March data shows uplift in sales and market engagement

The Real Estate Institute of New Zealand (REINZ) has released its March 2025 housing report, showing a notable rebound in market activity across the country.

Despite the seasonal shift into cooler months, buyer interest remains strong, supported by falling interest rates and relatively affordable property prices in many regions.

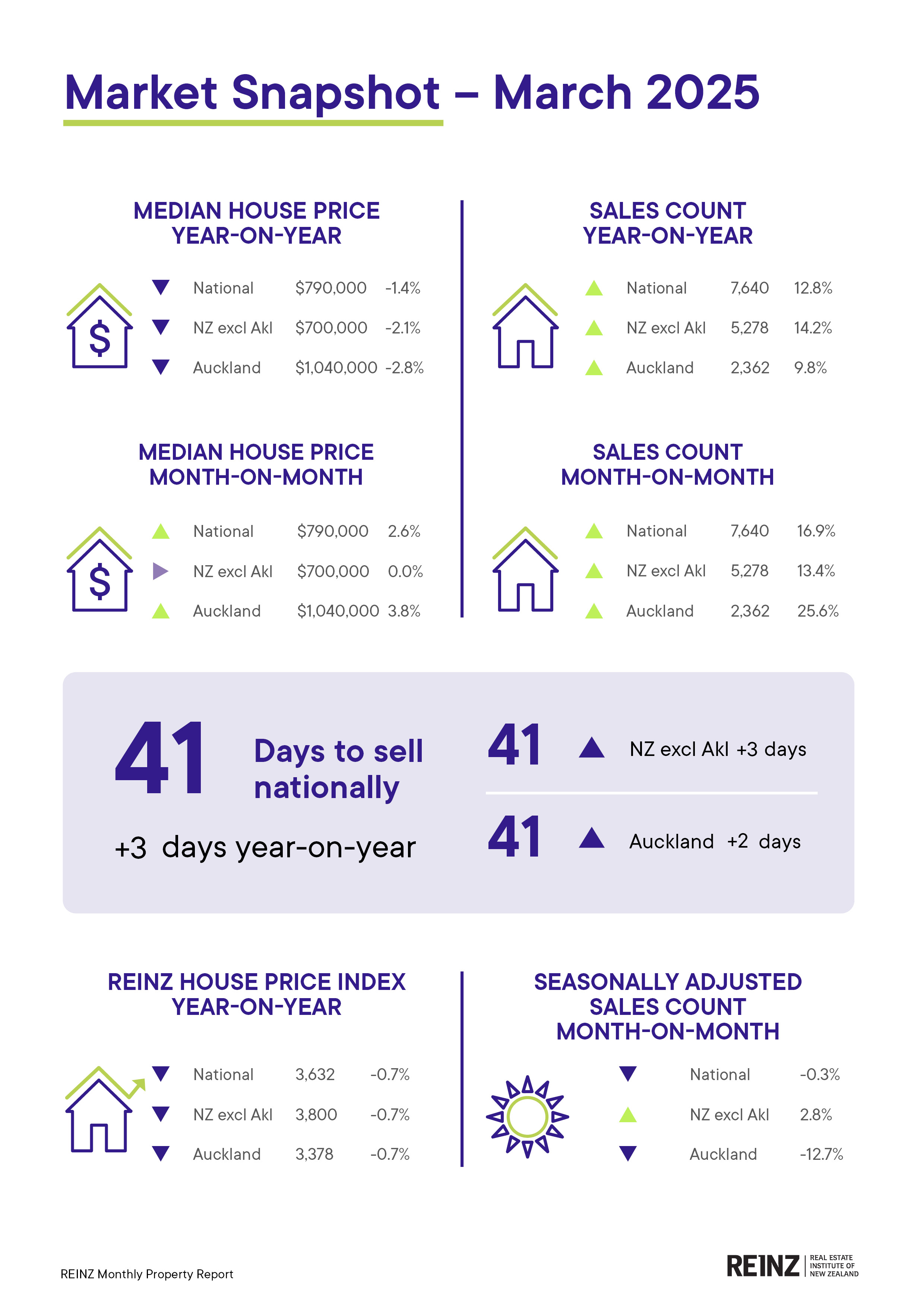

National sales volumes increased 12.8% year-on-year, with 7,640 properties sold compared to 6,774 in March 2024. Sales in New Zealand excluding Auckland rose even more sharply, by 14.2%, reaching 5,278 transactions.

“As we transition into the cooler months, the market remains vibrant rather than stagnant,” said Rowan Dixon (pictured), acting CEO of REINZ.

“There have been reports of increased attendance at open homes and auctions. Even in cases where properties don't sell at auction, there’s plenty of post-auction interest, indicating a resilient and engaged buyer community.”

Noteworthy sales growth was recorded in Tasman (+48.6%), West Coast (+23.6%), and Canterbury (+23.6%), with multiple regions achieving their highest March sales figures since 2021 or earlier, amidst falling mortgage rates, easing construction cost pressures, and stabilising home prices.

Home prices still sluggish, despite growing demand

While sales activity has surged, median property prices remain under pressure.

