Elevated interest rates continue to have an outsized impact on affordability, new report says

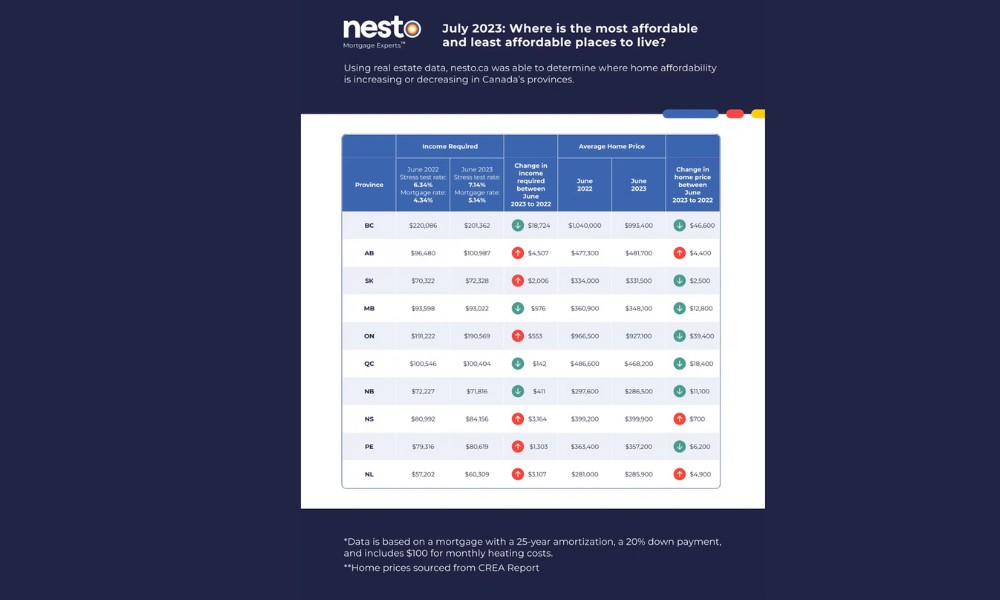

While home price declines were registered in seven out of 10 Canadian provinces as of this month, affordability improved only in four out of 10 provinces due to sharp increases in mortgage interest rates, according to a new analysis by nesto.

“It is clear that the housing market was negatively impacted by the latest Bank of Canada rate hike on July 12,” nesto said. “It increased the prime rate to 5.0%, and the lender’s best five-year fixed today stands at 5.14% compared to 4.64% in June 2022.”

“As long as interest rates remain at these levels, or continue to rise, we will still see issues at the income affordability level,” said Chase Belair, co-founder and principal broker at nesto.

In its analysis, nesto also examined the impact of the last 10 BoC rate hikes in particular. Assuming a home valued at $300,000 with a five-year fixed rate and a 25-year amortization, mortgage payments in March 2022 had an even split with $661 going towards principal and $661 going towards interest, for a monthly total of $1,322. The income required to secure this mortgage was a rather accessible $80,100.

In stark contrast, a mortgage payment of $1,710 on July 2023 will only have $463 going towards principal, while the remainder will be towards interest. The required income to secure such a loan is currently at $94,800.

Canada’s household debt-to-income ratio declined by 3.8 points to 180.5% on a seasonally adjusted basis in Q4 2022, from an upwardly revised 184.3% in the prior quarter, according to BMO Economics.https://t.co/EScJTZyFVT#mortgage #mortgagetrends #income #debt #household

— Canadian Mortgage Professional Magazine (@CMPmagazine) March 16, 2023

Still, Belair believes that the market might enjoy some relief in the near future.

“While I can’t predict the future, it appears that rate hikes should slow or home to a halt in 2024, giving a much-needed reprieve to first-time home buyers as well as current home owners,” Belair said.

At the same time, nesto stressed that such a policy easing might still be some way off.

“As we look to August 2023’s report, we expect a similar pattern to appear: Home prices will continue to level out, but with higher rates, income affordability will be brought into question,” nesto said.