Underlying inflation pressures are proving to be "superglue sticky," economists say

The latest inflation news is “good news” overall, but the bad news is, “underlying inflation pressures, particularly the domestic-driven parts, are proving to be very sticky,” according to ASB economists.

The latest annual inflation data from Stats NZ revealed a 6% rise in the consumers price index in the 12 months to June, slightly higher than market expectations of 5.9%, but weaker than the Reserve Bank’s May MPS forecast of 6.1%. Headline inflation is lower compared to the 7.3% annual peak recorded in mid-2022.

“Non-tradable inflation, at 6.6% yoy, was stronger than we and the RBNZ had forecast,” said Nick Tuffley (pictured above), ASB chief economist.

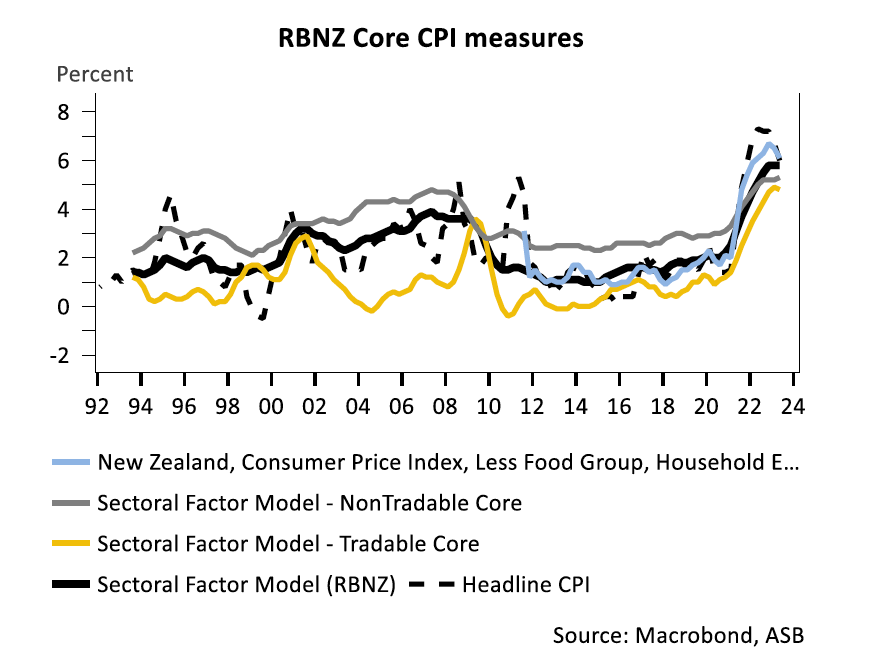

“Some of the strong drivers (housing construction and maintenance cost, rents, insurance) could be weather-related, and the RBNZ may be prepared to wait and see. Even so, other various measures of core inflation (see chart below) showed a degree of stubbornness and confirmed elevated domestic inflationary pressures were yet to cool.”

The ASB economists said that while the Q2 CPI was not a “smoking gun” that would prompt RBNZ to imminently lift rates, “the risks are still tilted towards the OCR peaking above 5.5% this cycle.”

The upcoming Q2 labour market data, set for release on Aug. 2, was expected to be the key ahead of the August monetary policy decision – that and the ANZ business confidence that will be out next Monday.

“An easing in tight labour market conditions and cooling annual wage inflation should provide the RBNZ reassurance that future inflation should settle in the 1-3% inflation target range,” Tuffley said.

“We’ve seen activity [ANZ business confidence] measures crawl out of the abyss, and cost/pricing measures come down slowly – albeit at a still-glacial pace for costs. Continued declines in costs and pricing intentions will be what the RBNZ will want to see after last week’s CPI.”

Use the comment section below to tell us how you felt about this.