Intermediaries in the UK do best with the right mortgage lender. One that is committed to topnotch service is Coventry for Intermediaries. Read on to know more

In every mortgage transaction, intermediaries play an important role by bridging the property buyer to the lender. As such, these intermediaries (or mortgage brokers) should partner with mortgage banks and companies that offer a broad range of products to suit their client’s needs.

Coventry for Intermediaries is a lending company that understands that every borrower is unique. They offer the usual mortgage products available in the United Kingdom, while also having a diverse selection for other client needs. This allows the Coventry for Intermediaries team to match borrowers with the most suitable mortgage program based on their financial circumstances and goals.

By building strong relationships with mortgage brokers, Coventry for Intermediaries facilitates better communication and support for new and seasoned intermediaries in the industry. This collaboration aims to help every aspiring homebuyer in the UK purchase their dream homes.

What is Coventry for Intermediaries?

Coventry for Intermediaries is the trading name of the Coventry Building Society, a financial institution that operates in the UK. They offer savings, mortgage lending, and other finance-related services.

The Coventry Building Society is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. They are also a member of the Building Societies Association.

What does Coventry for Intermediaries actually do?

The objective of Coventry for Intermediaries is to focus on working with professionals in the mortgage industry. This is exclusive for mortgage intermediaries or brokers and professional advisors working in the UK.

Coventry for Intermediaries also boasts excellent client service throughout the mortgage application process. To guarantee that these steps will be smooth and efficient, Coventry is eager to provide support and guidance to brokers through their website.

For property buyers seeking mortgage solutions through Coventry, consult a qualified mortgage intermediary or broker. Afterwards, they can assess your needs and guide you through the application process. Coventry works with the top mortgage intermediaries in the UK.

Other interested parties who would like to know more about Coventry’s mortgage products but are not intermediaries or professional advisors should visit coventrybuildingsociety.co.uk.

Products offered by Coventry for Intermediaries

Coventry for Intermediaries categorises their products to cater to new and existing clients. As for new clients, they have the following services:

- new home - for clients who want to move to a new property

- remortgage - for clients who want to change their mortgage lender

- first time buyer - for clients who want to buy their first property

For existing clients, here are the products offered by Coventry for Intermediaries:

- product transfers - for clients who want to switch to a new deal

- further advances - for clients who want to borrow more against their current property

- Green Further Advance – for clients to benefit from a lower rate when they borrow more for energy efficiency improvements

Check out the mortgage rates of Coventry Building Society for existing customers.

