Everything is in place for house prices to just keep rising

Following the global financial crisis of 2007-09, house prices worldwide dropped by 6% in real terms according to a recent report in The Economist. However, this decline was temporary as prices quickly recovered and surpassed pre-crisis levels. When the COVID-19 pandemic hit, economists predicted a housing crash, but instead, the market boomed, with homebuyers—often masked—competing fiercely for properties.

Then, starting in 2021, as central banks raised interest rates to combat inflation, concerns arose about a significant housing market collapse. Yet, real house prices only fell by 5.6% and have since begun to rise again. The resilience of the housing market, driven by various factors, suggests that house prices will continue their upward trend in the coming years, regardless of economic challenges.

There is certainly plenty of pent-up demand in the market – August saw a 23% increase in property sales agreed over the same period last year according to Rightmove as a result of the slight easing of the interest rate cork in the real estate demand bottle. And Zoopla figures released today support those numbers.

So – what has made house prices continue to rise?

Historically, housing was considered a stable asset class, with prices in developed economies remaining largely flat in real terms until about 1950. Builders would construct homes to meet demand, keeping prices stable. The expansion of transportation infrastructure in the 19th and early 20th centuries also helped to moderate housing costs by allowing people to live further from their workplaces, preventing too much pressure on the inner cities.

However, post-World War II developments dramatically changed these dynamics. Governments began subsidizing mortgages, urbanisation intensified, and a baby boom led to increased demand for homes. Housing construction peaked in the 1960s but has since slowed – and now a shortage of available properties is causing prices to rise steadily across much of the developed world.

