First-home buyer activity slips as investors regain ground in NZ property market

The dynamics of New Zealand’s property market are evolving, with new data revealing a softening in first-home buyer (FHB) activity and a rebound in investor confidence, as falling interest rates and renewed buyer confidence fuel increased borrowing.

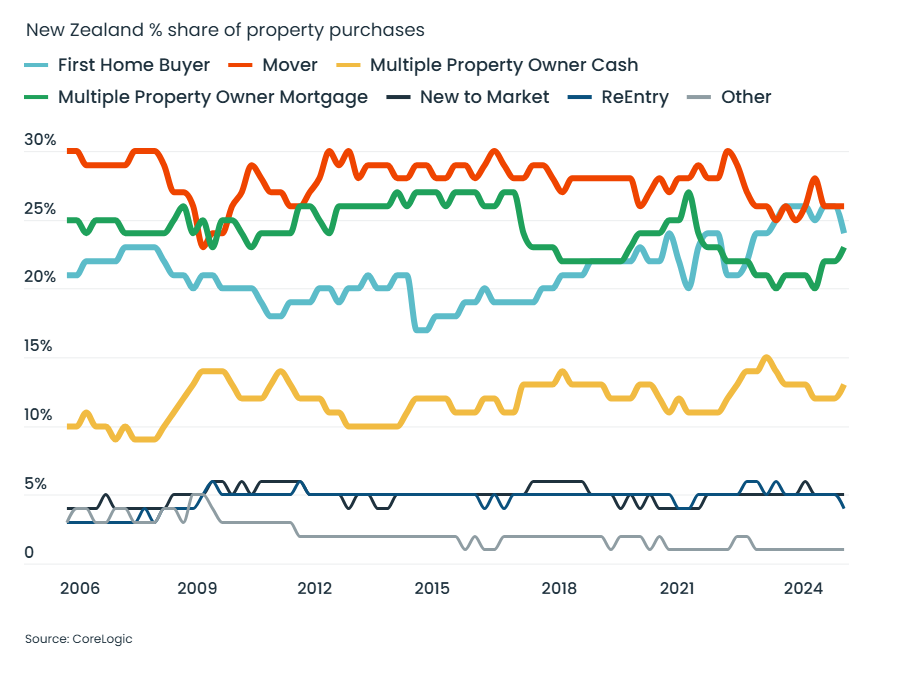

According to CoreLogic NZ chief economist Kelvin Davidson (pictured), FHBs accounted for 25% of residential purchases in the first quarter of 2025—down from 26% in Q4 2024 and the lowest level since early 2023.

Meanwhile, relocating owner-occupiers (movers) made up 26% of transactions, while investors—both cash buyers and those with mortgages—expanded their presence.

Cash-backed multiple property owners (MPOs) represented 14% of activity, while mortgaged MPOs took a 23% share.

While these shifts are broadly consistent nationwide, Wellington stands out as an exception. Across the wider region—including Lower and Upper Hutt, Porirua, and Wellington City—FHBs maintained a strong 35% share.

“An obvious factor here will be the relative weakness of Wellington property values (and improved affordability), which is likely playing into the hands of FHBs, provided they feel confident about their job security,” Davidson said.

Why investors are re-entering the market

Lower interest rates appear to be the key catalyst.

As mortgage rates dropped from over 7% to under 5% in the past 6–9 months, investors have found buying rental properties more financially viable.

Reduced deposit requirements (from 35% to 30%), a shorter Brightline test, and the full return of mortgage interest deductibility have also made conditions more favourable.

“The biggest shift in favour of mortgaged investors has simply been the reduction in the size of the top-ups that are generally required out of other income for a rental property purchase,” Davidson said.

What once might have cost $400 per week to support is now closer to $200—still a stretch, but far more accessible.

Recent trends showed that it’s primarily smaller investors—so-called “mums and dads”—driving the resurgence.

Mortgaged MPO-2s (those who now own two properties) have climbed from 6% to 8% of the market since mid-2023, while MPO 3–4s have also increased their share.

New builds lose some appeal for investors

Investor interest in new-build homes has slightly waned. In 2023 and 2024, mortgaged investors accounted for 30% and 29% of new-build purchases, respectively.

So far in 2025, that figure has dipped to 27%. This could reflect the now more balanced tax treatment of older homes, as interest deductibility changes have eroded the financial advantages of buying new.

With a wider range of listings available, existing homes may now offer better value—and more negotiating power—for investors.

What’s next for buyers?

The broader trend anticipated by market watchers—that FHBs would lose some ground in 2025 while investors recover—is unfolding. However, the dip in market share doesn’t mean fewer FHBs will buy homes overall.

CoreLogic expects around 10,000 more sales in 2025 compared to 2024, meaning more buyers across the board. FHBs still benefit from bank allowances for low-deposit lending and access to KiwiSaver for deposits.

Meanwhile, investors—buoyed by better cashflow and global uncertainty—may continue to see real estate as a safer bet compared to shares or bonds.