Commercial lenders work closely with brokers to boost support

Adaptability and resilience are important traits in commercial finance for both lenders and their broker partners.

In an uncertain economic environment, the sector has had to roll with the punches when it comes to the higher cost of capital, increasing credit risk and fluctuating property market dynamics. Higher interest rates and inflation, regulatory burdens on development and SMEs, and the rising costs of building and labour are among the ongoing challenges.

But commercial lenders and brokers have been able to adjust to their clients’ changing circumstances and provide the flexibility and support their businesses need to thrive.

The Australian economy remains buoyant overall, with demand for larger developments remaining strong and asset finance performing well – particularly in areas such as agribusiness and green equipment.

More residential brokers are leaning into the diversification opportunities that commercial lending provides, either by upskilling or forming partnerships with commercial brokerages.

To discuss these and other issues, including how technology can boost the sector, MPA recently held its annual Commercial Lenders Roundtable at Nobu in Sydney.

The attendees were Cory Bannister (La Trobe Financial); Karen Carter (BOQ Business); Joel Harrison (Thinktank); George Lyall (Millbrook Group); Michael Moloney (Resimac); Barry Saoud (Pepper Money); Grant Smith (ORDE Financial); Chris Thomas (NAB) and commercial broker Isabella Constantinou (Simplicity Loans & Advisory). Stephen Scahill (LMG) was unable to attend but provided written responses.

Q: How have commercial lenders adapted to challenges such as higher interest rates and inflation, reduced consumer spending, and rising construction and business costs in the last 12 months and reached out to support brokers and their customers?

The challenges a ecting the residential lending space have had a similar impact on commercial borrowing in the last 12 months. Self-employed individuals, SME borrowers and property developers have all felt the pain of rising interest rates and inflation.

Two key trends have emerged: consumers are not spending as much on discretionary items due to a cost of living crisis, and building costs have risen rapidly, exacerbated by a shortage of skilled labour and increased regulation.

Higher construction costs mean borrowers have to pay more, and some developments may not stack up financially for lenders or their clients. Labour availability remains a significant constraint for about 30% of firms, according to the NAB Quarterly SME Survey for Q2 2024, and while SME business confidence has improved slightly, it is still in negative territory.

Bannister (pictured below) kicked off the discussion by saying the high interest rate environment was causing a few challenges, and these were having an impact on commercial borrowers. The first priority was to discuss credit availability, he said: “Making sure that credit remains available. Anyone [lenders] can lend in good conditions; when times are good, it’s really easy to do.”

He said it was important for lenders to play an active and consistent role in the commercial space during uncertain and complex economic periods, particularly with the current steep interest rate curve.

“It’s a mark of maturity, experience and commitment to the channel if you can do that appropriately throughout this period.”

Millbrook Group could structure loans in various ways to ensure clients were in a better position, such as by increasing the contin gency if there were certain cost overruns, Lyall said. “It’s all about really working with brokers and clients for the duration of the build, in order to get the best outcomes.”

Consistency was a key theme for participants at the roundtable.

Harrison said brokers and the commercial lending industry benefited from remaining consistent in their approach. Availability of credit was one thing, but applying a consistent methodology was necessary to give borrowers a clear outcome on “where they are going to get the money from and how”.

“That’s been something as an industry we’ve done a fairly good job on during what continue to be challenging times.”

Saoud (pictured below) highlighted the need to increase and diversify funds for commercial lending, which would give brokers and customers confidence in non-bank lenders.

Non-banks have the ability to adapt credit policy to a changing environment, he said. “It’s looking at our approach to credit, how borrower circumstances, lending criteria and security types [have] evolved, and then ensuring we have the availability of funding to service those customer needs.”

From a broker’s perspective, Constantinou said that when the market provided so much uncertainty for borrowers, it was important that brokers could have confidence in loan outcomes from lenders. Their relationship with the lender and consistency of the outcome were more important than ever in changing times.

“If we’re suggesting a non-bank in the private space, we need to have confidence that we’re not putting the client in something that’s not going to provide the best outcome for them,” said Constantinou. “Knowing that we have that confidence in the lenders that we’re dealing with is so important.”

BOQ Business has looked at the challenges facing brokers and customers across the whole SME market, Carter (pictured below) said. The lender has implemented a number of policy changes, making it easier for clients to access funds.

