Aggregators, non-banks discuss the opportunities for brokers

It’s far too early to say when the asset and equipment finance sector will return to full health, but there are signs that a recovery is brewing and more opportunities await brokers and their customers.

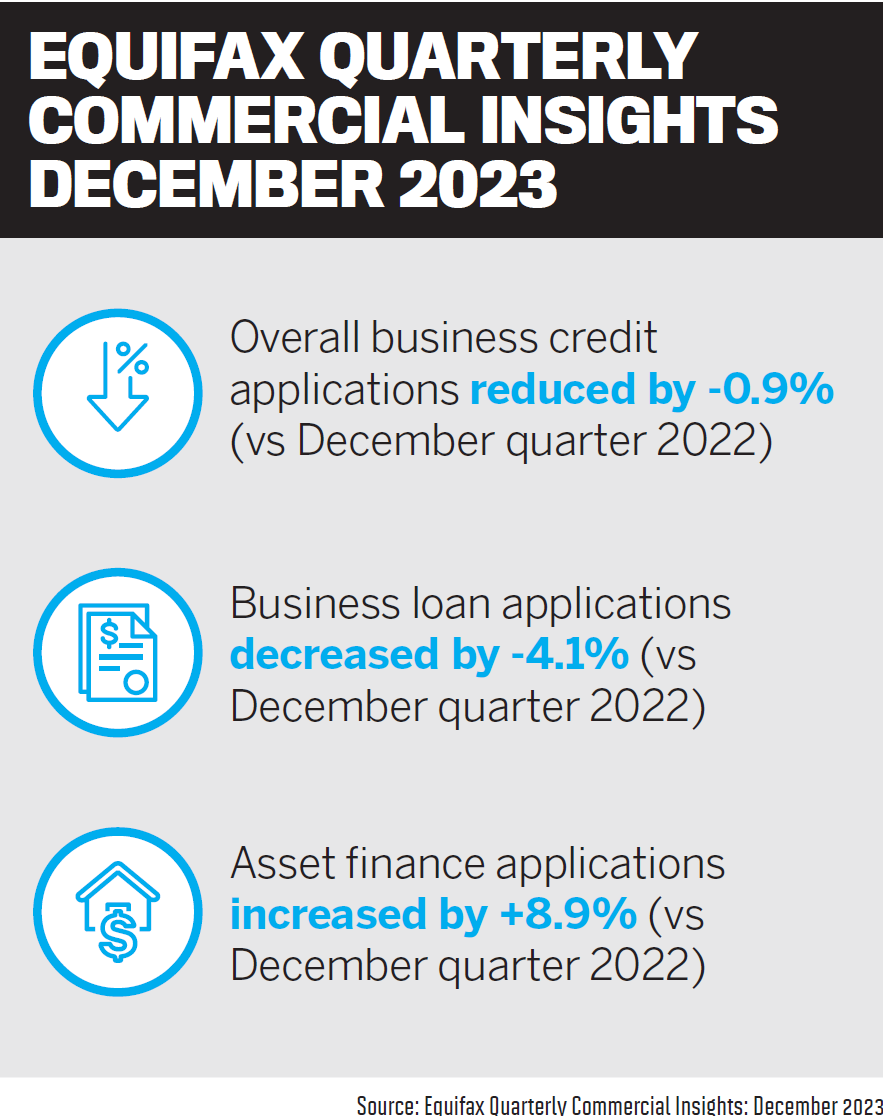

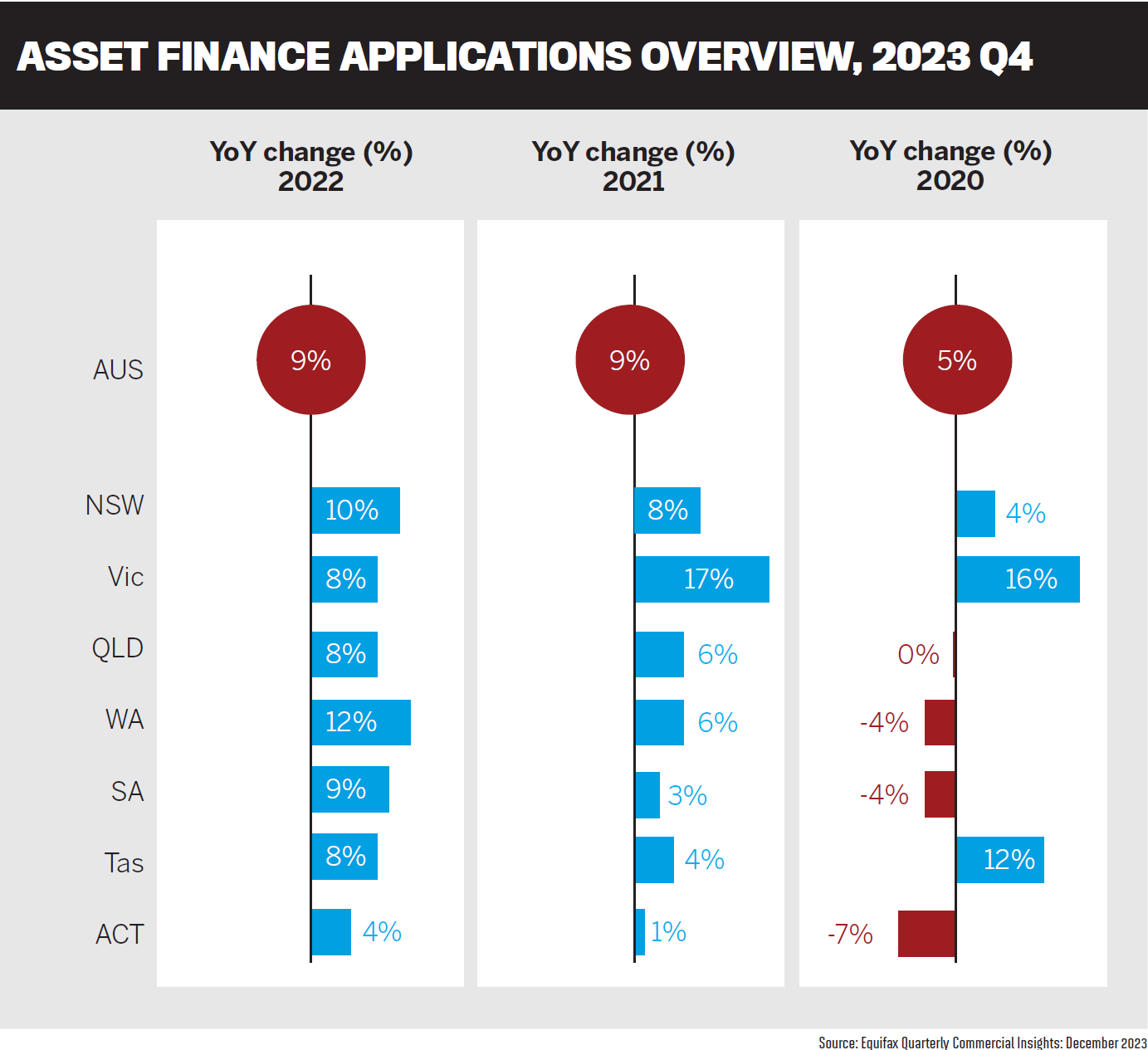

Equifax’s Quarterly Commercial Insights Report showed that asset finance applications had risen 8.9% in the December 2023 quarter compared to the Q4 2022.

