Expert notes homeownership becomes tougher, despite stable borrowing costs

Mortgage affordability worsened in 12 out of 13 major Canadian cities in January 2025 as home prices climbed and fixed mortgage rates remained stable, according to Ratehub.ca’s latest affordability report.

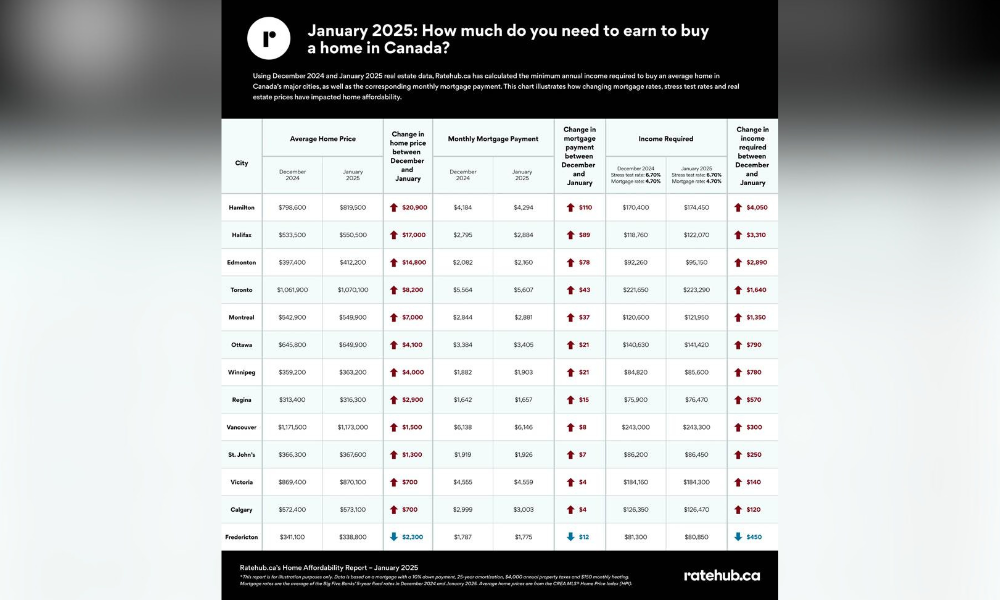

The report, which calculates the income required to qualify for a mortgage on an average-priced home, found that rising home prices were the primary factor behind declining affordability. While mortgage rates remained unchanged at an average of 4.7% for a five-year fixed term and a stress test rate of 6.7%, the cost of homeownership increased in most major markets.

Hamilton faces the largest affordability decline

Among the cities surveyed, Hamilton saw the most significant affordability decline. The average home price increased by $20,900 to $819,500, requiring an additional $4,050 in annual income to qualify for a mortgage. Monthly mortgage payments also rose by $110, equating to an additional $1,320 per year.

“Home prices increased significantly in the majority of the cities we looked at, which caused home affordability to worsen,” said Penelope Graham, mortgage expert at Ratehub.ca. “Since mortgage rates stayed the same month-over-month, home prices were the primary driver for the decline in affordability.”

Other cities that experienced notable affordability declines included Halifax, where homebuyers needed an additional $3,310 in annual income, and Edmonton, which saw a $2,890 increase in required income.

Fredericton sees a rare improvement

Fredericton was the only city where affordability improved. The average home price fell by $2,300 to $338,800, reducing the required income by $450 and lowering the monthly mortgage payment by $12.

Toronto and Vancouver experience modest increases

Toronto and Vancouver saw relatively modest increases in required income. Toronto’s average home price rose by $8,200 to $1,070,100, increasing the required income by $1,640 and the monthly mortgage payment by $43. Vancouver’s average home price increased by $1,500 to $1,173,000, requiring an additional $300 in income and adding $8 to the monthly mortgage payment.

Mortgage market outlook

While mortgage rates remained unchanged in January, external economic factors may influence future rate movements, Ratehub.ca noted. The Bank of Canada’s recent interest rate cut had little immediate effect on fixed mortgage rates, which remained stable due to elevated bond yields. However, future rate decisions will depend on inflation trends and GDP reports.

“It’s also looking more likely that variable mortgage rates will be unchanged for the next month. The latest Canadian inflation numbers showed the Consumer Price Index rose to 1.9% in January, up from 1.8% in December,” Graham noted. “As a result, the central bank is now more likely to pause on cutting its benchmark overnight lending rate – which lenders use to price their prime rates and variable lending products – in its next rate announcement on March 12, after cutting it six consecutive times since June.”

Any thoughts on this story? Let us know in the comments below.