“We’ve reduced interest cover, we’ve increased the amount that we’ll lend to with higher LVRs, and we’ve reduced the amount of information that we require,” said Carter.

“We could also see that some existing customers were having trouble meeting covenants, so we’ve made adjustments to our policy to better accommodate and respond to this”.

However, Thomas said the economy is robust, and NAB has been focusing on the value of its partnerships between business bankers and brokers.

“Given that it’s a multi-speed economy, a lot of the effort in helping customers get the funding that they need is really based around the forward projections,” he said.

More now than ever, deeper financial analysis was needed due to higher interest rates, inflation and labour pressures. Without this, it could be more difficult to obtain credit approvals.

Thomas said the need to stress-test a customer’s forecasts and tie it all back to the customer’s strategy was a joint responsibility “between the broker and the banker to work together to solve clients’ needs”.

At NAB, credit policies are not being changed, but the focus is on understanding both broker-introduced and direct customers, and what was happening in the economy. “So that we give the right advice to that client and lend them the money that they need, through the extension of appetite around existing policies,” said Thomas.

The major bank has also been running credit workshops for its experienced bankers, focusing on understanding key cash drivers, balance sheets, profit and loss and projections.

Thomas (pictured below) said that while bankers were already doing these things, it was critically important to keep “sharpening the axe” on education, and these workshops were also being rolled out to NAB’s key commercial brokers.

“That’s a really important feature of the market – that the credit continues to flow despite all the pressures out there,” Thomas said.

Scahill (pictured below) said it was only fair to point out that it was brokers who had done the heavy lifting with their customers.

“There has, unquestionably, been anxiety amongst commercial customers as they have dealt with interest rate rises, inflation, higher construction costs and more,” he said. “Some industries are still dealing with the hangover from COVID and the restrictions that were in place.”

As an aggregator, LMG has sought to provide its brokers with the tools and support they need.

“Broadening the scope of our lending panel has also been important,” Scahill said. “In the current environment, our brokers and their customers need an array of solutions, and whilst many exist in the market, we see it as our responsibility to vet the many lenders out there and partner with those we believe offer the best solutions.”

An economy operating at two different speeds – that is how Smith described the current market.

“For every Porter Davis [home builder that went bust] that didn’t battle through, there’s another 10 builders that actually got through that changing condition, are thriving, and are looking at government housing demand as a real opportunity,” he said.

Smith said it was imperative for lenders to look at the individual positions of borrowers and not get caught up in industry trends. The aim was to help borrowers and understand what they want to achieve.

“For someone starting to feel financial pressure, could a viable solution be found through a debt restructure, partnering with a good broker who could help them explore all the actual options?”

Resimac’s asset finance division does include some short-term property lending, Moloney (pictured below) said.

He praised banks for the strong funding made available to non-banks during a tough period.

Resimac is maintaining its LVR discipline on short-term property loans. “We need to be offering loans, but we just need to maintain a balanced portfolio.”

In asset finance, the non-bank’s average loan is $80,000, and SMEs are able to pay a fixed rate car loan for this amount without problems.

Moloney said that while asset finance is focused on low-doc lending, there are other options. “If you’re prepared to provide a few BAS statements or ATO portals, you can get more money through ‘lite-doc’ and full-doc lending.”

Q: Where do you stand on the issue of broker specialisation in commercial finance versus the need for residential brokers to diversify, and why? How do you educate both commercial finance brokers and resi brokers who want to move into this space?

With 74.1% of all new home loans written by mortgage brokers, it’s clear that competition for market share is fierce.

Lending activity has dipped in the residential sector given rising interest rates, reduced borrowing capacity and serviceability constraints. That is why so many brokers are looking to diversify their client offerings into commercial lending, where it’s estimated only around 30% of loans involve brokers.

But moving into commercial finance involves brokers upskilling and gaining an understanding of a sector that’s quite different to home loans. Some brokers prefer to pass on any leads to experienced commercial brokers for a fee.

Constantinou (pictured below), who was named MPA Top Commercial Broker in 2022, said she believed there would be a change in the trend to push residential brokers to diversify into commercial.

Simplicity Loans & Advisory only writes commercial loans and chooses not to do residential loans. “We’re really good at commercial finance, and it makes sense to stick with what we know,” Constantinou said.

