Lenders can help brokers, SMEs find best asset and equipment finance solutions

Demand from Australian business owners for asset and equipment finance has fallen in recent times. Hit by constant interest rate rises and high inflation, businesses are feeling the strain of higher costs, as well as supply chain problems and labour shortages.

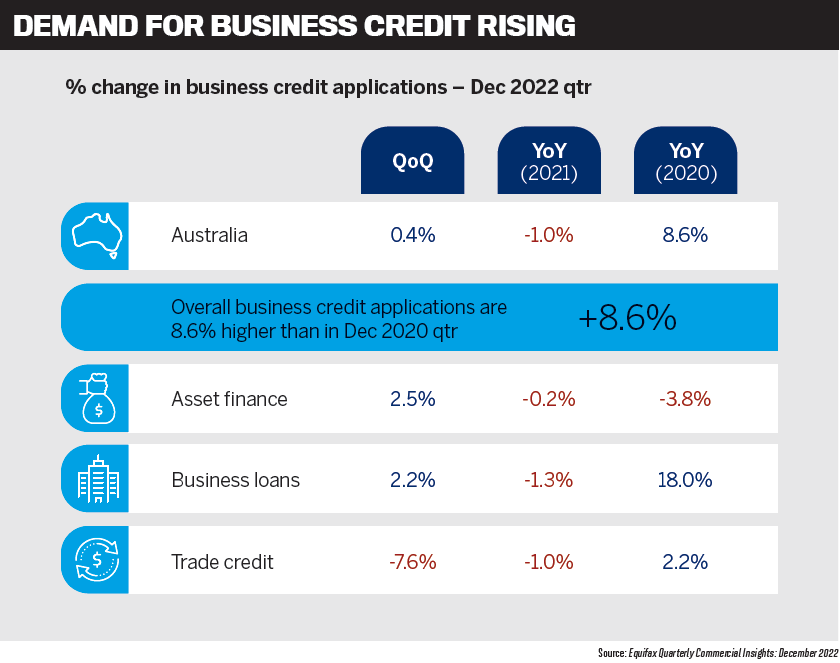

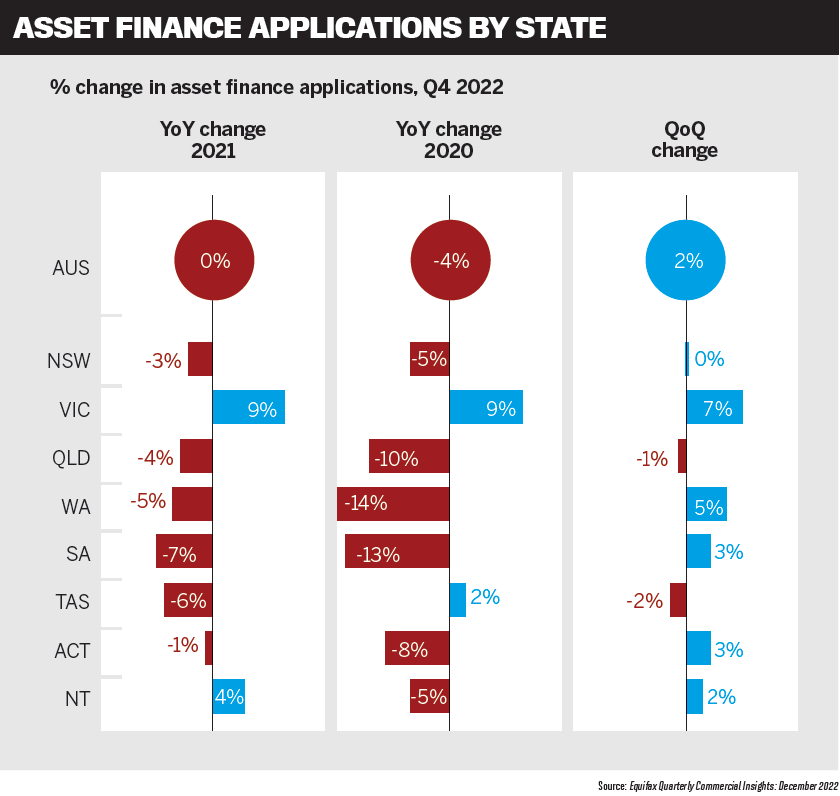

The latest Equifax Quarterly Commercial Insights report shows that asset finance applications were flat in the December 2022 quarter, falling by 0.2% compared to the December 2021 quarter and down 3.8% on the Q4 2020.