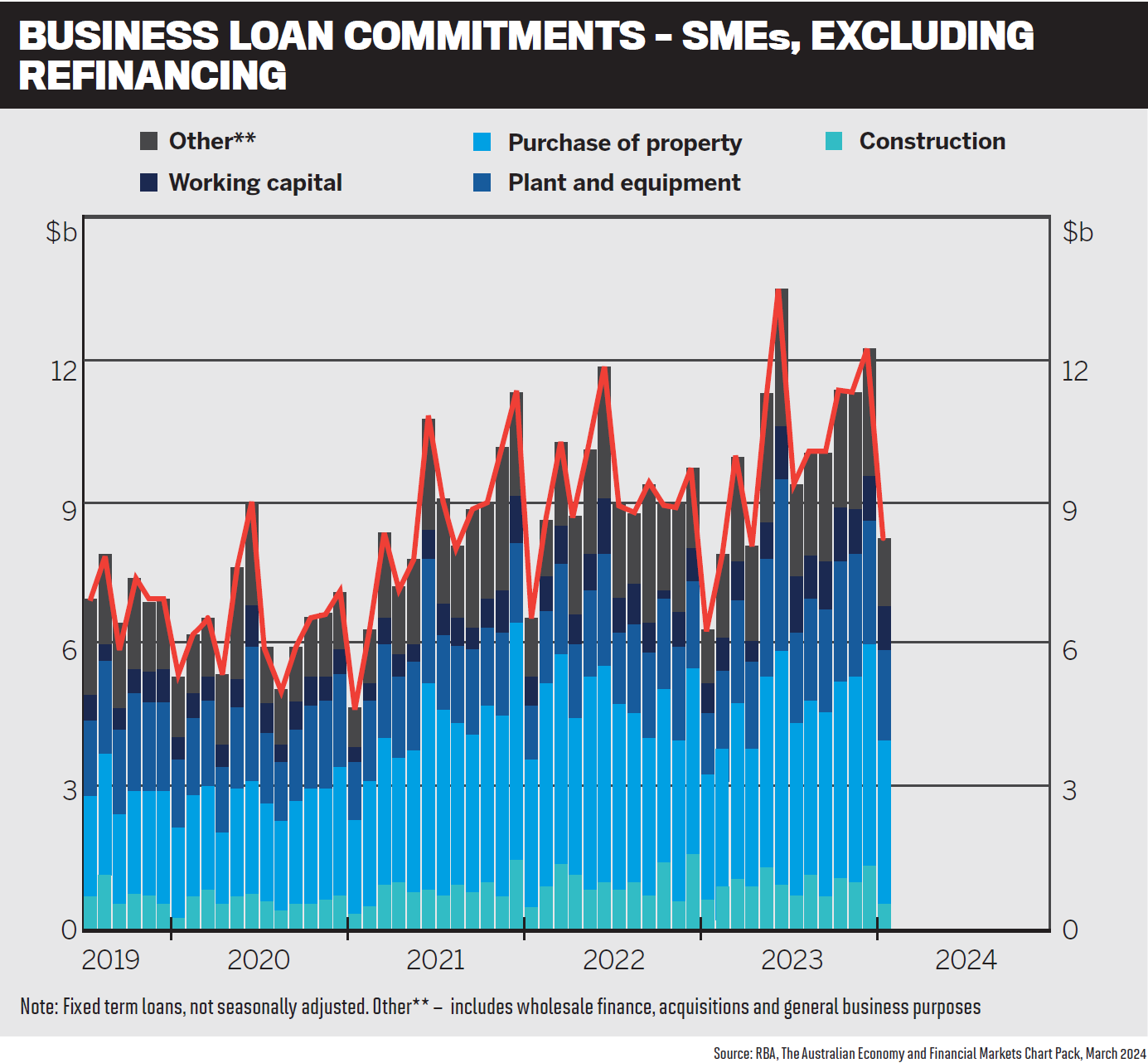

That was a much better result than business loan applications, which fell -4.1% in Q4 2023, and trade credit applications, which were down 0.4%.

Business confidence rose one point to +1 in the NAB Monthly Business Survey for March 2024, with signs that supply and demand are coming into better balance with capacity utilisation continuing to ease.