The brokerage enjoys great relationships with banks and different lenders. “We lean on our resi partners for all our resi needs because they’ve got all those relationships.”

Constantinou believes the trend of individual residential brokerages diversifying into commercial will change, with partnerships between major residential and commercial brokerage firms becoming more common.

“The resi side is very convoluted – there’s a lot of hoops you have to jump through,” she said. “I don’t understand how you can be really good at it if you’re not wholly focused on it. The resi brokers that do that really well should be leaning on their commercial partners, more so than looking to diversify and doit themselves.”

Thomas was supportive of Constantinou’s views. Looking at what was right for the customer, he said that NAB, other lenders and brokers had an obligation to work together “to get the right people in front of the customer the first time”.

“I like to see commercial brokers that have got the commercial acumen and experience to actually cope with their customers’ changing needs,” Thomas said.

However, Thomas said it was encouraging to see brokers investing in a commercial partnership or bringing someone with those skills into their business.

“We want customers to have the best experience possible, so it’s important that brokers have the right support, whether that is a commercial partner, or the knowledge and skills.”

Constantinou added that she wasn’t discouraging either residential or commercial brokers from being educated about each other’s sectors.

She said it was important for residential brokers to know the fundamentals of the commercial space because it would help them identify further opportunities with their residential clients and strengthen the industry.

“I just think there’s an opportunity for more partnerships than diversification.”

Carter also expressed caution about residential brokers stepping up into commercial finance. They needed to make sure they were providing the customer with the right experience.

She said more and more business bankers are moving into commercial broking, which is increasing the size of the sector.

“We’re definitely targeting the business brokers that have become commercial brokers; they do know what they’re doing,” said Carter. “Our education to them is more about what the product is and how we can structure a deal.

“That said, we’re about educating residential brokers if they have a keen interest.”

Education sessions o ered to date included topics such as how to build cash flow and present the right loan that matches the client’s needs. “We provide cheat sheets; we’ve got a commercial broker with niche lending guidelines.”

BOQ is expanding its remit in commercial broking, allowing brokers to access insurance premium funding and asset finance through its other divisions.

Carter said a number of aggregators have commercial mentoring programs in place that are very helpful.

Smith (pictured below) agreed with Constantinou that the trend is towards commercial partnership models – diversifying through others rather than brokers doing it on their own.

But he said ORDE Financial had always believed it was the broker’s choice, and if brokers wanted to move into commercial lending, ORDE would give them the education and support they needed to successfully provide that service to their customer.

Smith said it went beyond webinars, workshops and presentations. “It’s been the establishment of our relationship management team, who are focused on supporting brokers with upskilling and diversifying their business.”

The team sit within ORDE’s distribution team, working alongside a broker’s dedicated BDM. They draw upon their deep credit experience to support brokers from initial scenario engagement all the way through to submitting the loan.

Harrison (pictured below) said some businesses are feeling the pinch, and so are some brokers, which is why they want to diversify their income streams. He said there are lots of opportunities for residential brokers to step into the commercial space. Some of the more simplified products are “a really good stepping stone for these brokers to build their skills and knowledge”.

“I agree that once it gets into the more complex scenarios, you want to make sure that they’ve got the right people to provide guidance as needed,” said Harrison.

That’s why Thinktank has dedicated relationship managers to provide brokers with support through the process. “If the broker would like us to work with the customer, we can. We’re happy to help in any way that the broker feels comfortable and adds value.”

On the flip side, some commercial brokers are looking to step into the residential space to diversify their income.

“I’m sure most brokers would choose to write multiple deals with the same customer as much as possible rather than spending a multiple of that time and effort looking for new clients,” Harrison said.

“Whether it’s equipment finance, a home loan or commercial property, as a broker I wouldn’t want to step away from that opportunity and potentially leave it open for someone else.”

He said it was up to lenders to provide the support brokers needed through education sessions, the right tools, and insights showing how lenders looked at a deal and why.

Harrison said some brokers choose to work with an experienced commercial brokerage, while others prefer to participate in training courses.

“There seems to be a lot more peer-to-peer mentoring in the commercial space,” he added. “There are quite a few brokers willing to help other brokers along their diversification journey, which highlights how collaborative the sector is.”

