Latest NZ retirement guidelines enhance financial advising Strategies

The 13th edition of the New Zealand Retirement Expenditure Guidelines, published by Massey University’s Financial Education and Research Centre in collaboration with Financial Advice New Zealand (FANZ), offers fresh insights into the financial behaviours and needs of retired New Zealanders.

These insights are crucial for financial advisers tasked with guiding clients through the complexities of planning for retirement.

Adapting to economic changes

This latest edition highlighted the dynamic requirements of retirement planning, suggesting the necessity for ongoing adjustments in response to economic fluctuations.

As generations approach retirement age, from Gen X to Millennials, the guidelines stress the importance of proactive and continuous financial planning.

Financial planning essentials

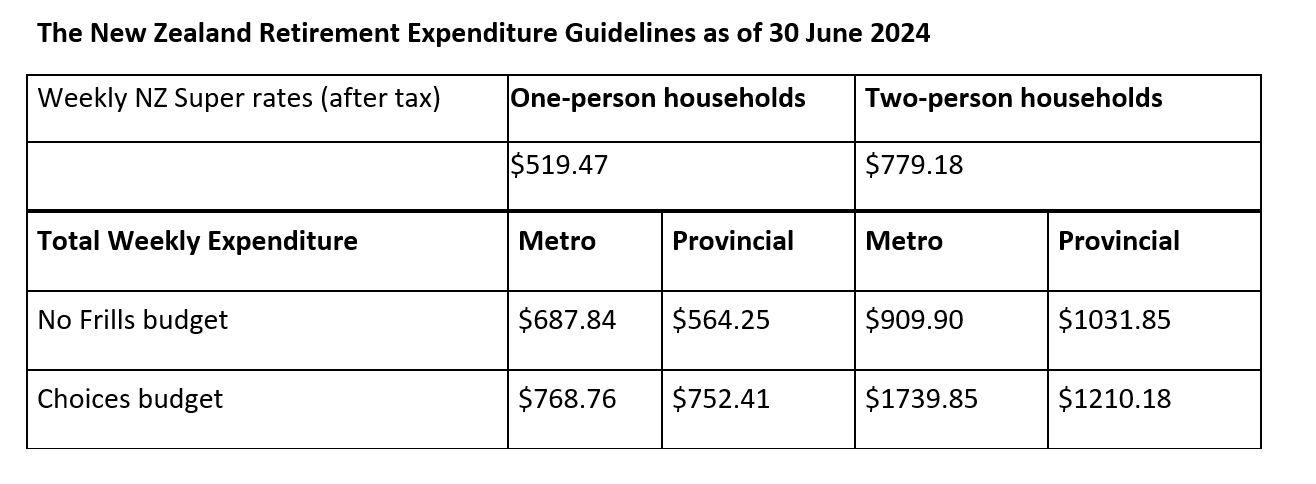

The guidelines serve as a resource for understanding actual expenditure levels among retirees, which is vital for preparing realistic budgets and saving strategies.

This data helps individuals tailor their retirement plans to meet desired lifestyle goals and to calculate the necessary savings to fund these ambitions.

Addressing longevity risk and inflation

One significant issue highlighted in the report is the longevity risk – the possibility of outliving one’s savings.

The guidelines provide strategies to manage this risk to ensure sustained income throughout retirement. They also detail the impacts of inflation on retirement spending, underscoring the importance of diverse income sources beyond NZ Superannuation.

FANZ insights

FANZ CEO Nick Hakes (pictured above) remarked on the value of the guidelines.

“Our members play a critical role in helping individuals navigate these complexities,” Hakes said.

“The data and insights from the guidelines equip advisers with information on spending patterns and the financial needs of retired New Zealanders, to assist with providing tailored professional advice that addresses longevity risk, optimizes savings, and ensures a comfortable retirement.”

Claire Matthews, associate professor from Massey University, also noted the necessity of adapting savings strategies to changing economic conditions to meet retirement goals.

Key findings and implications

- Many New Zealanders aspire to a retirement lifestyle that exceeds what is possible with NZ Superannuation alone, and many achieve this through various income sources.

- Annual expenditure increases were between 1.80% and 3.46%, influenced primarily by housing, transport, and insurance costs.

- Concerns about “fear of running out” (FORO) can lead to over-saving, potentially diminishing quality of life, while also posing the risk of under-spending in retirement despite having sufficient funds.

Life expectancy considerations

The uncertainty of life expectancy remains a core concern in retirement planning. Influenced by genetics, lifestyle, gender, ethnicity, and socioeconomic status, life expectancy varies, impacting retirement planning strategies.

The availability of NZ Superannuation as a guaranteed lifetime annuity provides a critical safety net against longevity risk.

These updated guidelines serve as an indispensable tool for financial advisers, enabling them to provide well-informed, precise advice tailored to the unique needs of each retiree, thereby fostering financial security and comfort in later years.