But there are signs that conditions are improving: NAB’s Quarterly Business Survey for Q1 2023 reveals that business conditions remained resilient throughout the quarter. Supply chain problems eased, and capacity utilisation rose to 85.5% during the quarter.

To discover more about the asset and equipment finance sector and the opportunities it presents for brokers, MPA sought the views of Mathew Clowes, head of credit and settlements at Resimac Asset Finance; Michael McEvoy, head of sales, asset finance at Pepper Money; and Tracey Crevatin, national partnership manager at Specialist Finance Group.

Market challenges

Clowes (pictured below) says there’s no question that SMEs are feeling the financial pinch.

“Interest rates, inflation and general increases to the cost of living and running a business are all factors impacting volume growth for asset finance,” he says. “But we also know that this sector is resilient. Market shifts always happen in cycles.”

Clowes points out that the pendulum is already starting to swing the other way, with supply chains slowly being restored and inflation lowering month-on-month since the December peak.

“Delinquency remains low, and SMEs are increasingly turning to brokers to assist them with tailored solutions to purchase equipment,” he says.

Certain sectors remain buoyant, with agriculture enjoying an uptick and the transport industry staying strong.

“Resimac Asset Finance continues to experience meaningful growth, and we expect a spike leading up to the end of financial year from SMEs who want to take advantage of the instant asset tax write-off,” Clowes says.

McEvoy (pictured below) says increasing interest rates and inflation are the two biggest contributors to the decline in asset finance demand. Rising interest rates push up the cost of borrowing, and rising inflation increases the cost of doing business.

“Businesses are also reporting that the rising energy prices and staff wage pressures have created additional inflationary challenges,” he says. “Market uncertainty and supply chain disruption to certain vehicles and other business assets is creating further reluctancy for businesses to make new asset investments.”

But overall business confidence among medium and large businesses remains strong, McEvoy says. “A high proportion of civil construction and engineering businesses have experienced continual growth, with many retail segments reporting a strong close to 2022.”

He says education, training and agricultural segments are also gearing up for a strong performance as borders reopen, students return and commodity production recovers from previous drought years.

Crevatin (pictured below) says there’s been a tightening of belts across the markets as interest rate increases bite. Generally, equipment finance is more expensive for consumers, usually being repaid over shorter periods. This is also being compounded by the higher cost of goods due to shortages, supply costs and more.

“The first quarter of 2023 sees enthusiastic brokers thinking outside the square and adjusting their business models to counter waning volumes by branching into the equipment finance and commercial space,” Crevatin says.

Brokers who invest time and money into proper diversification of their businesses gain a big opportunity to grow their share of the equipment finance market.

“Learning to identify the opportunities within your business is an important first step prior to committing to partnerships or employing specialists in this field and is the best step towards diversification,” Crevatin says.

Growth opportunities for brokers McEvoy says effective cash flow management becomes crucial for businesses in challenging times.

“The ability to turn a profit rather than growth for growth’s sake could be the focus,” he says. “Often, asset finance helps businesses manage their cash flow and free up capital for other business needs.”

A broker or finance introducer can help their client navigate the myriad of options in the market, especially as non-banks provide competitive options to business customers.

“With the cost of living impacting household budgets, new vehicles have never been more expensive or hard to obtain, so in this environment we expect to see continued strong demand for used vehicles,” McEvoy says.

Crevatin says, “Asset finance is an exciting space to be in, and there are plenty of opportunities out there; you just need to know where to find them. New cars; transport, plant and equipment; and earth-moving equipment are still experiencing supply chain issues, particularly from overseas.”

As a result, second-hand stock enjoys higher-than-normal values, and this will continue for some time, resulting in a greater need for equipment finance specialists to navigate a more complex second-hand finance market on behalf of their clients.

Crevatin says clients are the most valuable assets in a broker’s business. Brokers affected by volume shortages should be looking to their book for either previously missed opportunities or new ones as their clients’ needs change. “Growth follows activity, and I think as the interest rate movements settle and higher costs of goods and transport subside, increased activity and growth will result from an increase in consumer confidence and larger broker market share in this space,” she says.

