It's been 50 years since women could first apply for a solo mortgage – but has the sector gone far enough?

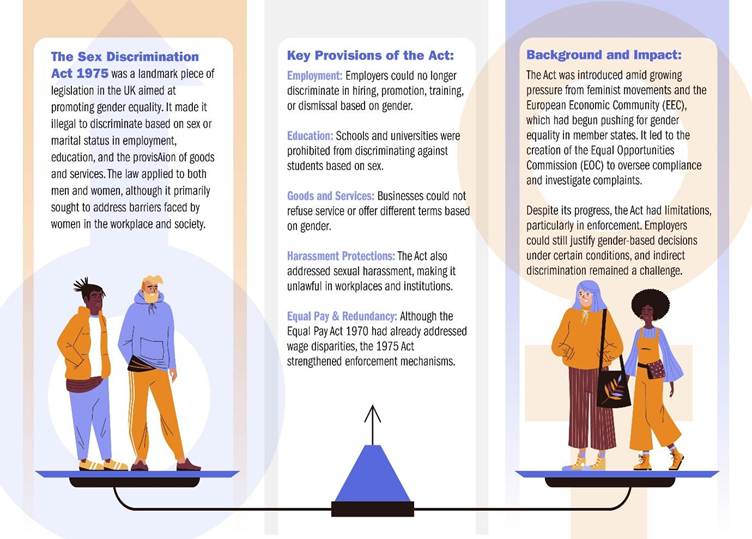

In 1975, a landmark bill passed by Harold Wilson’s cabinet made sweeping changes to the legal landscape of Britain – effectively ending centuries of misogyny, discrimination and unwarranted bias in workplaces, schools and, surprisingly, mortgage lenders.

It’s been 50 years since the Sex Discrimination Act of 1975 was made law, marking a shift in women’s rights in regards to finances. The act allowed women to open their own bank accounts and access mortgages on their own – banning bias around gender and marital status. And yet, despite the clear strides that have been made in the past five decades, the question being asked now is: have these changes gone far enough? Or are there still significant boundaries women have to navigate in mortgage land?

‘Women's income was seen as very erratic’

Speaking to Mortgage Introducer, Sam Lindsay (pictured left), founder and expert mortgage broker at My Mortgage Angel, said that the act was a real motivator for women to set out on their own without a father or husband – however, pay quality was and still is an issue in homeownership.

“[Back then], women's income was seen as very erratic. They couldn’t stop looking after children, and they weren't really paid very well either,” Lindsay said. “In the 80s, the pay gap started to narrow a little bit. And then in the 90s, we saw a lot more education [around money] – women were more aware of their finances and more confident to grab things on their own.”

According to recent data, the number of solo female mortgage applicants rose from 29% in 2017 to 33% in 2021. However, it’s important to note that there’s been a less than 3% rise in female mortgage holders across the last decade.

“Obviously, mortgage companies can’t use gender to affect the calculations on how much they’ll lend anymore, which is quite a big step forward,” Lindsay said. “Even issues like if clients are on maternity pay when their mortgage is being done – many lenders will look at their return-to-work plans and base it on there. They don’t require clients to actually be back at work to be able to take that mortgage.”

With mindsets and mortgages changing, the one barrier that persistently stands in the way of total gender equality is still prevalent – the pay gap. As of April 2024, the median gender pay gap for full-time employees was at 7%, a decrease from 7.5% in 2023. That gap is also more pronounced among older employees. In 2024, full-time employees aged 40 to 49 experienced a gender pay gap of 9.1%, while those aged 30 to 39 had a gap of 4.4%. However, over the last decade, the gender pay gap among full-time employees has decreased by approximately a quarter – but is that really enough?

‘The gender pay gap is still very real to this day’

“Although we’ve come a long, long way, [the gender pay gap] is still obviously there,” said Michelle Niziol (pictured centre), of Bespoke Property Investment. “Employers have to work at bridging that gap. [However], there’s more single female homeowners than there are male single homeowners at the moment – so that’s a huge positive in what we’re all fighting against here.”

For Sarah Tucker (pictured right), the main reason she set up a female-led brokerage was to address this challenge specifically. After having witnessed just how unfairly weighted the sector is against women, she took it upon herself to challenge the very male-dominated world.

“The gender pay gap is still very real to this day,” she said. “It also has this domino effect. If women are going to have maternity leave, for example. Although the rights are there for the man to be able to share that leave, most households need two thriving incomes to survive, especially with the cost of child care. [As such], the sensical thing to do is to pick the higher income to keep going and to keep that stability in a household. [All of] which means those historic gender pay gap concerns still exist in today’s world.

“Our role is to bring more women into the space, because we understand women can communicate with women in a very different way. And that’s not to say anything against men, but the way women receive information – as a general rule – is different. They like to have detail. They like to have timescales met. They like to have speed and efficiency. They’re more thorough and they really like to understand what’s happening.”

Looking back over the past 50 years, it’s thrilling to see just how far gender equality in the mortgage space has evolved – however more changes and innovations are on the horizon. New technologies such as generative AI and ChatGPT are shaking up how lenders operate and – oddly enough – dispelling unconscious bias at the same time.

“I think AI is going to take over a lot of the processing and underwriting,” Niziol said. “And I think that’s going to be a real positive thing – it’ll take out a lot of the gender bias that potentially goes on when cases are processed and underwritten, disadvantaging a female over a male applicant.”

Lindsay told Mortgage Introducer that the future will be dominated by a demand for new mortgage products that reflect changing demographics.

Financial education begins in the classroom

“We need to talk about first-time buyers potentially looking to buy later in life,” Lindsay said. “We certainly work with a lot of divorcees coming into property ownership a little bit later in life – [and there’s] not necessarily the right [sorts] of properties available. So we should be … looking at mortgage terms and products that are available [to them].”

The role of education, as always, remains of paramount importance in not only bridging the gender pay gap but also pushing forward more change in the mortgage industry as a whole. And this is something that Tucker believes should be happening in the classrooms and the playground.

“It’s really important that we start to educate on maths starting with our children,” she said. “And that has to extend to our parents and the women who are holding the children through these conversations. Mothers could be [turning to] to [their] child and saying: ‘Well, I don’t even [understand] this stuff – I wish I knew that.’ We have a duty to educate – educate on the knowledge that we hold, on our mortgage products, on what products are available to single parents … all of the mortgage challenges for women.”

And so, as we celebrate this 50-year milestone, the unified message is clear: continue to empower, educate, and innovate to ensure that women not only achieve but sustain financial independence.