Discover how Barclays for intermediaries supports mortgage brokers with its line of products and services. We’ll go over the application process, some online tools and calculators, and what brokers can expect from this banking giant

The lending sector in the UK, while very competitive, is rapidly evolving. Challenger banks are reshaping the industry, disrupting the market which has been long dominated by traditional lenders like Barclays, Santander UK, and HSBC.

Mortgage intermediaries play a critical role in navigating this changing industry. Their expertise is essential for securing the best mortgage deals and adapting to the evolving market conditions.

Here’s a detailed guide exploring Barclays’ products for intermediaries, the application process, as well as the digital tools, support, and training that intermediaries can make use of.

Products and services of Barclays for intermediaries

Barclays offers a wide range of benefits and products for intermediaries. One of these benefits is 1% commission on the total loan value for business loans or commercial mortgages. Certain conditions apply.

Barclays offers products designed to meet your clients’ needs, allowing aspiring property owners more ways to get on the property ladder. These products include:

- low deposit options

- fee-free products

- government schemes

Barclays offers products for the following types:

- first time buyer

- remortgage

- buy-to-let

- existing customer

- Purchase

Barclays works with thousands of brokers, including the top 10 intermediaries in the UK.

Latest rates for Barclays intermediaries

Here are some of the rates offered by Barclays for intermediaries to choose from, depending on the needs of their first-time clients.

|

4.46% Residential Premier Exclusive: 5 Year Fixed (Purchase Only)

|

||

|

Product Fee |

Annual percentage rate of charge (APRC) |

Loan to value (LTV) |

|

£699 |

7.1% APRC |

60% minimum loan £5,000; max loan £2m |

The initial rate is 4.46% until 30th June 2029, while the follow-on rate (variable for the remaining term) is 8.74%. Meanwhile, the early repayment charge is at 4% of the balance repaid until 30th June 2029.

|

4.47% 5 Year Fixed (Purchase Only)

|

||

|

Product Fee |

Annual percentage rate of charge (APRC) |

Loan to value (LTV) |

|

£899 |

7.1% APRC |

60% minimum loan £5,000; max loan £2m |

The follow-on-rate for and the early repayment charge for this product are the same as the first one. The only thing that’s different is the initial rate which is at 4.47% until 30th June 2029.

|

4.54% Residential Premier Exclusive: 3 Year Fixed (Purchase Only)

|

||

|

Product Fee |

Annual percentage rate of charge (APRC) |

Loan to value (LTV) |

|

£999 |

7.8% APRC |

60% minimum loan £5,000; max loan £2m |

The initial rate for this product is 4.54% until June 30th 2027 and the follow-on rate is 8.74% (variable for the remaining term). The early repayment charge is 3% of the balance repaid until 30th June 2027.

|

4.73% 5 Year Fixed (Purchase Only)

|

||

|

Product Fee |

Annual percentage rate of charge (APRC) |

Loan to value (LTV) |

|

£899 |

7.2% APRC |

75% minimum loan £5,000; max loan £2m |

The initial rate for this is 4.74% until 30th June 2029 with a follow-on rate of 8.74% (variable for the remaining term), while the early repayment charge is 4% of the balance repaid until 30th June 2029.

You can find a detailed listing of Barclays mortgage rates in our interest rates database, updated weekly.

Why work with Barclays as an intermediary?

Barclays provides four good reasons why you should register to be one of its intermediaries.

- Barclays puts you in control through the Intermediary Hub, resulting in valuable time saved for you and your customers

- Barclays has a dedicated service and support teams in the UK

- Barclays offers attractive rates with quick processing times

- Barclays offers tools designed to help you understand the borrowing needs of your clients

What’s the application process?