He suggested there may be opportunities for a solo broker operation looking to partner up either via mentoring or by potentially merging with a business to include a range of sector experts.

Moloney said diversification depended on the individual broker, their strategy and the market.

“Twelve months ago, the asset finance world was hot, and the resi mortgage business was pretty tough. As a broker, it would be nice to pick the best of both worlds.”

For residential brokers the easier transi- tion was to asset finance, because “you can do quick car loans on loc-doc matrixes; you don’t need to be looking at financial state- ments”, he said.

Overall, Moloney favoured the referral option for brokers.

Thomas said it was exciting to see these partnerships gain pace, whether they were brokers coming together, sharing equity and setting up joint ventures, or formalised referral relationships.

“If you’ve got that diversity within your skill set, there is no client that you cannot assist, and there’s no cycle that you will potentially miss.” This would also lead to great customer outcomes and help brokers manage rising costs.

Bannister said consolidation would be a strong theme going forward. He encouraged diversification but believed it was not for everyone.

“Diversification for diversification’s sake is risky and probably not good for the industry overall. If you take measured steps, commercial-resi is no longer as binary as it once was. There’s so many segments and nuances to each of those markets … a resi broker can perhaps write an asset finance transaction but maybe can’t do a business banking transaction or development finance transaction. It’s no longer black or white.”

Aggregators could play a significant role here, Bannister said, especially in coaching and selecting brokers who were ready to diversify. Aggregators had good education and referral programs, but these could be enhanced to target brokers and “take them on a more selective journey”.

Commercial brokers’ market share remains low and is growing only slowly, Bannister said. “How do we address that? … Rather than having a pathway from resi to commercial, perhaps it’s more a targeted banker-to-broker program. It’s not going to please the banks, but as a whole, more capable commercial brokers is a good thing.”

Saoud said there was a place in the industry for both specialisation and diversification.

“There’s not a ‘one size fits all’, but it comes down to, as an industry, how do we better support the right brokers to diversify? I think the industry’s done a good job, but we need to continually listen to brokers, meet them where they’re at and develop the right content to support their diversification pathway.”

Aggregators and the MFAA and FBAA all had a part to play, as did lenders, in creating adaptable ways to better educate and support brokers, Saoud said.

Brokers needed to have a long-term diversification strategy to ensure they provided their customers with the best outcomes. They could achieve this by either investing in education or establishing the right referral partnerships.

Scahill said LMG had a vision of all brokers offering commercial finance solutions to their clients, either directly or through experienced commercial brokerages in the network, while maintaining the client relationship.

“The relationships that brokers have developed with their clients are powerful. Customers trust their brokers to provide them with the best service and outcomes, and that extends beyond home loans.”

LMG’s role as an aggregator is to provide clear pathways for those brokers who want to diversify. Scahill said tech had been at the cornerstone of this, with MyCRM enabling brokers to service clients across any loan vertical, whether commercial, residential or asset finance.

“Having state commercial specialists available to all brokers has provided many with the confidence to begin their commercial journey, knowing they have an expert available to them should they require support.”

Q: Broker question from Isabella Constantinou: How are the lenders who play in the construction space finding the changing landscape? Particularly given the banks are coming back into the market with some pretty competitive terms on construction debt. Is there going to be any change to their policies around land/pre-development loans/ transactions with a development feel (not necessarily construction loans)?

Bannister said La Trobe Financial is starting to see the banks offering construction finance for good, solid transactions, and this is also welcomed and encouraged.

“For the economy broadly, we need more and more people fuelling that particular space. The tradies need it – there’s a lot of people that are relying on construction getting off the ground.

“Once we get momentum going again, and more construction activity picks up, everyone in this room will prosper because there’ll be more self-employed clients available looking for finance, there’ll be more construction coming out of the ground.

“The approvals are there; the starts are low. If the starts pick up, there’s still more than enough business to go around.”

He said La Trobe Financial would continue to exercise discipline: “knowing what your appetite is and sticking to that … which has served us through multiple cycles”.

That provided consistency, which was good for brokers, while other operators could also fill gaps.

Lyall (pictured below) agreed that banks had become more competitive in the construction space. Millbrook Group has adjusted its policy and funding structure to be more flexible and quicker to market on certain transactions. “So, if we have a developer who’s looking at starting a project, maybe a six-month lead time for a bank in order to get all the CPs [construction permits] met, we could turn that around in two to three weeks subject to all the valuations and QS [quantity surveys],” Lyall said.

