Australia warned against KiwiSaver-like housing policies

Since its introduction in 2010, the KiwiSaver HomeStart scheme in New Zealand has led to unintended consequences in the housing market.

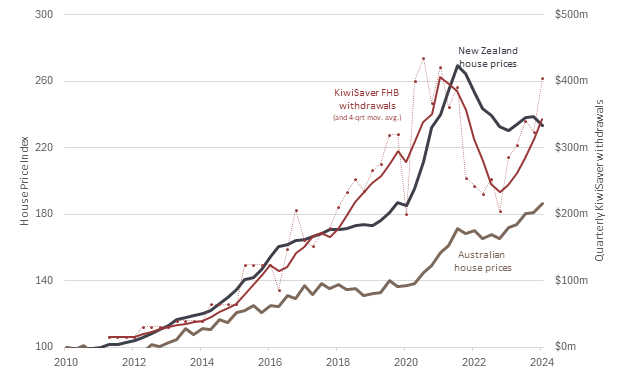

The Super Members Council’s detailed review showed that the initiative has coincided with a significant increase in house prices and a decline in homeownership, especially among younger demographics.

House prices in New Zealand escalated by 134% from June 2010 to June 2024, outpacing growth in the previous two decades and exceeding price increases in Australia by 1.5 times.

Homeownership rates have notably decreased, with a sharp decline of about 7% among individuals in their 30s.

Escalating mortgage debt for first-home buyers

First-home buyers have been particularly hard hit, finding themselves compelled to assume substantial debts to compete in the escalated market.

Since 2014, the incidence of first-home buyers taking out loans with an LVR of more than 80% has tripled.

“The proportion of high LVR loans taken out by first-home buyers has risen from 25% to 75%,” the council reported.

Financial strains and policy repercussions

Increasing financial burdens amid cost-of-living crisis

The spike in house prices necessitates that young New Zealanders tap into their KiwiSaver retirement savings to afford home purchases, transitioning from an option to a necessity.

According to the latest QV House Price Index, national residential property values rose modestly by 1.3% in the January quarter, with the average home price now at $913,567, down 1.3% from last year and 14.1% below the late 2021 peak.

The rate of first-home buyers using KiwiSaver funds increased from 65% in 2015-16 to 77% in 2023-24. This linkage suggests that withdrawals are a predictive indicator of market trends, with increases in withdrawals often leading to subsequent price hikes.

Warnings against similar Australian policies

Misha Schubert (pictured above), CEO of the Super Members Council, cautioned Australia against adopting a similar approach.

“If you want to see further rises in house prices and falling homeownership rates – New Zealand shows introducing a super-for-a-house policy leads in that direction,” Schubert said.

She advocated for alternative solutions, such as increasing housing supply, instead of enabling superannuation withdrawals for home deposits.

Expert economic perspectives on housing policies

The overwhelming consensus among Australia’s leading economists is that enabling super withdrawals for housing will exacerbate price increases and deepen mortgage and debt issues amidst a cost-of-living crisis.

Saul Eslake, an independent economist, analysed the effects of such policies in a report for the Super Members Council, concluding that they tend to make homes more expensive without increasing homeownership rates.

Long-term economic implications for retirement funds

The requirement to accommodate withdrawals has forced New Zealand retirement funds to maintain higher liquidity, consequently diminishing investment returns.

In comparison, Australian MySuper products have consistently outperformed KiwiSaver options, suggesting potential long-term detriments for Australians’ retirement savings if similar policies were implemented.

See the full media release on Mirage.News.