New metric tracks first-home buyers

Infometrics is adjusting how it tracks first-home buyer activity after the government ended the Kāinga Ora First Home Grant scheme in May.

The new First Home Loan metric will replace the discontinued grants in Infometrics’ Quarterly Economic Monitor to reflect changes in first-home buyer trends more accurately.

“We previously used Kāinga Ora First Home Grants (FHGs) in the Quarterly Economic Monitor as a measure of first-home buyer activity,” said Nick Brunsdon (pictured above), principal economist at Infometrics. “However, with the grant scheme scrapped, we are introducing a new indicator – First Home Loans.”

How First Home Loans measure buyer trends

The First Home Loans metric, previously known as Welcome Home Loans, offers more flexibility by providing territorial-level data.

These loans require a deposit as low as 5%, helping borrowers with limited savings enter the housing market.

This approach contrasts with First Home Grants, which were subject to strict eligibility limits based on income and house prices.

Differences in first-home buyer data sources

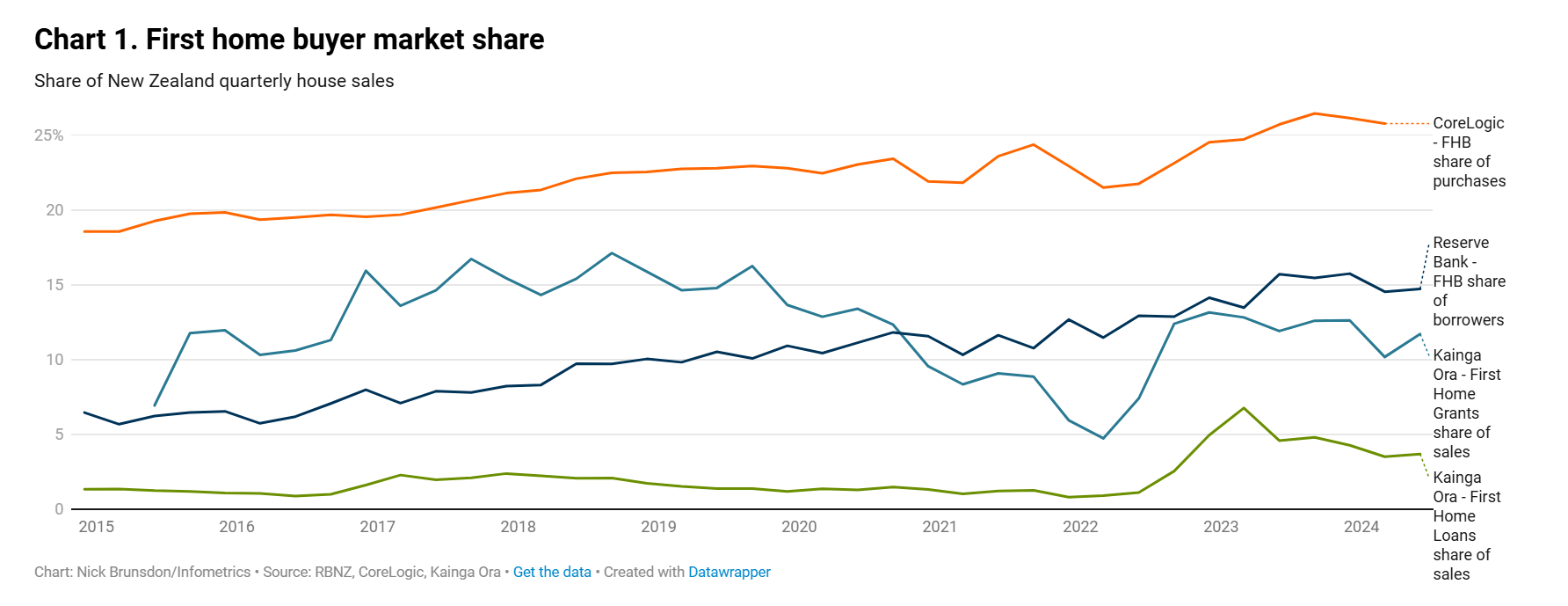

Various agencies, including the Reserve Bank, Kāinga Ora, and CoreLogic, collect data on first-home buyers, each offering a slightly different perspective.

- Reserve Bank: Tracks first homebuyer loans but excludes buyers co-purchasing with someone who owns property.

- CoreLogic: Identifies buyers by checking whether their name has appeared on a title before, reporting national trends but lacking detailed local breakdowns.

- First Home Loans: Captures a subset of buyers with lower deposits but offers a local-level perspective that can highlight regional trends.

“First Home Loans will undercount overall first homebuyer activity, but the local-level data provides valuable insight into regional trends,” Brunsdon said.

Regional disparities in home buyer access

The effect of ending the First Home Grant varies across regions, as housing affordability influences grant and loan uptake differently.

In areas with more affordable homes, such as those with house price-to-income ratios well below the national average of 7, the grants were used in more than 19% of purchases.

Conversely, in higher-priced areas like Thames-Coromandel (where the ratio is 14.6), the grant was used in only 6.5% of transactions, with no First Home Loans recorded.

First-home buyers pay less than market average

First-home buyers typically purchase properties priced between the lower quartile and median house prices, according to CoreLogic’s analysis for Q1 2024. This suggests buyers are choosing homes that are below the market median but not the cheapest options available.

Cheaper homes may require higher deposits due to deferred maintenance, insurance issues, or unusual ownership structures.

Deposits surpassing expectations

Surprisingly, the average first-home buyer deposit in 2024 was 29%, well above the standard 20% deposit requirement and far exceeding the 5% allowed under the First Home Loan scheme.

“This demonstrates the variety of financial situations among first homebuyers,” Brunsdon said. “Not all buyers are scraping by, though larger deposits are often necessary in more expensive regions.”

New loan data to feature in reports

The Kāinga Ora First Home Grant measure will be discontinued in Infometrics’ next Quarterly Economic Monitor, set to be released on Nov. 21. The updated report will instead feature First Home Loan data, offering fresh insights into regional first-home buyer activity.

Brunsdon encouraged subscribers to explore the new series.

“We would encourage Quarterly Economic Monitor subscribers to have a look at the First Home Loan series for their area and get in touch if they have any questions,” he said.

For more details, visit the Infometrics website.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.