Millbrook hasn’t changed its leverages or rates but is acting faster and offering flexibility on certain covenants and loan conditions.

Constantinou asked Thomas about his views on the changing development appetite, particularly in light of Westpac introducing a competitive no-presale construction policy for townhouses.

Thomas said for larger development transactions NAB is seeing good flows come through as well as a strong pipeline, although customers are taking longer to make decisions. “We have a real sweet spot in that sub-$5 million development space, and that’s probably the laggard.”

Customers that traditionally develop in that space are holding land but are tentative about going ahead with the development because they are worried about the costs and controlling the inputs.

“We see the greatest risk right now in terms of that effort to build more being really our customers’ appetite to push forward,” Thomas said. “A lot of that’s got to do with where interest rates are and also now that we’re looking at potentially higher rates.”

NAB still has presale requirements, but Thomas said the bank does have an appetite to “do something a bit different, where it makes sense to do so”.

Q: Broker question from Isabella Constantinou: For the lenders for which construction is not your core business, are you planning to get into that space, lending to developers?

Saoud said Pepper Money is keen to fund construction loans, seeing the significant growth in appetite for construction development and vacant land acquisition.

“We’ve adjusted our credit policies and processes to accommodate those changing borrower circumstances who are seeking construction loans.”

Traditionally, Thinktank is not viewed as a lender that brokers will seek out for construction funding, but Harrison said it sees this as an area where more funding support is needed.

“Recently we released two new short-term products, which are designed specifically for construction and developer borrowers.”

Harrison said these include three-year terms, flexible income-verification options and a residual-stock policy.

“We know that customers are still buying assets that are either new or still under construction, and we want to be able to help with that.”

Smith said ORDE Financial has always taken a tailored approach to individual borrowers, taking a borrower’s position and requirements into account when making credit decisions. “The result of that is we’ve always been comfortable assessing complex profiles like builder/developer.”

He said ORDE has also always aimed to help brokers offer more to customers. That’s why it launched to market with a full product suite and continues to introduce new products such as Prestige loans for high-end residential properties.

In August, ORDE introduced its Residential Construction loans in response to broker demand for a construction product that’s flexible, transparent, easy to manage, and delivered quickly by an experienced credit team. The product offers borrowing solutions up to $2 million, catering for borrowers with alternative income documentation and less than perfect credit history.

Q: What’s been happening in asset finance, and why is this such an important segment for brokers and SME clients?