Businesses are still feeling the effects of higher costs and interest rate rises, but non-bank lenders and aggregators are reporting an increase in demand for asset and equipment finance, especially as supply chain problems ease.

To understand the market and how brokers can grow their business in this space, MPA spoke to Blake Buchanan (pictured above left), general manager of SFG; Tom Caesar (pictured above second from left), group executive – asset finance at LMG; Ken Spellacy (pictured above second from right), general manager asset finance, Pepper Money; and Danny Tuttlebee (pictured above right), head of sales at Resimac Asset Finance.

Market trends

While there was an uptick in demand for asset finance in Q4, Buchanan says over the longer term growth had been flat or declining for several years prior to the December 2023 quarter.

“So whilst the bump is great news, it is a modest improvement when averaged over a couple of years,” says Buchanan. “It is likely due to people that were holding off on new or replacement assets that had a wait-and-see mentality, with the higher cost of goods and lifting interest rates affecting their choices.

“Having more confidence with the higher cost peak nearly behind us and rate environments easing off usually spurs on activity, which is what we are seeing here.”

Caesar says the industry is experiencing a shift in demand.

“Our [LMG] asset finance brokers around Australia have reported that their SME clients are prioritising cash flow in the current environment, therefore relying more on their borrowing capabilities,” Caesar says.

Business owners have been seeking to de-risk their businesses from any negative economic impacts, such as the uncertainty around interest rates and the general economic outlook.

“They’re keen to strike a balance between cautious optimism and realistic expectations,” says Caesar.

“With recent improvements in the supply chain, access to both equipment and transport assets has been easier than in previous years, and that’s been reflected in healthy levels of enquiry and applications.”

Spellacy says despite the challenging market, Pepper Money is still seeing opportunity across various segments where there is robust demand for financing assets such as equipment, vehicles, and machinery.

Several factors are contributing to this demand, including more favourable interest rates encouraging financing activity.

“Some segments of construction and manufacturing are still experiencing growth, and we are seeing general resilience in the mining, agriculture and logistics space,” Spellacy says. “There is also most likely some post-pandemic economic recovery still occurring, with business strategically buying assets to boost productivity and drive growth.”

Tuttlebee says Resimac’s data and feedback reveal that the strong end to 2023 was helped along by record truck sales, up 7.6% on 2022.

Tuttlebee says Resimac’s data and feedback reveal that the strong end to 2023 was helped along by record truck sales, up 7.6% on 2022.

“The automotive industry also had record numbers in 2023, with sales surpassing 1.2 million new vehicle sales,” says Tuttlebee.

“This growth has been driven by several things. Continuous government spending in infrastructure is certainly a factor, as well as overseas migration increasing by a third from 2022 to 2023.”

Tuttlebee says early numbers this year already suggest a strong start for the automotive industry, with a continued increase in electric vehicle (EV) take-up, “and we’re cautiously optimistic about the economic outlook for the remainder of 2024”.

Broker partnerships

Spellacy says constant feedback from Pepper Money’s broker partners has always been: “make it easy for me to do business”.

“That feedback sits at the heart of everything we do. Because when our partners succeed, so do we.

“We are clear and consistent about our appetite and service levels, with the aim to provide certainty for our brokers. We offer a broad range of solutions for a wide range of customers, allowing brokers to consider us as a one-stop shop.”

Spellacy says Pepper Money prioritises ease of doing business by implementing intuitive systems.

“Brokers find it straightforward to engage with us. We support the broker through the life cycle of the customer, providing retention opportunities to the introducing broker when a customer is considering buying a new asset, or at key milestones in the contract term.”

Resimac prides itself on its broker relationships, says Tuttlebee.

“We have come a long way in a short period of time and one of the key drivers for this success has been our willingness to listen to brokers.

“We regularly seek broker feedback on our products and services, enabling us to provide better solutions for Australian SMEs that are seeking funding to grow their business.”