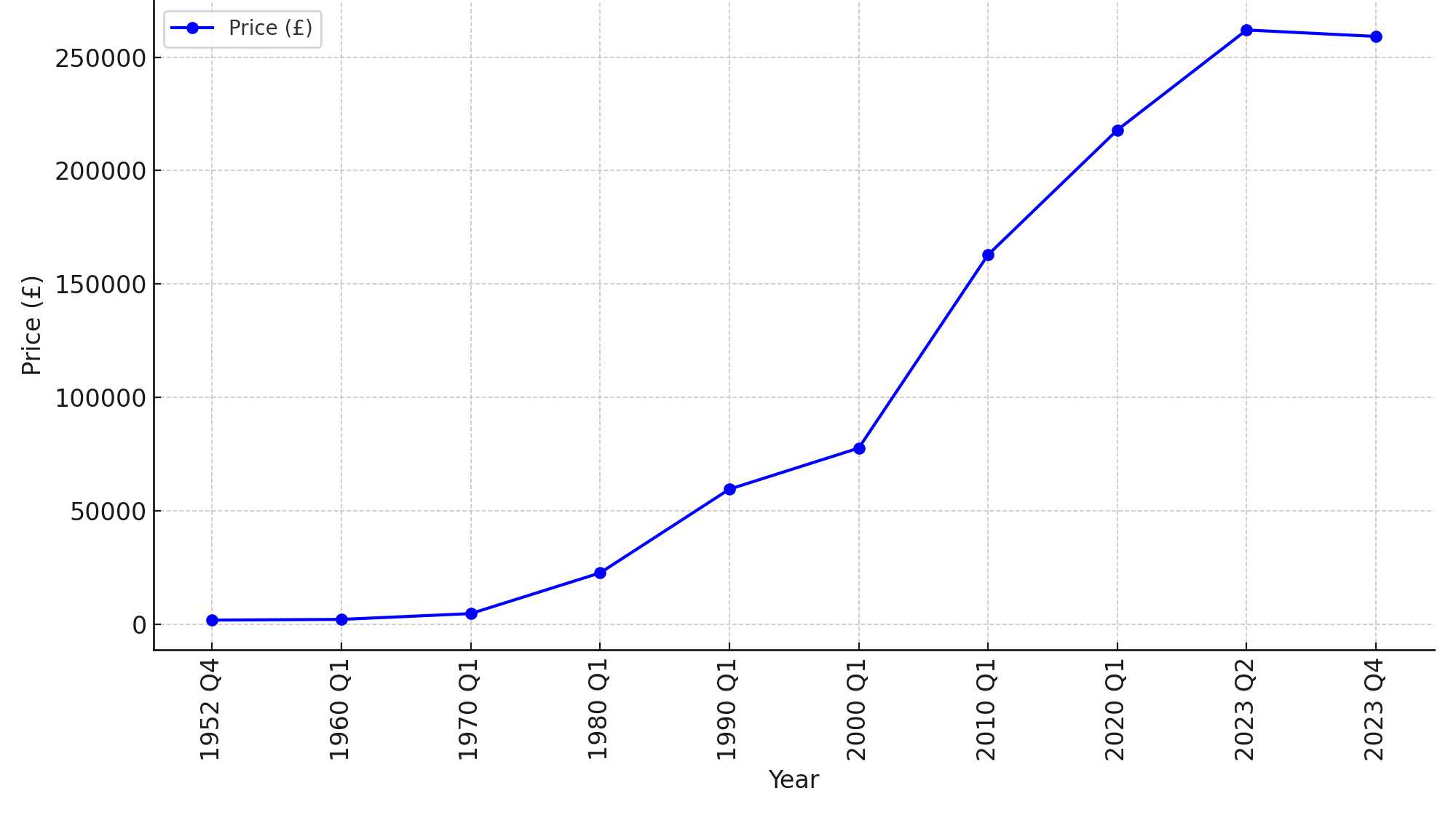

Figures: Nationwide BS

Interest Rates as a Key Driver of House Prices

One of the most significant contributors to rising house prices over the past 40 years has been the steady decline in real interest rates. According to research from the Bank of England, house prices in the UK have nearly quadrupled in real terms since the 1980s, largely due to the sharp drop in the real risk-free interest rate.

As real interest rates fell, borrowing costs decreased, making housing more affordable and driving up demand. This trend has not been limited to the UK—many developed countries have experienced similar dynamics, with falling interest rates encouraging borrowing and fuelling house price growth.

Crucially, this decline in interest rates has often been unexpected, further driving up house prices as markets adjusted to new borrowing conditions. Homebuyers who secured low fixed-rate mortgages have been shielded from rising interest rates, allowing house prices to continue climbing, even in the face of broader economic uncertainties.

And why aren’t rents rising as fast as house prices?

Despite rising house prices, rental yields have been declining, particularly since the mid-1990s. This divergence between house prices and rental yields does not indicate a housing bubble but instead reflects the reduced "user cost" of owning a home, as explained in a recent Bank of England’s working paper. The user cost accounts for factors such as interest rates, maintenance, taxes, and anticipated capital gains.

As interest rates have fallen, the user cost has decreased, allowing house prices to rise without a corresponding increase in rents, leading to lower rental yields. However, this trend remains consistent with broader economic fundamentals, rather than signalling unsustainable price growth.

Urban Demand and Immigration

When the pandemic hit , a wave of city dwellers headed out to the countryside, but cities remain key drivers of housing demand, despite the rise of remote work. Large urban centres have retained their appeal, with a substantial portion of businesses in the U.K. still located in major cities. Employment in capital cities across the developed world has increased, further intensifying competition for housing in dense urban areas.

Immigration is another crucial factor driving housing demand. The foreign-born population in developed countries is growing at an unprecedented rate of 4% annually. Research from Barcelona University found that a 1% increase in immigration rates can lead to a 3.3% rise in house prices. Despite efforts in countries like Canada and Germany to curb immigration, the continued need to support aging populations means wealthy nations are likely to see continued demand for housing from immigrants, contributing to upward pressure on prices.

Long-Term Sensitivity to Interest Rates

One of the most important takeaways from the Bank of England research is the long-term sensitivity of house prices to changes in interest rates. The study contends that a 1% increase in medium-term gilt rates could lead to a nearly 20% drop in house prices – but it . This finding underscores the significant role that monetary policy plays in shaping housing markets. While demographic trends and urbanization will continue to support housing demand, changes in interest rates remain a critical factor that can alter long-term price trajectories.

Countries like the U.S. have seen housing prices hit new record highs, with a 5% nominal increase in the past year alone. In Portugal, prices are also soaring, and even markets that struggled in the past, such as Rome, are now experiencing recoveries. The global decline in real interest rates has been a key factor driving these trends, as lower borrowing costs have made homeownership more accessible.