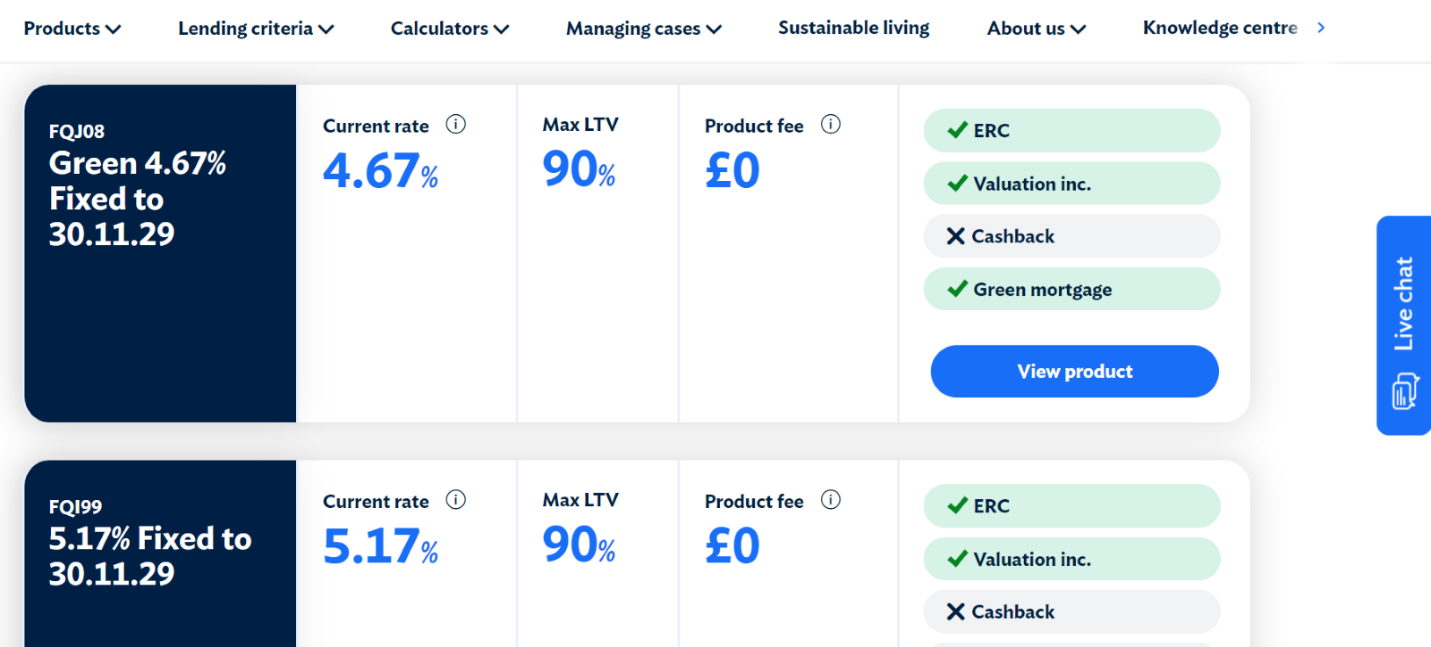

On Coventry for Intermediaries’ website, all mortgage products can be filtered according to:

- rate type - can be fixed or flexible

- repayment type - can be repayment or interest only

- product LTV - can range from 50% to 90% LTV

- product fee - can be with or without

- initial period - can be 2, 3, or 5 years

- features - can be valuation included, offset, green mortgages, or non-green mortgages

Here is what it looks like on the Coventry for Intermediaries’ website after using their product filter. It shows the products available under filtered values. You can also click on the “view product” button for more details on your chosen mortgage product:

Residential criteria

As you can expect with getting a mortgage, there are several different criteria that people must meet. Here is a list of all those criteria. If you want to learn more, look at the number next on the left and then go down to the corresponding number below:

- Age

- Address history

- Residency status

- Credit check

- Identification and verification - photos of physical documentation

1: Age

All applicants must be aged 18 or over, and they must be no more than 75 years old at the end of the mortgage term.

For applicants who cannot provide evidence of adequate pension income, the maximum age is their stated anticipated retirement age (70 years old and below). It can also be the applicant’s state retirement age if there is no anticipated retirement age provided.

2: Address history

All applicants must be living in the UK for three years. If an applicant is unable to provide a UK address history of three years, non-UK addresses should be recorded. Afterwards, the case will be reviewed on its own merits.

3: Residency status

All applicants must currently be residents in the UK and have permanent leave to remain. For foreign nationals except those from the Republic of Ireland, each applicant must be granted indefinite leave to remain or right of abode to live and work in the UK. If not, they can also have a settled or pre-settled status to live and work in the UK.

Coventry for Intermediaries will require any of the following documents as evidence:

- valid passport containing indefinite stamp

- home office letter with no expiration date

- residence permit showing indefinite leave to remain

- manual share code check showing settled or pre-settled status

Coventry for Intermediaries also requires evidence of two years' residency and employment history in the UK. All applicants must not hold any level of diplomatic immunity. If the applicant is unable to present any of these requirements, Coventry will decline the application.

4: Credit check

All applicants are credit searched before a mortgage is offered. This is usually completed at application in principle. Obtaining an application in principle will record a soft footprint against the applicant's credit records. It is when the full application is submitted that a hard footprint is left.

When completing a credit search on a mortgage broker’s client, Coventry for Intermediaries must leave a footprint. This highlights that they performed a search connected with mortgage lending when a full application is submitted, leaving a hard footprint.

Multiple credit searches over a short period can have a negative impact on the credit rating. Intermediaries should explain this to their clients before submitting their applications. Additional checks will also be carried out to verify the identity of the applicants.