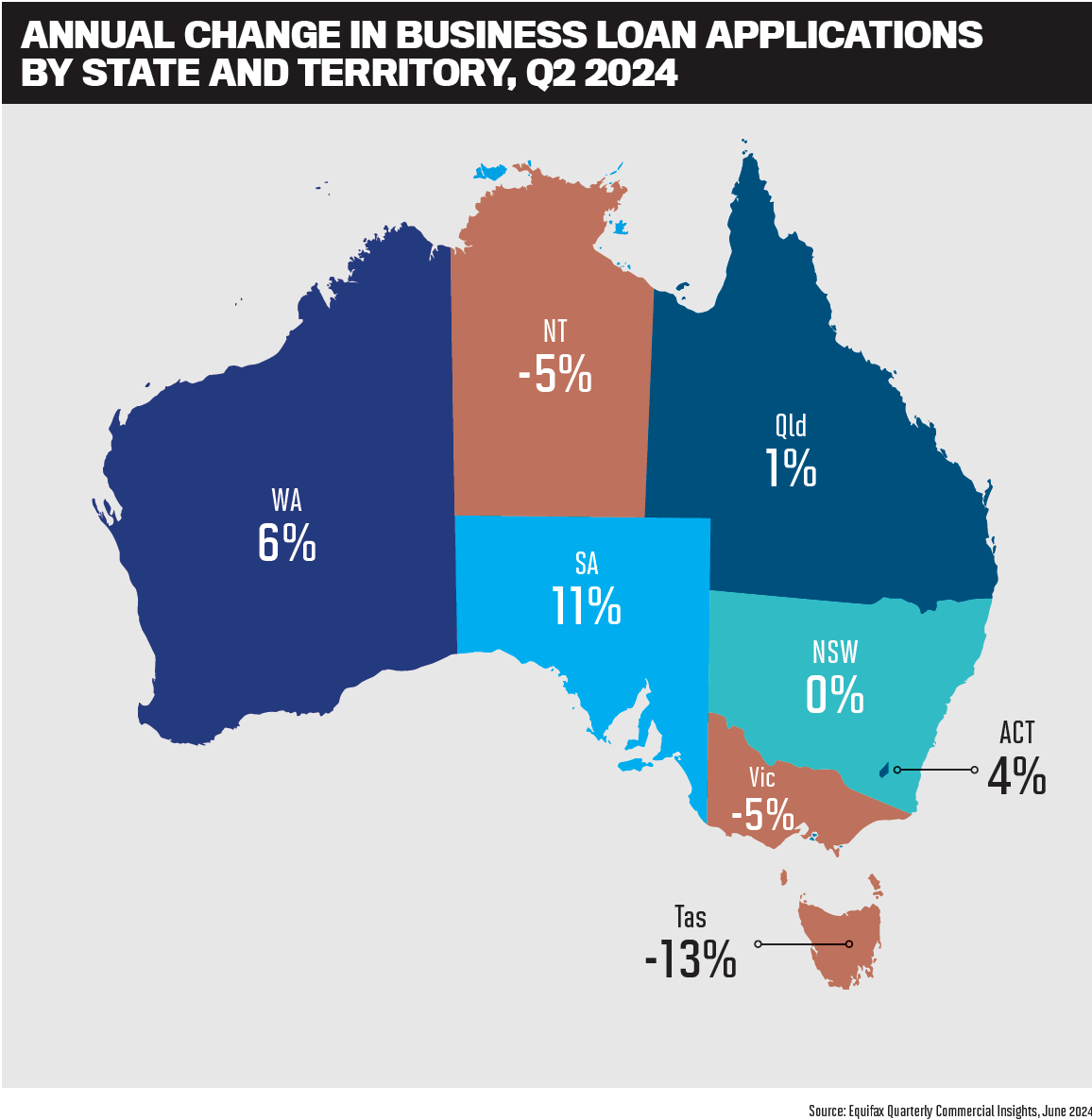

Asset finance applications fell by 8.1% in the June 2024 quarter, according to Equifax’s Quarterly Commercial Insights report, which went against the grain in terms of the usual expected lift in Q2 applications due to businesses purchasing new equipment at the end of the financial year.

Equifax speculated that SMEs were avoiding large credit contracts because of cash flow concerns and tighter margins.

But while there has been some pain, the roundtable participants said asset finance is resilient, and the future looks bright.

Moloney said Resimac had only been in asset finance for three years and is still in a growth phase, with its loan book doubling this year. However, the past six months have proved challenging for the asset finance sector due to the broader economic conditions.

“I would suspect if you ask most brokers or lenders, they’re probably down slightly over the past six months,” Moloney said. Some of that was due to the instant tax write-off, which had dropped from $150,000 last year to $20,000 this year.

“I’m a glass-half-full guy – there’s plenty of infrastructure money to be spent out there, whether it’s in Brisbane for the 2032 Olympics or the Coffs Harbour bypass.

“We lend to SMEs to help the brokers. I don’t see that stopping; it’s a big part of the market.”

Moloney predicted the year would prove to be a good one for asset finance.

“With brokers, it’s about making sure you’re listening to them, what they need, what prod- ucts, what’s working for them, where’s the sweet spots in the industry.”

More residential brokers are writing asset finance, and Resimac is making it easier for residential brokers to offer asset finance to their clients, he said.

“If you’ve got a borrower that’s got a home loan, they’re highly likely to need a car loan at the same time … you want to be able to help the broker sell our product,” Moloney said.

Scahill said the asset finance sector had proven to be resilient during economic uncertainty, with federal government initiatives – such as the instant asset write-off – supporting this.

“We anticipate the strength in this sector to continue ... asset finance provides an avenue for brokers to support clients above and beyond the commercial landscape, strengthening relationships and increasing revenue streams.”

Scahill said for many types of businesses, the link between commercial and asset finance lending is strong.“A broker with the ability to operate across both sectors broadens the range of solutions they can offer their clients.”

