It is beneficial for intermediaries in the UK to work with lenders that offer competitive home loans. Learn more about Kent Reliance for intermediaries in this guide

The mortgage industry in the United Kingdom is dominated by large banks and the usual lending companies such as HSBC, Barclays, Nationwide, and others. These lenders are widely known by many due to their top-notch services for both intermediaries and their clients.

Another leading player among these lending institutions is Kent Reliance. The boast of being the go-to mortgage lender for complicated residential and Buy to Let cases. Their property loan offerings are competitive and flexible. They are also known for accepting clients that are typically rejected due to their complex situations.

Do you feel like this might be the mortgage lender your clients are looking for? In this article, Mortgage Introducer gives an overview of Kent Reliance for intermediaries. We’ll go over their background as well as their flagship mortgage products. You can check if your clients are eligible for their property loan offerings as we will also shed light on their eligibility criteria.

Get to know Kent Reliance for intermediaries

Kent Reliance for intermediaries is the exclusive intermediary arm of Kent Reliance, a private banking company based in Kent, England. They have been in operation since the 1840s. Kent Reliance offers these award-winning services to clients across the UK:

- fixed rate bonds

- tax-free cash ISAs

- regular savings accounts

Kent Reliance is the trading name of OneSavings Bank plc or better known as the OSB Group. The OSB Group is a specialist lender and savings provider. They focus on underserved sub-sectors of the mortgage market.

Do you wish to succeed in the mortgage industry like the top intermediaries in the UK? Working with a reliable mortgage lender like Kent Reliance will help propel you to greater heights in your career.

Products and services offered by Kent Reliance for intermediaries

Kent Reliance is bent on helping intermediaries with clients who have complicated cases. With their market knowledge and flexible terms, they can provide tailored solutions where other lenders might struggle. These two are their flagship mortgage products:

- buy to let mortgages

- residential mortgages

Both property loan options have additional services like product transfer and further advances.

Let’s discuss both mortgage products at length:

1. Buy to let mortgages

Buy to let mortgages are best suited for property landlords who want to expand their property portfolios. Kent Reliance for intermediaries is eager to accept different cases for your clients.

Whether they are first-time landlords or those with large portfolios, your clients can get the most out of Kent Reliance’s buy to let mortgage. Some of its highlights include:

- no maximum loan amount

- £75,000 minimum property value

- affordable rates that can be as low as 4.79%

- competitive loan-to-value (LTV) ratio of up to 80%

- houses of multiple occupancy (HMOs) up to 20 beds and multi-unit freehold blocks (MUFBs) up to 10 units accepted

- more fee options alongside lower mortgage rates to help with affordability

We’ve reduced our buy to let rates across all products!

— KRFI Mortgages (@KRFI_Mortgages) August 9, 2024

With rates now from 4.09% as part of our limited editions range, paired with our flexible criteria, there are plenty of options to support your landlord clients🤝

FOR INTERMEDIARIES ONLY. pic.twitter.com/KmrtywtKU4

Our mortgage rates database should be part of every intermediary’s tool kit. It shows what the top ten mortgage providers’ loan offerings are plus how they compare against each other. This database is updated weekly, so intermediaries can have the most updated rates to share with their clients. Feel free to bookmark this page and come back weekly to check for any updates!

2. Residential mortgages

For intermediaries whose applicants want to secure a mortgage for residential purposes, Kent Reliance has four ranges of mortgage options:

- core range

- extra flexibility range

- shared ownership range

- income flexibility range

Let’s explore the different perks that each mortgage range has:

Core range

This option has fixed plus percentage fee options. It has no maximum loan amount and can be up to 90% LTV. The minimum property value required is £75,000.

Extra flexibility range

The maximum loan for the extra flexibility range is £1,500,000 while the minimum property value is £75,000. It also has affordable rates that can be as low as 6.14%.

Shared ownership range

You apply for up to 100 share value and still have flexible underwriting. This range’s minimum property value is £125,000. Part-own and part-rent mortgage applications are also accepted. The only downside: this option is only available in England and Wales.

Income flexibility range

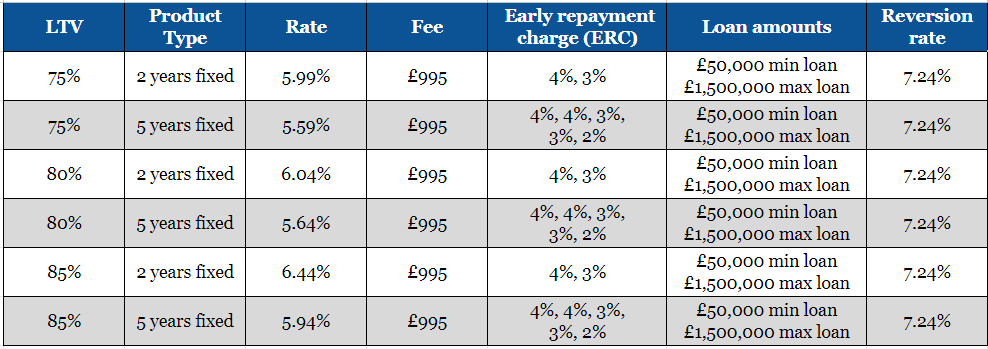

The minimum loan requirement for income flexibility range is £50,000 while the maximum is £1,500,000. This option is available for purchase and remortgage, including day one remortgages.