Tuttlebee says Resimac made some major product changes late last year, one of which was an increase to funding limits on its Lite Doc product.

“The feedback we received was that trucks had become more difficult to fund. Inflation had driven up prices, and meeting the higher lending requirements meant brokers had to provide full financial analysis solutions through banks.”

The Lite Doc change gave businesses access to those greater loan limits through Resimac simply by using the two most recent activity statements and tax portal statements.

“This is one of many examples where Resimac Asset Finance has developed products off the back of broker needs. One of the benefits of being a lender our size is that we can move quickly when market conditions changes,” says Tuttlebee.

Supporting the growth of its brokers is at the forefront of LMG’s activities, says Caesar.

The aggregator’s extensive events calendar features LMG professional development days, as well as asset finance and commercial-specific PD days.

“We provide brokers with access to a range of online training courses and opportunities to network, upskill and educate themselves in the ever-changing finance industry,” Caesar says.

LMG also provides its brokers with leading technology solutions, including integration of MyCRM and Nodifi, allowing asset finance, commercial and residential deals to be written and housed in the one platform.

This centralised platform enhances brokers’ productivity, freeing up their schedules to spend more time supporting their clients.

Caesar says LMG’s holistic marketing suite, including email communications, reviews and social media content, not only allows brokers to nurture relationships with clients, but also expand their reach and grow their business.

Buchanan says brokerages are becoming more sophisticated, scaled and diversified, allowing for deeper customer discussions around clients’ more wholistic financial needs.

“When consumers don’t think something can be done, they don’t do it. When a customer is given credit advice that would be of benefit to them, they will usually act on it.”

Buchanan says SFG brokers experienced significant year-on-year growth and the demand for more asset and equipment accreditations has never been greater.

“Our brokers are also seeing greater levels of enquiries from new and existing clients. This points to both an increase in market share but also some consumers who have paused their property finance aspirations to pursue other investments and finance requirements for their business purposes.”

Diversification routes

Tuttlebee highlights the value of diversifying for mortgage brokers, with the most obvious route being to provide customers with asset finance solutions, “whether they’re PAYG clients who need a car to get the kids to weekend sports, or it’s the $300,000 prime mover that their truck driver client needs to take on a new and more lucrative contract”.

Resimac, a well-known non-bank mortgage business, did exactly this three years ago when it diversified into asset finance.

“Our initial offering focused on lending solutions in commercial asset finance, but we’re growing our product offering quickly. We recently launched our mortgage security-backed short-term business loan (SBL), and later this calendar year will see us launch our consumer product and then move into novated leasing,” says Tuttlebee.

Resimac’s asset finance team has grown nearly 10 times in three years, with several internal account managers and broker support staff on hand to assist mortgage brokers with moving into commercial asset finance.

This support can include helping brokers with a quote for their clients, packaging together a Resimac deal, walking them through the simplified processes, and providing a deeper understanding of not only the products “but why we may be asking for certain information or paperwork”.

Spellacy says it’s a great time for brokers to consider how they diversify into asset finance and support customers seeking access to asset finance solutions.

“First port of call for a broker should be with their aggregator. Aggregators can provide a broad range of information, training and support to a broker looking to diversify. Many aggregators offer different customer application pathways like spot-and-refer programs.”

Spellacy advises brokers to familiarise themselves “with the asset types that your customers will require”.

Many residential mortgage customers may be considering an EV, so brokers need to become experts in this fast-expanding segment.

“Commercial clients will often require equipment finance on a regular basis, so it’s worthwhile understanding how you can best support them across their changing needs,” says Spellacy.

“Gradually start to introduce asset finance into your business and build out strong customer processes and journeys to ensure your customer is getting a great experience.”

Buchanan says that when it comes to diversification, SFG “takes the approach of education, connections and strategy”.

“Education empowers brokers with what can be done and identifies the opportunities that are within their current model, along with the open market.