Pepper Money has experienced continuous record asset finance originations, focusing on balancing volume, risk and margins, said Saoud. “It’s a key product which is going to be maintained in our stable and where we have seen great success.”

Saoud said asset finance is a key area into which brokers could diversify. “It’s simple, it’s fast, and integrating it through technology serves a really good purpose, deepening and strengthening relationships with our partners and their customers.”

BOQ is still seeing demand in the agriculture and health sectors and plays a key role in these niche markets, Carter said. “We are using it as a tool to help SMEs grow and help with their cash flow.”

NAB is experiencing strong demand from commercial asset finance customers looking to automate due to labour shortages, Thomas said. Clients also want green equipment because of the lower carbon footprint.

“We’re really excited about equipment finance; it’s probably a barometer of the business community and their desire to want to continue to grow in the right sectors.”

Strong sectors include agribusiness, mining and food manufacturing.

Thomas said NAB is keen on working with brokers to ensure that their customers are using the right products to finance the right assets.

“Often we find situations where customers are using their balance sheet or perhaps even property to fund equipment.”

Q: How can technology revolutionise commercial lending, and what plans do you have to improve tech, particularly when it comes to automation and AI?

It’s widely accepted in the industry that residential lending has got the jump on the commercial finance sector when it comes to the adoption of technology and its wider use by both lenders and brokers. But this appears to be changing.

The roundtable participants discussed their companies’ investments in automation and other tech tools, and how AI could assist the sector.

Technology and artificial intelligence are tools that can enhance the broker experience by making businesses more efficient, said Lyall.

“However, we still think that there needs to be that human touch, especially in the commercial space. There need to be BDMs that are on the phone talking through scenarios with their brokers. From Millbrook Group’s point of view, we don’t see that ever changing.”

Smith said the commercial finance industry is lagging behind when it comes to technology, but it’s “a complex beast” to tackle.

Certain segments, such as asset finance, adopted automation years ago, and there has been greater use of technology in property lending.

He said ORDE Financial had invested in aligning its automation with both residen- tial and commercial and residential credit functions. “This means that our commercial process becomes as easy as our resi process for brokers.”

Automation gains could be seen in direct modular platforms, credit steps to speed up the loan process, and broker customer experience elements such as digital signatures.

ORDE Financial is watching AI developments with interest, Smith said.

His own view was that while early AI adopters would make gains in pricing models and understanding risk, there would be opportunities for customer-focused non-banks like ORDE due to mispricing and specific lending segments being excluded.

Constantinou said technology would not replace “commercial thinking”. By this she meant “the ability to look at a transaction and make a decision, not just on the prop- erty, the LVR, the location, but actually being able to look at the specifics and make a commercial decision”.

Simplicity Loans & Advisory was one of the early adopters of automating processes and using tech to help identify lenders that “might do transactions pretty easily”.

The brokerage is developing systems where you can plug in basic details such as property, location and asset class, Constantinou said. “It will then tell us the lenders that will do that transaction, what LVR they’ll do it at and who to contact.”

She said brokers wanted technology that would boost efficiency and by extension help them build relationships with certain lenders who played in that space.

While technology wouldn’t replace commercial thinking, especially in non- bank private lending, Constantinou said it could work better for banks, which had a more “formulaic” credit appetite.

Carter asked Constantinou about the accuracy of the tech tool Simplicity was using and whether it suggested the right lenders.

“It’s a work in progress, but it’s pretty good,” Constantinou replied.

She said the brokerage is in the process of collating all the data and building the system.

“However, it still requires the broker using it to have some knowledge of why it won’t be the best option to go to a lender that it suggests. It still requires a human brain to ultimately make the decisions.”

Carter said she loved AI, describing it as a great tool that she used a lot. “I have found within the bank [that] using it is actually helpful, and it creates a lot more efficiencies.”

She encourages her BDMs to use AI to help structure emails. “But you do need that human element; you need to review what it comes out with because if you just hit send you could be quite embarrassed about the wording or incorrect inferences,” she said.

“I don’t think it will replace bankers; we need that commercial view and to be able to structure deals differently, which AI won’t be able to do.”

Thomas said he was excited about whattechnology could bring to the commercial broker segment, but there was a long way to go to change practices.

“We still see so many transactions that are submitted by email, in very different forms. There’s a lack of standardisation across different aggregators, brokers and banks, so you can only deduct there’s huge inefficiency in our system.”

