New data suggests a key indicator is rising

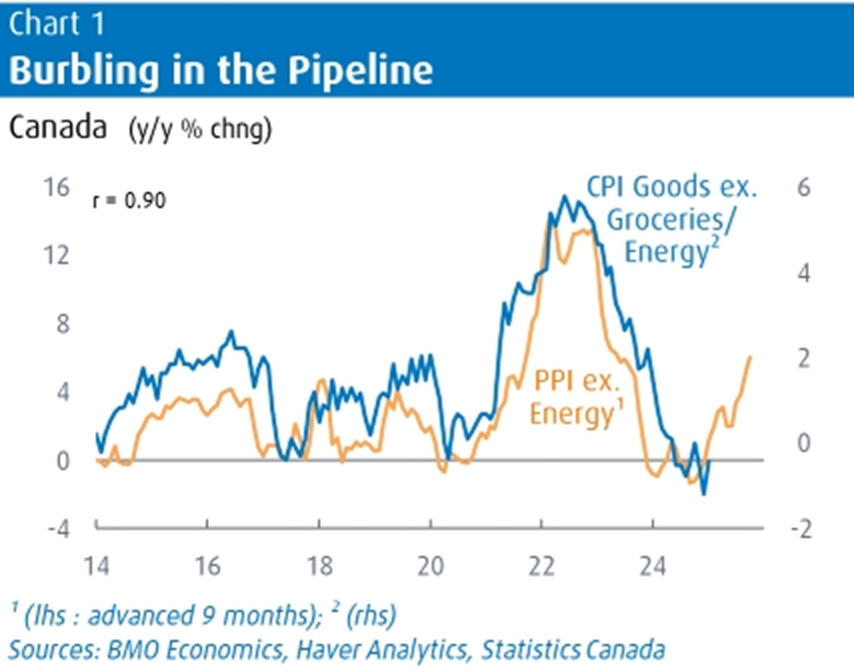

Inflationary pressures in Canada may persist longer than anticipated, according to an analysis from BMO Economics. A newly released chart titled “Burbling in the Pipeline” suggests that producer prices and consumer inflation remain closely linked, raising concerns that inflation could remain elevated despite recent declines.

The data, sourced from Statistics Canada and Haver Analytics, tracks the year-over-year percentage change in Canada’s Producer Price Index (PPI) excluding energy and the Consumer Price Index (CPI) for goods excluding groceries and energy. BMO’s analysis highlights a strong correlation (r = 0.90) between the two indicators, with producer prices typically leading consumer prices by approximately nine months.

The chart reveals that after a significant decline in both PPI and CPI inflation in late 2023 and early 2024, producer prices have begun to rise again. This suggests that consumer price inflation may follow a similar upward trend in the coming months, potentially complicating efforts by the Bank of Canada to achieve price stability.

BMO senior economist Sal Guatieri noted that, while Canadian inflation has largely remained under the radar compared to the US, recent trends indicate underlying price pressures remain stubborn. January’s CPI data showed only a modest 0.1% month-over-month increase, aided by a temporary sales tax holiday, but core inflation metrics continue to hover above the Bank of Canada’s 2% target.

“Simply put, underlying inflation is sitting uncomfortably above the 2% target, which likely explains the BoC’s hesitancy to fan rate-cut expectations,” Guatieri said.

Further pressure is emerging from producer prices, which surged 1.6% month-over-month in January. Excluding energy, producer prices rose 0.9% and have been increasing at an annualized rate of 9.3% over the past four months. A weaker Canadian dollar and higher commodity prices, particularly metals, have contributed to these pressures. The Bank of Canada’s core ex-energy index has risen 8.3% in the past year, suggesting that the mild deflationary trend in consumer goods prices may be coming to an end.

With CPI services inflation still running at 2.8% year-over-year and accounting for over half of household spending, inflation risks remain tilted to the upside. Guatieri warned that stronger job growth and solid income gains could encourage businesses to raise prices further. Additionally, despite a rise in the unemployment rate, overall job creation remains robust, meaning consumers may be more willing to absorb higher costs.

“The upshot is that, while we still expect the BoC to reduce rates a further 50 bps this year, the inflation data provide cover should it decide to hold off in March,” Guatieri said.

As inflation concerns mount, all eyes will be on upcoming economic data to gauge whether price pressures are truly subsiding or if further monetary tightening remains on the table.

Any thoughts on the recent analysis? Let us know in the comments below.