Step 1. Register

You have to register online and ensure that the following information are available:

- last 6 years’ residential history

- company name and financial services registration number

- head office address and contact details

- procuration fee and mortgage club scheme details

- company bank account details (if you want to be paid directly and not through a mortgage club)

- business email address

- if you’re a director, make sure to input ‘Sales Director’ or ‘Compliance Oversight’ into the Proc Fee text box on the Barclays Intermediaries Registration website.

Step 2. Confirm

After submitting your registration form, Barclays will send a confirmation email and provide instant access to its products and services.

Step 3. Access the Barclays Intermediary Hub

Finally, after everything is all set, you can log into the lender’s Intermediary Hub. It is a portal system that allows you, as an intermediary, to be in control. Through this tool, you can access real-time case updates, have a live chat, and make use of the ‘Knowledge’ help centre.

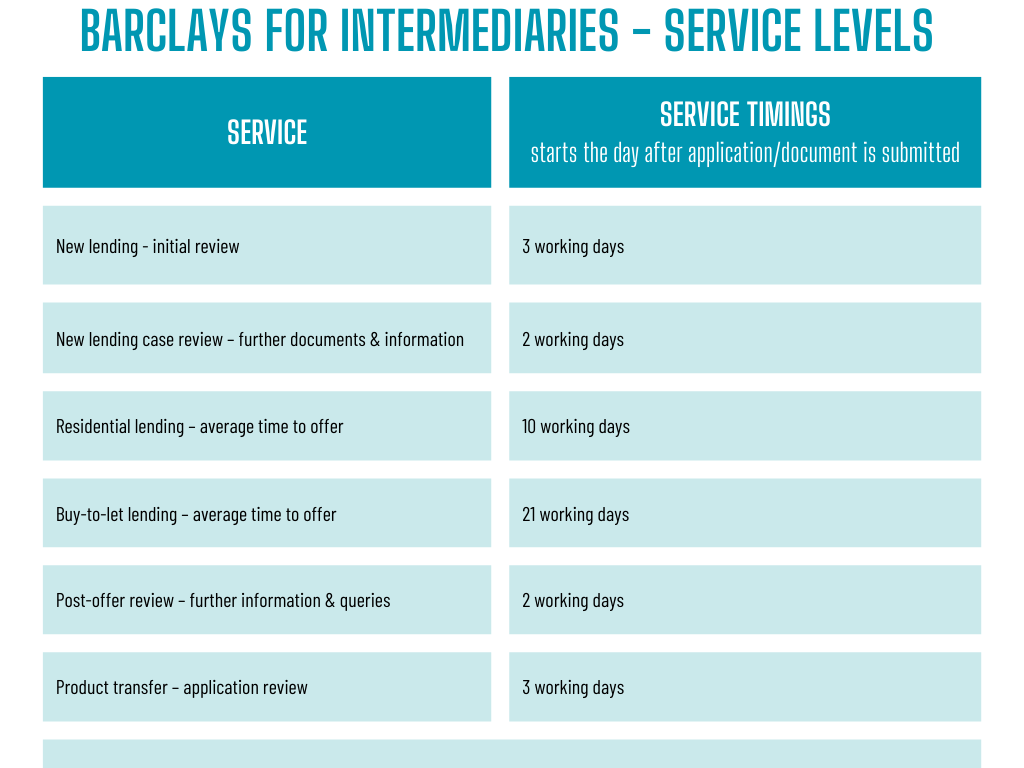

When can you expect to hear back from Barclays?

Here’s a listing of service level timings:

What digital tools and resources are available for intermediaries?

There’s a whole slew of tools for intermediaries carefully crafted to help you, your business, and most importantly, your clients.

Barclays Intermediary Hub

This portal provides real-time detail, information and progress updates concerning clients’ cases. It also features an online chat system for queries and questions, as well as the knowledge help centre, which contains all of Barclays’ help guides, tools, and collaterals.