“Connections is about the right partnerships with the right people and providers. The strategy is about planning, implementing and making sure you have the right structure to execute against that and steer you towards your goals.”

Buchanan says SFG operates a busy education program at specific commercial and asset PD days, conventions and other events such as webinars and content libraries.

“It is one thing to know about it, but how you implement it is equally as important. This is where we take an individual approach with our members to assist them with their plans and implementation around business growth, improvements and diversification.”

Caesar says LMG supports brokers to diversify into asset and commercial finance in multiple ways.

Its newly created Referrer to Writer program is an intensive course for residential brokers who are currently referring asset finance deals but want to transition to writing their own.

The program is facilitated by the knowledgeable business success managers (BSMs) of LMG Asset Finance, helping brokers to build the capacity to write those deals internally.

“Our central learning and development platform, Brokerversity – exclusively available to LMG brokers – also educates brokers so they can diversify into asset finance and commercial finance, successfully,” says Caesar.

The library of online courses and webinars provides demonstrations and best practice insights from LMG experts.

Integrations with MyCRM and Nodifi create a “single source of truth to give brokers a 360-degree view of their customers across residential, commercial and asset finance on the one platform”.

Growth trajectory

Caesar says any cash rate movements will affect borrowing costs and influence market sentiment.

“In the next 12 months, various factors will influence growth in asset and equipment finance and the impacts will be different across separate sectors. For instance, in agriculture, farm equipment financing could see growth due to advancements in technology, the need for modernisation and recent seasonal conditions,” he says.

In the mining sector, demand for equipment finance may rise with increased exploration and extraction activities.

“We’ve seen dealerships offering discounts on vehicles and that could stimulate growth in the automotive sector,” says Caesar.

“Government incentives for the purchase of electric vehicles could encourage increased financing demand.”

Buchanan says broker market share will continue to grow in this sector, as a direct result of brokers continuing to upskill and diversify.

He says the general easing of costs with inflation coming down, the costs of goods easing and more cash available due to tax reform will result in increased consumer confidence and capacity to purchase.

“This will of course result in higher activity and more financing of goods in the near term.”

The EOFY will also trigger activity as businesses either fit new purchases into the current tax year or wait to acquire equipment in the new financial year.

“Brokers should be prepared for this and be proactive with their client communications to make sure they are at the forefront of their clients’ minds for these inevitable purchases,” Buchanan says.

Tuttlebee says in the forthcoming year, asset and equipment finance are poised for growth in certain areas. Several factors will be instrumental in shaping this growth – most notably the focus on reducing carbon emissions.

“Electric vehicle sales have surged, nearly tripling in growth between 2022 and 2023. This emphasises a groundswell of interest in cleaner transportation solutions,” he says.

Tuttlebee says government spending on infrastructure projects is expected to remain robust. However, the asset finance industry is not completely out of the woods just yet, with larger construction companies – which previously drove a sizeable portion of sales in this market – still grappling with the repercussions of the pandemic, he says.

“The good news is that construction is going to pick up again soon. Housing shortages and a growing migrant population means the demand for property is only going to get stronger, and this will drive a steady flow of new construction projects.

“Businesses that win the tender for these upcoming projects are great candidates for asset finance solutions.”

Spellacy says new car sales serve as a strong barometer for the industry’s health.

“We continue to witness remarkable records being set for car sales. Nine of the last 12 months have been a record for new car sales, which is an indicator that the supply constraints the pandemic caused have gradually eased.”

EV and hybrid sales also outperform expectations, says Spellacy.

“As we fast approach the end-of-financial-year period, the impact of the tax write-off scheme will come into play.”

He says although the current tax write-off scheme is less favourable than in 2023, “we are seeing some significant improvement in other factors, such as interest rates easing, and inflation being at lower levels compared to the same period last year”.

What trends are you seeing in asset and equipment finance demand from clients? Comment below