The Interplay of Interest Rates and Housing Prices

The continued rise in housing prices can be largely explained by the prolonged decline in real interest rates. As borrowing costs have fallen, more people have been able to enter the housing market, driving up demand and pushing prices higher. While short-term fluctuations in economic growth, interest rates, and banking crises may cause temporary volatility, the long-term drivers—demographics, urbanisation, and most importantly, low interest rates—are likely to ensure that house prices continue to rise.

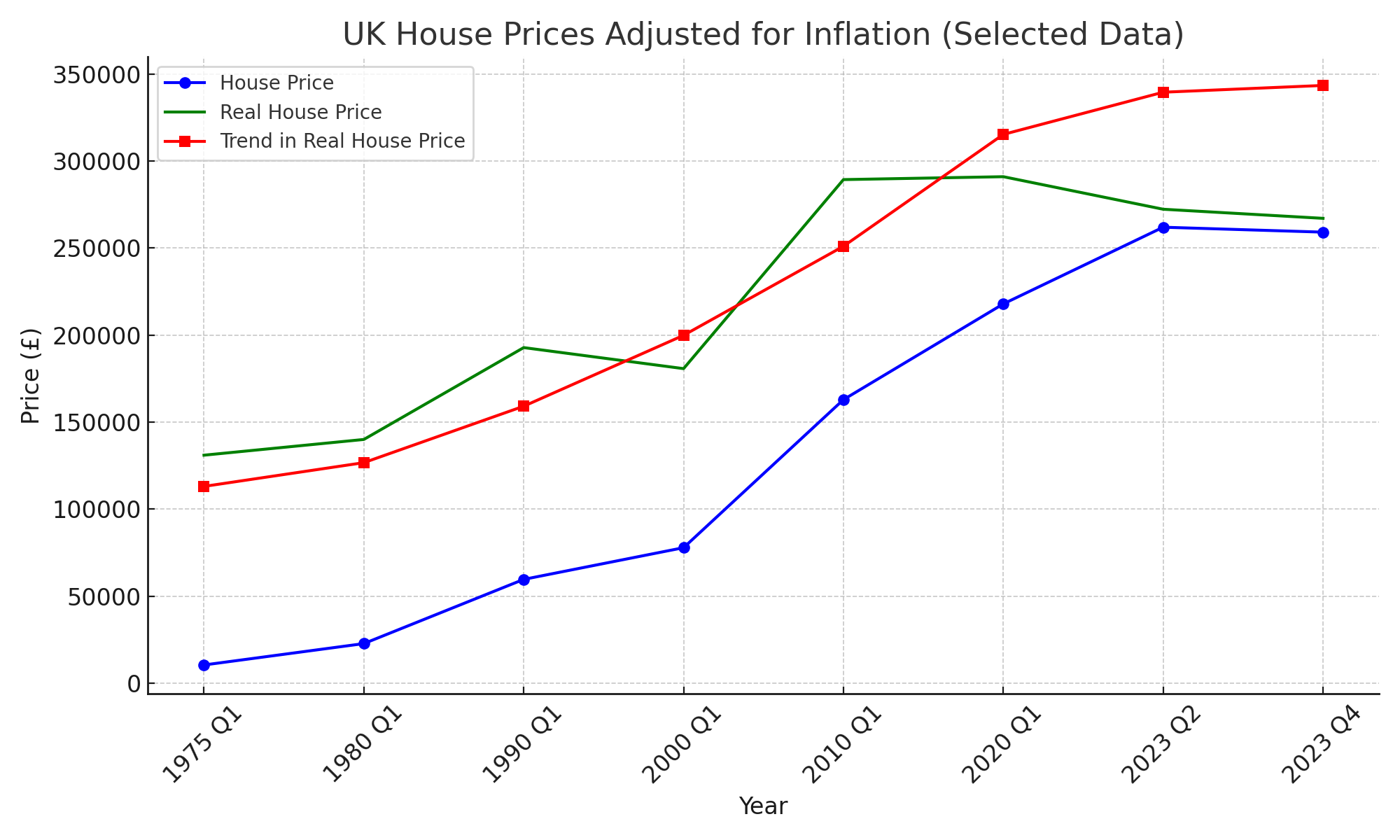

How much have houses gone up in real value?

Nationwide’s excellent housing figures show an interesting story when we look at what houses cost adjusted for inflation:

Figures: Nationwide BS