Clowes says it’s a great time for brokers to be in the asset finance space, and brokers have access to several competitive products they should bring to their clients. “At Resimac Asset Finance, we have a variety of products aimed at SMEs, including low-documentation loans up to $250,000 and light documenta- tion loans where clients may not have full financials available yet.”

With the end of the financial year approaching, Clowes says brokers should consider how they can assist their SME clients with asset and equipment finance purchases that leverage tax incentives such as the instant asset tax write-off.

“There is ample opportunity for brokers to help SMEs within several industries that are continuing to thrive, including agriculture and transport. Federal and state governments have also allocated billions of dollars to build infrastructure over the next few years, so there’s plenty of opportunity with peripheral SMEs who’ll be looking to finance assets and equipment for these large-scale projects.”

Brokers should also be aware of improvements in the “green sector” and electric vehicles, and expect growth in asset and equipment finance in this space, says Clowes.

Broker diversification

Crevatin says the diversification drum has been beating for over a decade now, which is resulting in more brokers actively diversifying their business models.

“I think the increased number of brokers in this space is in alignment with both broker market share growth in commercial but also

businesses forming the right referral partnerships, which enables them to identify as a business with a commercial and equipment offering,” she says.

Crevatin says there’s more awareness of where opportunities are within the commercial space, and this will only increase as brokers look to replace income and opportunities in a shortening residential market.

“Lenders in the commercial space are focusing more and more on the broker opportunity. This is evident through higher educational awareness and practices by all lenders in the commercial space.”

Clowes says interest rate rises and inflation have resulted in a contraction of the housing market, with mortgage volumes slowing down.

“Mortgage brokers have had to either diversify their product and service offerings or be left behind. This is why we’ve seen record growth in mortgage brokers who now operate in commercial lending,” he says. “Savvy brokers have recognised the opportunity to expand on the lending solutions they offer to include asset finance.”

Doing so can complement brokers’ mortgage product offering, Clowes says, so they can become a one-stop shop and assist their clients with a home, car or business loan, commercial property and more.

McEvoy says brokers have been eager to diversify their customer bases, and aggregators have supported this by investing in systems and people to support asset finance growth. “Commercial lending, particularly commercial asset finance lending, is attractive to many brokers due to the relatively non-complex regulatory environment, which makes access to this segment straightforward,” he adds.

Educating brokers

Educating brokers

Brokers continue to be the primary distribu- tion channel at Resimac Asset Finance, Clowes says. “We’ve invested heavily into ensuring they – along with their customers – have an exceptional experience when using us for asset and equipment finance.”

Clowes says Resimac Asset Finance’s sales support team is nationwide and has experience in mortgage lending and asset finance, while its BDMs are some of the best in the industry and are always available to support brokers with client scenarios.

“Every broker interaction is as much an educational opportunity as it is a sales opportunity, and our BDMs are consistently building on their broker relationships to add as much value as possible to the third party channel.”

Crevatin says SFG offers a comprehensive training and education program for SFG brokers, and its lender partners provide a diverse range of educational programs within the group.

“Our Partnership Program for Lender Education drove more than 60 face-to-face educational seminars in the last 12 months – something we’re very proud of, with positive feedback and measurable results from our SFG members,” she says.

Crevatin says professional development gives SFG members the tools and strategies to identify opportunities, and strategic structuring of advice to accomplish their goals and build their businesses.

“It starts with being able to identify the opportunities, pinpointing the best way we can assist with advice, support and educa- tion, then helping them to formulate and execute the strategies for better performance and business growth,” Crevatin says.

McEvoy says Pepper Money offers one of the broadest ranges of commercial asset finance options, including solutions for a wide variety of customer types and assets.

“We’ve made it simple for brokers to do business with us, with intuitive systems, e-signing for all borrower types, and biometric ID solutions.

“We also know speed to decision and time to cash are key, which is why we continuously invest in our processes and technology to ensure we deliver market-leading capabilities for our customers and partners.”

Pepper Money actively educates its network of brokers and finance introducers at regular PD days, promoting its product and how it can support business customers, McEvoy says.

“Our BDMs work with their broker part- ners to deepen their understanding of how Pepper can help the broker’s customers,” he says. “If you’re new to asset finance, talk to your aggregator about Pepper Money’s wide range of options and how you can get started today.”