What’s the outlook for next year?

The UK housing market displayed unexpected resilience in 2024 despite affordability pressures, according to the head economist of the world’s largest building society.

Robert Gardner (pictured), chief economist at Nationwide, noted that at the beginning of 2024, potential buyers faced significant hurdles, including high house prices relative to earnings and surging rental costs. He added that first-time buyers struggled to save for deposits, with the private rental sector’s record-breaking rent increases compounding the challenge.

Even for those with sufficient deposits, higher borrowing costs stretched affordability, Gardner pointed out.

“A typical mortgage rate for someone with a 25% deposit hovered around 4.5% for much of the year, three times the 1.5% prevailing in late 2021 before the Bank of England started to raise bank rate,” he said.

Despite these challenges, housing market activity picked up as the year progressed.

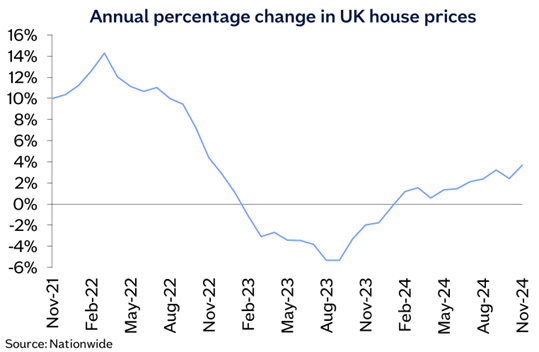

“The number of mortgages approved for house purchase each month rose above pre-pandemic levels towards the end of the year,” Gardner noted. “Similarly, after starting the year registering small annual declines, the pace of house growth moved firmly into positive territory, approaching 4% in November.”

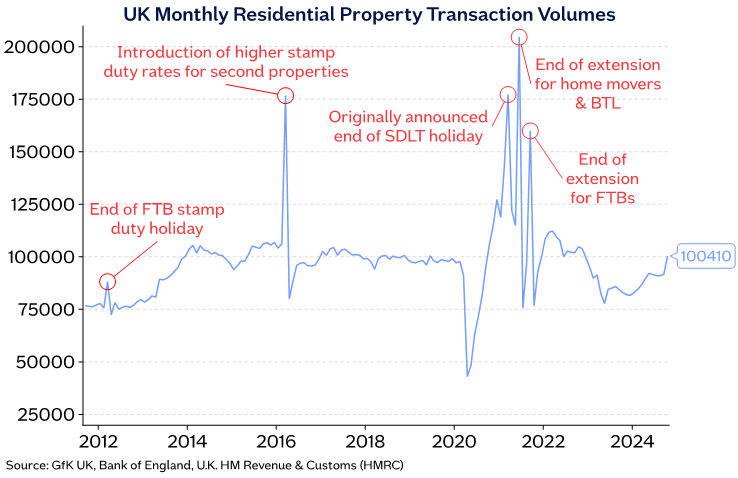

Gardner warned of potential volatility in 2025 due to upcoming changes to stamp duty. Buyers are expected to bring forward purchases to avoid the additional tax, leading to a spike in transactions during the first quarter, particularly in March, followed by a slowdown in the following months. Similar patterns occurred after previous stamp duty adjustments, making it harder to assess the market’s underlying strength.

Looking ahead, Gardner anticipates gradual improvements in affordability as interest rates ease slightly and earnings outpace house price growth.

“Providing the economy continues to recover steadily, as we expect, the underlying pace of housing market activity is likely to continue to strengthen gradually as affordability constraints ease through a combination of modestly lower interest rates and earnings outpacing house price growth, where the latter is likely to remain broadly in the 2% to 4% range in 2025,” he concluded.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.