Mortgage adviser survey shows state of market

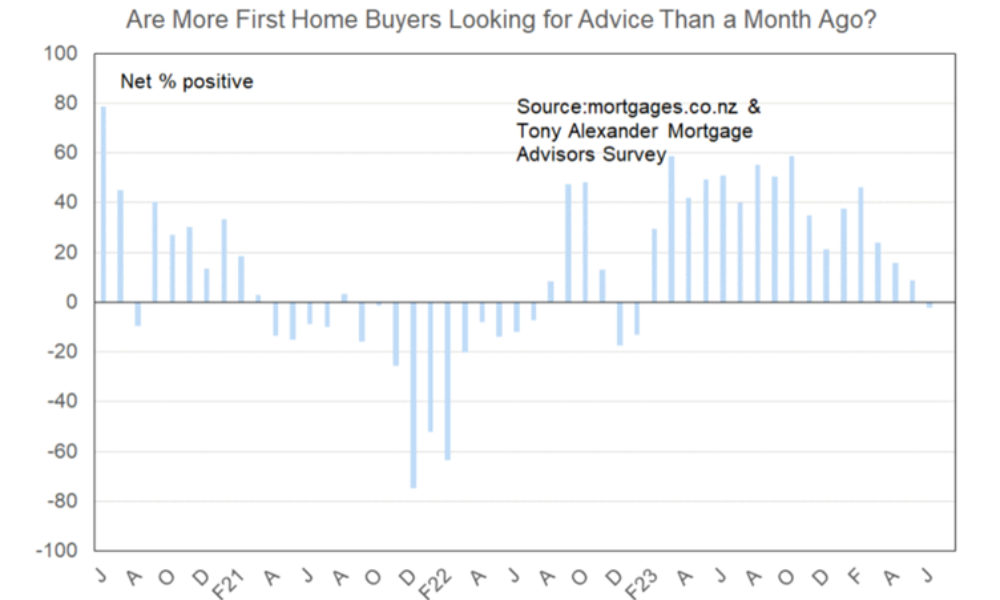

A net 2% of mortgage advisers have seen fewer first-home buyers in the market looking for advice, according to New Zealand economist Tony Alexander’s mortgage adviser survey, as the market slows down amid economic uncertainty.

This is the first negative result since January 2023 and is well down from the net 46% in February who said they were seeing more young buyers in the market, according to the survey which attracted 54 responses.

“Economic conditions in New Zealand have noticeably deteriorated since the earliest months of this year,” said Alexander (pictured above).

“In particular, worries about employment security have jumped higher and for many potential young house buyers this will be the first time they have seen a weakening of the labour market without any official moves to provide economic stimulus.”

Some anecdotal comments from advisers about first home buyers show some “slight improvements” in allowing boarder income to assist servicing and offering more cash contributions if the client is a first home buyer.

However, much of the respite ends there.

“Someone turned the tap off in AKL,” one adviser said. “Quietest I can remember in a long time. Lots of existing clients and referrals looking for refi to get cash from a new lender, but new enquiry for lending has really dropped away.”

“First-home buyers can get pre-approvals for finance to a certain level, but they are really scared when you let them know the amount of the repayments,” said another.

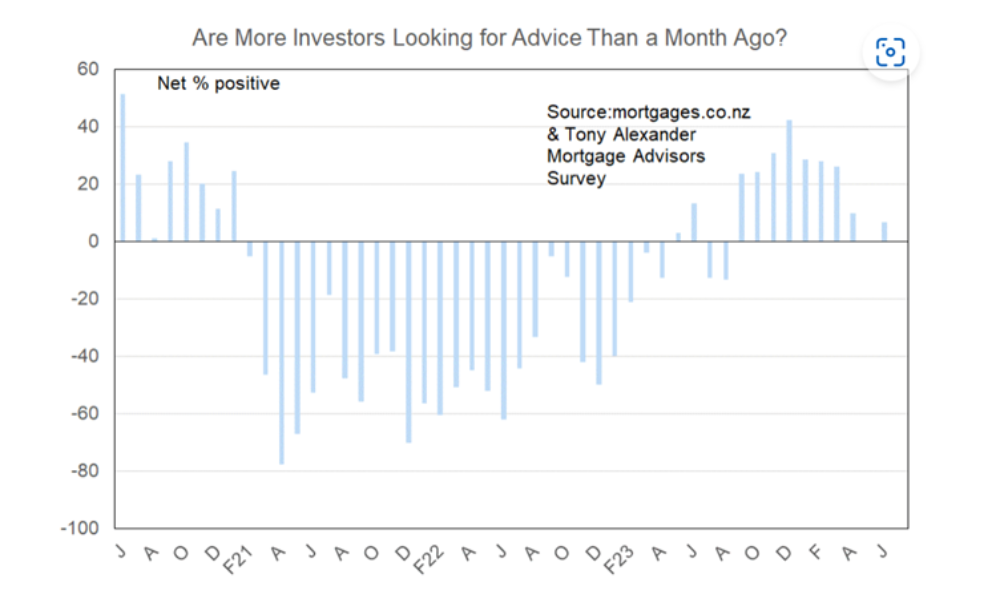

Investor activity slightly up

A net 7% of mortgage advisers had also noted that they are seeing more investors in the market looking for advice.

“It is not common for this measure to be stronger than that for first home buyers and a number of advisers noted that investors are showing increasing interest in purchasing now that the tax rules have changed,” Alexander said.

“But as our graph here shows, the rise in investor buying interest in the latter part of last year did not last long and it may be safest to say that since April there has been little net change in investor presence in the market as buyers.”

On the ground, advisers are starting to see changes with the rental haircuts with the reintroduction of interest deductibility, but banks are “very slow” to open the door much wider.

“Due to the upcoming easing of interest deductibility, the banks have reverted back to not differentiating when a house was purchased when shading during a rental income assessment,” Alexander said. “Now rental income is treated the same regardless of when purchased.”

Another adviser said the banks had altered their calculators to allow for tax deductibility of interest cost and were “less punitive” when allowing for rates and insurance costs associated.

Overall, a net 28% of mortgage advisers have this month said that banks are becoming more willing to lend money for a house purchase. This is unchanged from May’s result and consistent in fact with almost all other months since February 2023.

To fix or not to fix

There is a widespread view amongst economists and the general public that the next change in monetary policy will be an easing.

“Most expect this easing to come early next year and that is why borrowers are showing high preference for fixing their mortgage interest rate for just a 12-month period,” Alexander said.

“People wish to eventually take advantage of lower rates and feel that locking themselves into a long term now would deny them that chance.”

Some 81% of brokers say that buyers favour fixing for one year or less while 17% say they favour fixing from just over one year to two years.

Refinancing among homeowners

The survey also found there was an easing underway in the net proportion of brokers saying that more people are stepping forward and enquiring about refinancing their existing mortgage.

“As previously noted, it is difficult to figure out what this means for the general supply of properties coming to the market,” Alexander said. “But the rise in this measure earlier this year does correlate with a rise in fresh property listings at the same time.

“This suggests fresh listings may now be easing off and that is a result we can also see in my monthly survey of real estate agents.”