RBNZ OCR cuts: What's happening and why?

The Reserve Bank (RBNZ) has taken decisive action to address a slowing economy and cooling inflation, cutting the OCR three times in recent months.

After holding the OCR at a 15-year high of 5.5% between May 2023 and August 2024, the central bank implemented a 0.25% reduction in August, followed by consecutive 0.5% cuts in October and November.

Nick Tuffley (pictured above), ASB chief economist, believes RBNZ is now over halfway through its easing cycle, with further cuts likely to follow in 2025.

However, Tuffley warns that interest rate markets remain volatile, impacting mortgage strategies.

“It’s not a one-way street to lower mortgage rates,” Tuffley said, highlighting the need for borrowers to stay informed of ongoing risks.

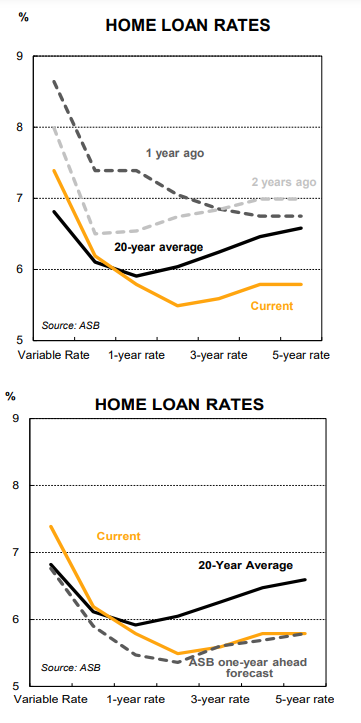

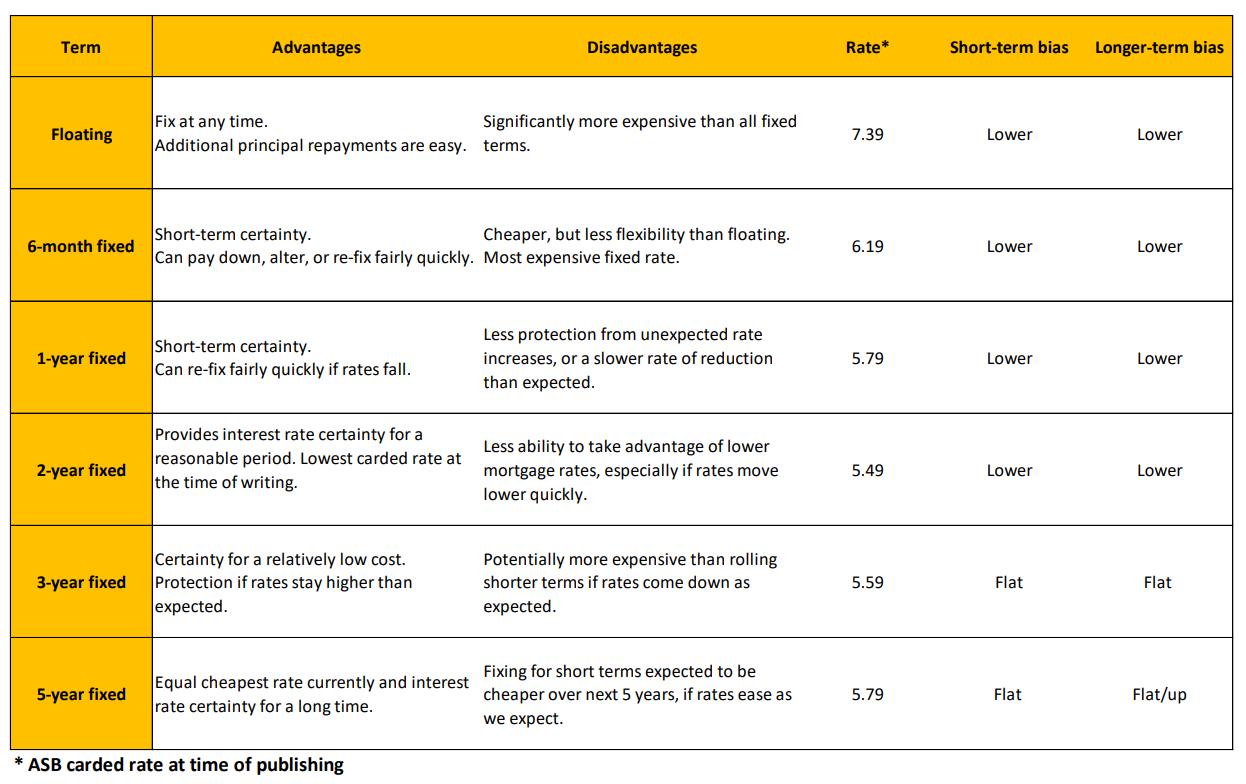

Short vs long-term mortgage rate drivers

The key influences on mortgage interest rates include the OCR, international rates, and bank funding costs. These factors affect short- and long-term rates differently.

Shorter-term rates (floating or one-year fixed)

The softening labour market and weakened business profitability signaled OCR cuts in mid-2024, prompting early declines in wholesale and fixed mortgage rates. Recent cuts have further eased short-term fixed rates, and ASB expects a continued downward bias through the first half of 2025.

Longer-term rates (two years or more):

Global central banks, including the Reserve Bank of Australia, are approaching or already initiating rate cuts. Longer-term New Zealand mortgage rates have eased this year but may remain stable, as current five-year rates are already below their 20-year average. ASB expects the focus of any declines to stay in the one–two-year fixed terms.

Choosing the right mortgage strategy

Selecting the best mortgage strategy remains complex amid current conditions. Floating and short-term fixed rates offer flexibility for borrowers who want to reassess their loan structures or pay off debt soon.

In contrast, longer fixed terms provide greater certainty and, unusually, now carry lower rates than shorter terms.

Tuffley advises borrowers to carefully weigh their priorities, balancing cost, flexibility, and interest rate certainty.

“It is important to weigh up your own priorities and make the mortgage choice that looks best aligned with your needs,” he said.

ASB also cautioned that while further rate cuts are expected, inflation risks or economic shocks could cause rates to hold steady or rise.

Borrowers should focus on aligning their mortgage structure with their personal budgets, risk tolerance, and long-term goals.

For guidance, ASB encourages customers to consult their mortgage experts at 0800-100-600 or explore online tools, such as mortgage calculators, for tailored solutions.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.