The benefits of technology are enormous, he said. It saves time spent on keying in basic information, so brokers can spend more time face-to-face with their clients.

Thomas said it was not even about AI but about standardising a credit submission so that when brokers sent it to banks it would fit right into their systems, reducing joint work efforts.

“NAB is investing millions in our back-end systems to be able to receive information from external sources. And equally, many aggregators and brokerages are investing money into those systems in their own offices.”

He said AI has the potential to look after everything from menial analysis tasks, all the way through to fraud detection. Fraud is an emerging risk, and any tools that could protect businesses would prove important.

Scahill said LMG is excited about the anticipated broker growth in commercial lending and is committed to driving greater efficiencies in its broker businesses.

“We have recently launched a commercial lending platform which is in pilot with a hundred of our leading commercial brokers. This tool is designed to take time out of the deal whilst allowing for the flexibility needed around such a wide array of commercial transactions.”

LMG knows that when it comes to technology the relationship between a commer- cial customer and their broker remains important.

AI has many advantages, Scahill said. “We see value in providing brokers the ability to find and use key information within the CRM in a matter of seconds, powered by AI, as an example of that.”

Anything administrative could “absolutely be automated or digitised”, said Bannister.

“But for assessment, we’ll continue to prioritise human intelligence over artificial intelligence. I can’t see that changing any time soon.”

Harrison said one point that had not been raised was the integrity and safety of the data being transferred when applying for commercial finance. There was still a huge amount of data being submitted by a broker to a lender via email, raising cybersecurity issues, and in this respect commercial lending was lagging behind its residential counterparts.

“What can we actually do to take that risk off the table? Because if brokers are sending a submission through to any lender via email, the client’s financial history and frequently PII is often contained in the application, including aspects of their personal details and data,” said Harrison.

“And if a bad actor intercepts that email, what’s the potential consequence for the lender, the broker and the borrower?”

On that note, Harrison said Thinktank is working on a plan to securely digitalise loan submissions – particularly the data – that’s due to go live later this year.

However, he added: “You’re never going to take the people out of the equation. You always need a human to actually look at the deal on its own merit and be available to work with the broker all the way through the process.”

Constantinou said Simplicity Loans is building a system that will enable brokers to lodge deals to the lenders online through the platform, without requiring email communication.

Saoud said whether it’s technology or AI, Pepper Money’s goal is to support credit confidence and consistency, as well as improve broker efficiency and experience. “This is the optimal goal across the business.”

Asked if brokers liked sending deals straight through to the lender, Constantinou said they did if the system was set up well.

“Where there’s a gap, from a broker’s perspective, is every lender has a checklist for each transaction, but it’s a checklist that applies to every single deal that they will write … I don’t see how it’s so difficult to have a checklist that’s specific to the property, LVR, asset class and the product that you’re submitting the deal through.”

If the checklist was tailored, Constantinou said others could lodge the deal on her behalf without her having to wade through the entire checklist.

Carter noted that banks had to abide by regulatory requirements.

Saoud said the concern for commercial lenders is that, unlike in the residential space, which has two primary intermediary technology platforms in NextGen and Simpology, there are multiple players in commercial finance.

“We know that having the right technology can help automate processes. We have increased our asset finance novated leasing automated approval rate to 78% and digit- ised and automated more than 80% of our home loan underwriting process.

“So, unless as an industry we can agree what that primary platform is going to be, we’re going to continue to struggle to innovate in the commercial lending space.”

Moloney said the industry needed systems that work for brokers. “That’s what we’re trying to achieve, and we’re not there yet, but that’s our ultimate goal. I think that will drive mindset change.”

“Build it and they will come,” said Thomas. “It’s got to be a benefit at the end of the day for a customer.

“We get approached quite often by people saying you could build a system at lodgement, and it’ll give the broker a really great experience, but I’m really conscious that if we can’t then turn that into something faster in the back end, then what’s the point?

“It’s just misleading people. It’s not really an integrated digital experience. We’ve got to be genuine in that we are trying to speed up that process for our customers.”

Thomas said achieving great systems was possible, but it would require the industry to work together.

“We just have to stay the course.”

As a broker, where are you seeing the opportunities in commercial lending? Share your comments below.