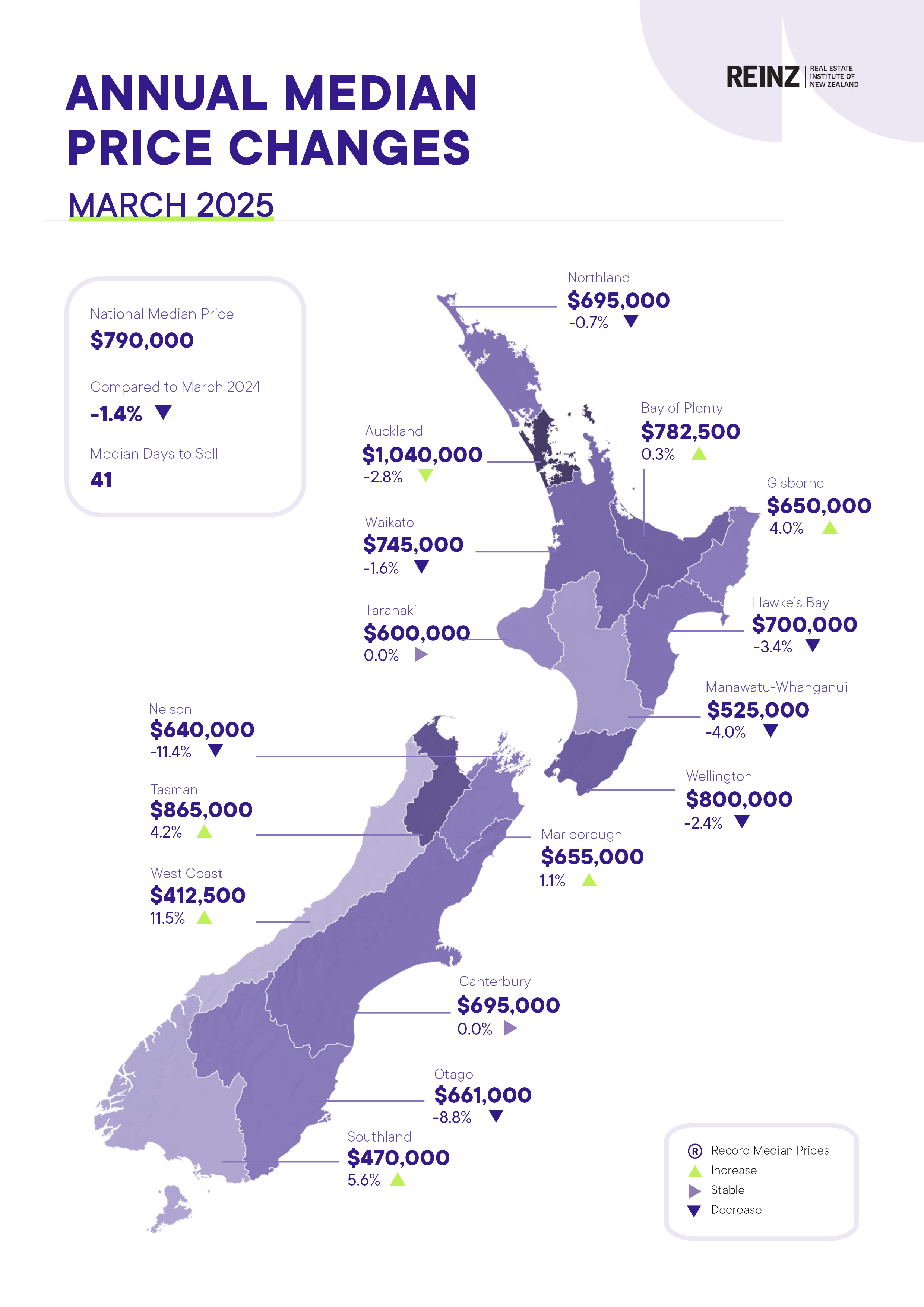

National median prices fell by 1.4% year-on-year to $1,040,000, while excluding Auckland, the median dropped by 2.1% to $700,000.

Only six of the 16 regions reported year-on-year increases in median prices. The West Coast led the growth with an 11.5% rise, followed by steady prices in Canterbury and Taranaki. However, Nelson saw a sharp 11.4% decline, falling from $722,000 to $640,000.

“March saw a year-on-year increase in sales, but median prices continue to lag behind,” Dixon said. “New Zealand’s property market remains the same: high listings result in decreased buyer urgency. If a buyer misses out on a property, they can easily find a similar one for sale.”

More homes available gives buyers breathing room

New listings rose 5.0% year-on-year to 12,029 properties across the country. Inventory also climbed 10.9% compared to March 2024, reaching 36,870 homes. Fourteen of 15 regions reported annual inventory increases, with Taranaki now posting 41 consecutive months of growth in supply.

Gisborne (+23.8%) and West Coast both saw notable jumps in new listings, continuing a trend of broader supply expansion that has contributed to longer selling times.

Auctions, selling time, and HPI show mixed results

Auction activity represented 15.8% of total sales in March, down slightly from 17.2% a year earlier. Meanwhile, median days to sell increased by 3 days, to 41 days nationally—a pattern mirrored in New Zealand excluding Auckland.

The House Price Index (HPI) declined 0.7% year-on-year to 3,632, and was down 0.6% from February 2025, indicating modest downward price pressure in the national market.

However, Southland held its position as the strongest-performing region for HPI movement—ranking first for the ninth consecutive month.

Outlook: Stability returns with hints of optimism

“As interest rates continue to fall and the OCR drops once again, local salespeople around the country are anticipating stability in the market over the coming months, bringing renewed energy and hope for many navigating these changing economic tides,” Dixon said.

With higher listings, a steady buyer base, and signs of confidence returning, the New Zealand property market appears to be entering a phase of recovery and realignment, even if prices remain subdued in the near term.

For detailed regional breakdowns, visit the full report on the REINZ website.