Check out this comparative table of Kent Reliance for intermediaries’ income flexibility mortgage range for clients who are residential mortgage applicants:

Aside from their flagship property loan offerings, Kent Reliance for intermediaries can also provide assistance through:

- large loan mortgages

- lending into retirement

- shared ownership mortgages

- landlords who want to apply for MUFBs and HMOs

- options for self-employed and contractors

- limited company and special purpose vehicle (SPV) mortgages

Kent Reliance for intermediaries’ eligibility criteria

The buy to let and residential mortgages have varying criteria for applicants. It is beneficial for mortgage brokers to know the requirements set by Kent Reliance for intermediaries regarding these two home loan choices. First, let us explore the criteria for the buy to let option:

Requirements for buy to let mortgage applicants

For buy to let mortgages, the minimum age limit of applicants must be 18 years old. On the other hand, the maximum age limit at the end of the mortgage term must be 85 years old.

Types of landlords accepted

Kent Reliance for intermediaries accepts mortgage applications from the following landlord clients:

-

personal ownership landlords: Kent Reliance for intermediaries also accepts consumer buy to let applications for personal ownership landlords. There is no requirement for experienced landlords to have their own residential property.

-

first-time landlords: For intermediaries with clients who are first-time landlords, Kent Reliance accepts HMO applications for properties with up to six lettable rooms. They also require a minimum of 20% deposit for property loans to help aspiring landlords buy their first HMO.

-

limited company landlords: Kent Reliance accepts intercompany loans from intermediaries with clients who are limited company landlords. They also accept shareholder deposits and director loans as deposits.

-

portfolio landlords: For portfolio landlords, Kent Reliance does not set limits on the size or value of existing portfolios held with other lenders. There is also no limit on the number or value of properties mortgaged.

-

HMO and MUFB landlords: Kent Reliance considers applicants for HMOs and MUFBs with up to 20 lettable rooms or units. Applications with multiple flats or houses on a single freehold can also be accepted. Investment valuations can be instructed on certain five and six bed HMOs.

Deposit requirement

Kent Reliance for intermediaries accepts intercompany loans as a source of deposit. However, the loan term must not exceed that of the mortgage. The majority shareholder needs to be reflected in the SPV and the connected company. As for the connected company, it should not have any charge or interest in Kent Reliance’s security.

The intercompany loan is required to have its terms written in a loan contract. A copy of the agreement will be held on file. For the calculation of the loan, the rate of interest applied should be HM Revenue and Customs (HMRC)’s ordinary rate of interest. Any monthly payment will be included in the interest cover ratio (ICR) calculation.

Unacceptable property attachments

Kent Reliance will not accept mortgage applications for properties above or attached to the following establishments:

- takeaways, restaurants, and cafes

- bars and nightclubs

- MOT garages or any property where industrial processes are carried out

- dry cleaners

- nail bars

- tattoo parlours

- hairdressers

For further clarification, Kent Reliance's business development managers can assist intermediaries in navigating these issues.

Costs for application

Here are some of the fees required for buy to let applicants:

- application fee of £145

- product switching fee of £30

- other product fees

Requirements for residential mortgage applicants

The minimum and maximum age limits for residential mortgages are the same as buy to let mortgages.

Income requirements

Kent Reliance for intermediaries will accept the following forms of income:

- 50% for overtime, bonus, commission

- 100% for gross annual basic income

- 100% for pension, whether state or private

- 100% for child or working family tax credits

- 100% for child maintenance by court order; child can be up to 13 years old

These benefits are not acceptable as income:

- housing benefit

- jobseeker’s allowance

- mobility allowance

Rental income

Kent Reliance for intermediaries will accept 100% of net rental income and 50% if used as additional income by the applicant. However, it must be supported by evidence through these documents:

- finalised accounts

- SA302s tax calculations

- accountant’s reference for tax calculations

Second income

If the applicant can prove that they can maintain an additional source of revenue, Kent Reliance for intermediaries will accept 100% of the second income. This extra income should also be held for at least 12 months. As for the hours worked, they should be sustainable and not excessive.

Loan purposes

There are only two loan purposes accepted by Kent Reliance for intermediaries:

- purchase of applicant’s main residence

- remortgage of applicant’s main residence

Here are some examples of unacceptable loan purposes:

- to repay tax obligations

- to shore up a business

- remortgages to repay gambling debts

- purchases where the applicant is married or in a civil partnership and their spouse or partner is not included on the application

Costs for application

Residential mortgage applicants are required to pay the same application fees as buy to let applicants.

Does Kent Reliance for intermediaries have remortgaging options?

Intermediaries with clients who want to remortgage can apply for this service with Kent Reliance. This allows applicants to apply for a new mortgage with more competitive interest rates. Remortgaging is one of the many Kent Reliance products under their New Business Mortgage category.

To know more about remortgaging with this lender, watch this a video from Kent Reliance on the process and fee assisted remortgages:

Becoming an intermediary partner for Kent Reliance

Now that you know what Kent Reliance for intermediaries can offer, you might want to decide whether becoming their intermediary partner is good for your career. Of course, this decision will benefit not just your current clients but also your prospects. Establishing a partnership with good mortgage lenders is a pro tip that topnotch intermediaries apply to succeed in this profession.

If you want to see other mortgage companies with exclusive intermediary platforms, we have several guides that might interest you. Here are some of our overviews on lenders that are intermediary-centric and are equipped with competitive mortgage products for your clients’ benefit:

- Your guide to Accord for intermediaries

- Your guide to Aldermore for intermediaries

- Your guide to Barclays for intermediaries

- Your guide to Coventry for intermediaries

- Your guide to HSBC for intermediaries

- Your guide to Leeds for intermediaries

- Your guide to Nationwide for intermediaries

- Your guide to NatWest for intermediaries

Do you think that Kent Reliance for intermediaries is the right lender for your clients? Why or why not? Tell us what you think in the comments section below.