Barclays calculators

Barclays provides calculators to enable intermediaries to know how much clients can afford to borrow. Barclays’ calculators let intermediaries know their clients’ residential and buy-to-let affordability. Here are some of Barclays’ calculators for intermediaries:

- residential affordability calculator – information needed for this includes the client’s mortgage requirements such as property value, product fee, and loan amount; applicant details like income; and commitments including credit card and overdraft balances

- buy-to-let affordability calculator – considers both personal and rental income in the assessment of the borrower, with the result depending on the accuracy and completeness of information entered

- offset mortgage calculator – helps clients see how their savings could reduce their mortgage term or monthly payments

Barclays guides

Barclays has a collection of simple guides, both in written and video formats, to help intermediaries work with their clients effectively.

The guides include documents showing:

- why clients should choose a Barclays new build mortgage

- how Barclays can support remortgage clients

- why a Family Spring mortgage may suit clients

- why choose Barclays for buy-to-let clients

- how to expedite the assessment process for portfolio landlords’ applications

- how to find the best remortgage deal for clients, and more

The video guides teach intermediaries on:

- how to register with Barclays

- how to use the intermediary hub

- how to submit an application

- how to edit intermediary hub details

- how to reset intermediary hub password

What are the updates and innovations in Barclays’ intermediary services?

Supporting the Mortgage Charter

Barclays has signed up to the UK government’s new Mortgage Charter to further help residential mortgage holders in the country.

Under the charter, a residential mortgage customer can apply to reduce their mortgage payments by either switching to an interest-only mortgage for six months or extending the mortgage term without a new affordability check. However, customers aren’t allowed to apply for both options on one mortgage account.

Read about the pros and cons of the Mortgage Charter.

Kensington Mortgages acquisition

Barclays completed the acquisition of Kensington Mortgages in March 2023, reinforcing the traditional lender’s commitment to the UK residential mortgage sector.

The acquisition made Barclays to be one of the few major banks that has a specialist mortgage offering.

Kensington is recognised in the mortgage sector for having a “market-leading data technology platform” to serve customers whose circumstances do not meet the lending criteria of high street banks.

The specialist lender, which is now part of the Barclays Mortgage Group, not only relies on credit scoring and algorithms to make decisions but looks at clients’ individual circumstances with an open mind.

Barclays Green Home Mortgages

Barclays launched the UK’s first green home mortgage in 2018. Green home mortgages offer lower rates for building energy-efficient homes. Customers under this new service buy an energy-efficient new build home directly from a builder or developer while getting a lower rate on fixed-rate mortgages.

Eligibility criteria for this service:

- the home must be a new build with an energy efficiency rating of 81 or higher

- the home must be in energy efficiency band A or B

- valid Energy Performance Certificate for fully built properties

- valid Predicted Energy Assessment certificate for properties still being built

New Build Mortgages

Barclays supports intermediaries’ clients in new build homes through its mortgage products for residential and buy-to-let products, valuations started on application submission, and six-month new build offer extensions.

Other features for clients under this service:

- up to 90% LTV ratio for houses

- up to 85% LTV for flats and maisonettes

- free valuations for properties with up to £2 million purchase prices

- specialist underwriters for high-value and complex income mortgage applications

Sustainability and social responsibility at Barclays

Part of Barclays’ strategy is to provide green and sustainable finance necessary to transform the economies it serves.

According to its website, Barclays, as a large global financial intermediary, plays an important role in helping channel investments into new green technologies and low-carbon infrastructure projects.

Visit our page on green mortgage rates for Barclays’ rates on eco-friendly homes.

Barclays for intermediaries and the property market

The UK mortgage market is undergoing significant changes. By leveraging Barclays’ range of tools and expert guidance, intermediaries can better navigate these changes and secure the best deals for their clients.

Barclays’ entry into green mortgage, its acquisition of Kensington Mortgages, and its support of the Mortgage Charter signify strong support for the property segment in the UK. And with the products and services offered by Barclays for intermediaries, brokers in the UK can expect nothing less.

What do you think of Barclays’ services for intermediaries? Let us know in the comments