5: Identification and verification

All applicants must submit the required documents listed under Coventry for Intermediaries’ website. All paperwork used for verification must be original or certified copies of documents originally printed at source and posted to the applicants. Copies printed from the internet are not acceptable.

If the applicant has examined the original document, they can certify the copy. If they did not examine the original document, copies of original documents can only be certified by one of the following:

- legal professional

- qualified accountant

- public sector official

- medical professional

- post office official

- embassy official

- local government councilor

- member of parliament

- bank manager

- building society manager

- minister of religion

Copies of original documents should be certified within the last 12 months using the following words: “I confirm that I have seen the original document.” The certifier must sign their name and include the following details:

- full name

- profession

- business address

- phone number

- date

The person certifying should be in current employment, but Coventry for Intermediaries will also accept certification from a person who has retired. They should not be related to the applicant in any way (e.g. spouse, partner, sibling, parent, child, or in-law). Finally, they should not be named as a joint account holder or borrower on the mortgage loan.

Coventry for Intermediaries will decline the applicant if they certify their own identification.

Photos of physical documentation

Coventry for Intermediaries also accepts photos of physical documentation for identification and verification purposes. These images can only be accepted by Coventry Building Society intermediaries and intermediaries admin.

Since Coventry does not accept JPEG files, the images should be in a PDF or TIF file format, with a maximum file size of 4MB. They must also be uploaded in one go on Coventry's document upload facility if the photo is longer than one page.

Another option is to send it in a separate email using their secure email service. Photos scanned from CamScanner are also accepted.

Remortgaging criteria

For those who want to apply for remortgage, Coventry for Intermediaries requires the applicants to be residents in the property on the date of application.

Acceptable capital raising purposes

Coventry for Intermediaries accepts the following loan purposes which are subject to loan amount and LTV limits:

- to consolidate debt

- to purchase additional land

- to purchase the equity of another party to the mortgage

- to improve, repair or maintain residential properties that are owner-occupied

- to extend the leasehold title of the property in mortgage to Coventry for Intermediaries

Loan purposes

Coventry for Intermediaries will consider applications for the following loan purposes if the application meets all their lending criteria:

- to buy additional land

- to buy the equity of another party to the mortgage

- to raise capital, including debt consolidation, subject to restricted purposes

- to improve, repair or maintain residential properties that are owner-occupied

- to raise capital on mortgage-free residential properties that are or will be owner-occupied

- to buy the freehold title of a leasehold property which is already in mortgage to Coventry for Intermediaries

- to buy residential properties for owner-occupation, including properties purchased under the Right to Buy scheme

- to remortgage residential properties for owner-occupation, including properties originally purchased under the Right to Buy scheme

Coventry for Intermediaries will not accept applications for these loan purposes:

- to pay taxes

- to invest in business

- to share ownership application

- to use the loan for bridging finance

- to replenish savings and investments in timeshares

- to apply for a loan that does not benefit all parties on the mortgage

- to buy properties where vacant possession would not be achieved upon completion

- to share equity applications, including the Homebuy scheme and the Key Worker scheme

Partnering with Coventry for Intermediaries

Having a wide choice of mortgage loan options tailored to different client profiles, Coventry for Intermediaries is a good partner for mortgage professionals who want to up their game.

Their online portal can be leveraged by mortgage brokers and financial advisors for easier tracking of their applications. Coventry for Intermediaries’ tools and resources will boost mortgage professionals into giving topnotch service for their clients.

As with any mortgage bank or lender, it is important for intermediaries to stay updated on the changes made regarding the products, criteria, and guidelines of Coventry for Intermediaries. This will open many opportunities to enhance skills and gain more experience.

Above all, partnering with Coventry for Intermediaries can help elevate you in a better position of succeeding in the mortgage industry. If you don’t feel that they’re the right fit, please see our overviews of other UK lenders’ intermediaries services:

Natwest for intermediaries

Barclays for intermediaries

HSBC for intermediaries

Halifax for intermediaries

Santander for intermediaries

Nationwide for intermediaries

Accord for intermediaries

Would you like to work with Coventry for Intermediaries? Why or why not? Share your insights in the comments below.