What caused mortgage rates to fall last month—and how long will the slide last?

Homebuyers in Canada experienced a rare improvement in affordability last month as declining mortgage rates eased financial burdens in several key markets across the country.

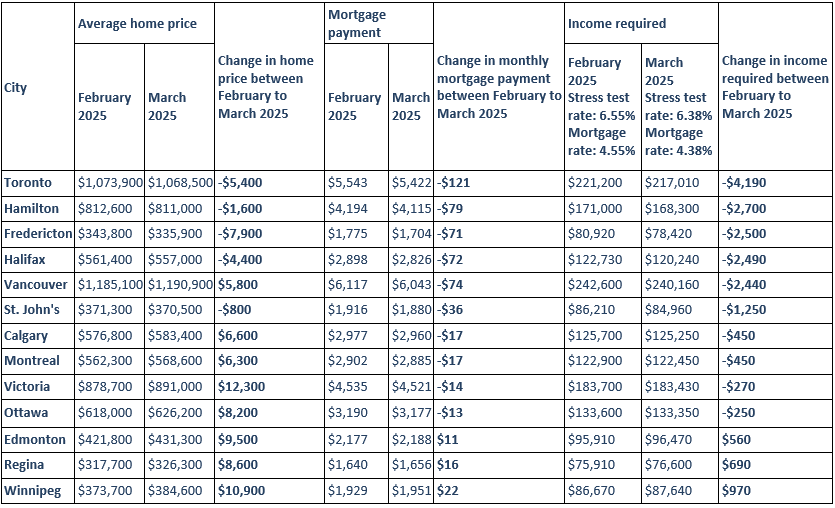

According to Ratehub.ca’s March 2025 Home Affordability Report, affordability improved in 10 out of 13 major cities, thanks to a combination of lower mortgage rates and softened home prices. The report calculates monthly changes in the income required to purchase a home, factoring in real estate prices, mortgage stress test rates, and borrowing costs.

“Buying conditions improved in 10 of 13 markets, largely due to falling mortgage rates,” the report stated.

Ratehub.ca noted that the decline in borrowing costs followed a short-lived but impactful imposition of 25% US tariffs on Canadian goods. Although the tariffs were reversed within 30 days, the initial announcement caused significant movement in the bond market. The US 10-year Treasury yield fell to 4.16%, dragging Canadian bond yields down with it. As a result, Canadian lenders dropped their five-year fixed mortgage rates, with the lowest insured option falling to 3.84%.

This downward trend in mortgage rates led to a reduced average stress test rate of 6.38%—down from 6.55% the previous month—making it easier for more Canadians to qualify for financing.

How much income is needed to afford a home?

Among the most improved regions was the Greater Toronto Area (GTA). The average price of a home in Toronto dropped by $5,400, to $1,068,500. Consequently, the required annual income to purchase such a home fell by $4,190, while average monthly mortgage payments dipped by $121.

Hamilton also saw gains in affordability, with home prices decreasing by $1,600 to an average of $811,000. The income needed to afford a home in the city fell by $2,700.

On the East Coast, Fredericton saw a notable shift. The city’s average home price fell by $7,900 in March, which led to a $2,500 reduction in the required income and a $71 drop in the average monthly mortgage payment.

March 2025: Home affordability report

Data is based on a mortgage with a 10% down payment, 25-year amortization, $4,000 annual property taxes and $150 monthly heating. Mortgage rates are the average of the Big Five Banks’ 5-year fixed rates in February and March 2025. Average home prices are from the CREA MLS® Home Price Index (HPI). (Source: Ratehub.ca)

Outlook

Experts caution that the outlook remains uncertain. Bond yields, which heavily influence fixed mortgage rates, have begun to rise again as investor confidence in US fiscal policy wanes.

At the same time, the Bank of Canada opted to hold its overnight lending rate at 2.75% in April, keeping variable mortgage rates stable. Despite lower-than-expected inflation in March, the central bank emphasized its commitment to monitoring economic risks tied to tariffs and inflation volatility.

“Our focus will be on ensuring that Canadians continue to have confidence in price stability,” the Bank stated in its April announcement.

What are your thoughts on the latest findings? Share your insights in the comments below.