Fixed rates continue gradual decline

The availability of low-deposit mortgage deals in the UK has reached levels not seen since 2008, according to the latest data from the Moneyfacts UK Mortgage Trends Treasury Report.

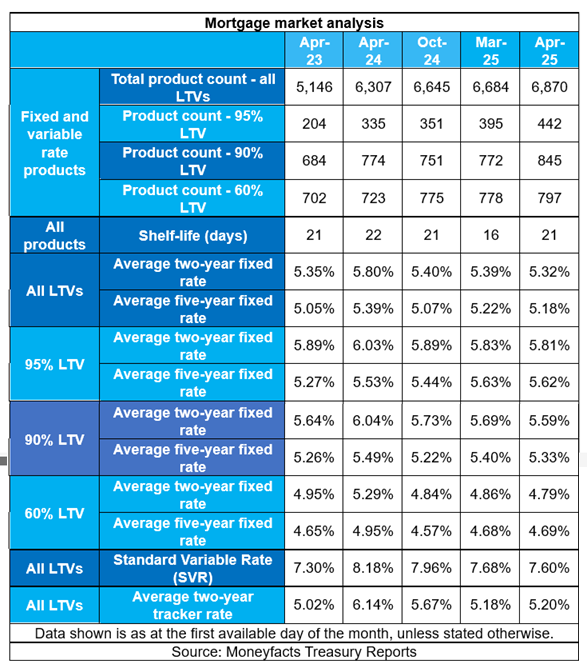

As of this month, the number of products available at 95% loan-to-value (LTV) increased to 442, while those at 90% LTV climbed to 845 – both marking their highest levels in 17 years. Overall mortgage product choice also expanded, rising to 6,870 options – the most since October 2007.

Average fixed mortgage rates continued to fall, though at a slower pace than in recent months. The typical two-year fixed rate dropped by 0.07 percentage points to 5.32%, while the five-year fixed dipped 0.04 points to 5.18%. These decreases follow more significant cuts in March, when two- and five-year rates fell by 0.13 and 0.10 points, respectively.

Since early April, the five-year fixed rate has declined by 0.21 percentage points, while the two-year equivalent has dropped by 0.48 points. The spread between the two now stands at 0.14%, the narrowest since October 2022, when rate inversion began.

Meanwhile, the average two-year tracker variable rate edged up to 5.20%, and the standard variable rate (SVR) fell to 7.60%, down from a peak of 8.19% in late 2023.

The average mortgage product shelf life has increased to 21 days from 16 in the previous month. According to Moneyfacts, this reflects a period of limited movement in swap rates and stability in the Bank of England base rate, which held steady in March. The next rate decision is due in May.

“The flourishing choice of low deposit mortgages will no doubt be welcomed by borrowers who are either looking to remortgage or are a first-time buyer,” said Rachel Springall (pictured), finance expert at Moneyfacts. “However, there is still much more room for improvement, particularly as the choice of deals at 95% loan-to-value represents just 6% of all deals available.”

Springall also pointed to the recent end of Stamp Duty Land Tax relief as a possible factor encouraging lenders to offer more products. She added that even in a steady base rate environment, lenders may adjust rates in response to movements in the swap rate market.

“Fixed mortgage rates are down year-on-year, and slowly the market is seeing the average two-year fixed getting closer to its five-year counterparts,” she said. “These moves make it essential for borrowers not to delay finding a new deal… it’s vital borrowers seek advice to find the most appropriate package for them, and not just be swayed by the initial rate.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.