success

MPA: Why do you think brokers were so pleased with Pepper’s service over the last 12 months?

Mario Rehayem: There isn’t a day that goes by that I don’t receive an email, text or call from satisfied brokers on how grateful they are about our grade of service.

That’s because Pepper has invested a significant amount of time and money over the years to ensure its processes are aligned to broker and borrower expectations. This investment ensures a higher grade of service across the entire origination chain. Brokers are not measuring our service purely on our same-day turnaround times for fully assessed applications; service has a much larger remit than that. Brokers measure you on the entire experience, from the quality of your BDMs to the way you treat customers post-settlement.

MPA: You took out the gold medal for turnaround times, after not receiving a medal at all in this category last year. What have you done to improve in this area?

MR: We focused on refining our underwriting processes to maximise productivity. To do this we engaged with brokers from every state and held multiple focus groups to better understand the areas we needed to improve.

To consistently deliver quick turnaround times, you need to have an efficient decision engine that assists your credit team. With the introduction of Pepper Product Selector and Pepper Resolve we continue to increase the number of customers we have helped, and have done so in a more efficient manner. More specifically, we’ve increased our application-to-settlement conversion ratios by 14%.

We also have a number of technology enhancements coming out towards the end of the year which will significantly improve our turnaround times and overall grade of service to brokers and borrowers.

MPA: What are you going to do over the next year to continue to work with brokers?

MR: Brokers and borrowers are at the heart of everything we do. This is why we will continue to invest heavily in broker education, invest in the Pepper brand to build awareness, and release more products that will cater to a larger cohort of borrowers. But most importantly, we promise to never be complacent. We will continue to challenge the accepted and push every boundary to maximise our overall experience in the most responsible way.