Higher tax burden shifts BTL focus to Northern England

The increase in the stamp duty land tax (SDLT) surcharge on second homes from 3% to 5%, announced in Labour’s recent Budget, has had limited impact on landlord activity so far, according to residential estate agent Hamptons.

Analysis of sales agreed in November reveals that 10.7% of transactions across Great Britain involved landlords, slightly above the 2024 average of 10.2%.

While landlord activity remains far below its 2015 peak of 15.7%, the proportion of buy-to-let buyers is broadly consistent with pre-pandemic levels. In 2019 and 2020, landlords accounted for 10.8% and 10.9% of purchases, respectively.

The data suggests landlords have remained largely committed to purchases initiated before the tax rise, with only 28% of deals renegotiated or remarketed in the months leading up to the change. This figure is significantly lower than the 2022 mini budget aftermath, when 56% of landlord sales were adjusted amid soaring mortgage rates.

The surcharge hike means investors now face significantly higher costs. For example, on a £300,000 property, an investor pays £17,500 in SDLT compared to £2,500 for a home mover and nothing for a first-time buyer. From April 2025, investor and mover costs will increase by an additional £2,500.

Northern England becomes a buy-to-let stronghold

The increased tax burden is expected to push more investors toward Northern England, where lower property prices result in smaller SDLT bills. In the North East, 18.4% of November sales were to landlords, slightly above pre-surcharge levels from 2015. There, the average buy-to-let purchase price was £115,000, with SDLT rising from £3,450 to £5,750 under the new rules.

In contrast, landlord purchases in southern regions, particularly outside London, have fallen significantly, where high property prices and surging SDLT bills make buy-to-let investments less viable.

The average SDLT bill on a £500,000 property now stands at £37,500 for investors, rising to £40,000 in April 2025. Landlords in the South are increasingly purchasing properties in the North to take advantage of lower SDLT bills, higher rental yields, and faster house price growth. Gross rental yields in the North East averaged 9.7% in 2024, far exceeding London’s 5.7%.

SDLT revenue projections

The UK government has previously outperformed its revenue targets from the 3% SDLT surcharge introduced in 2016, which has consistently raised between £1.4 billion and £2.7 billion annually — up to three times the original estimate. Officials now project the 5% surcharge will generate an additional £400 million annually, with only a modest decline in investor activity expected.

In Scotland, where the surcharge increased from 6% to 8% in December 2024, revenue from second-home buyers and investors accounted for 31% of total stamp duty receipts from January to October. However, landlord purchases in Scotland have dropped sharply, with investors accounting for just 5.8% of transactions so far this year, compared to 10.3% in 2016.

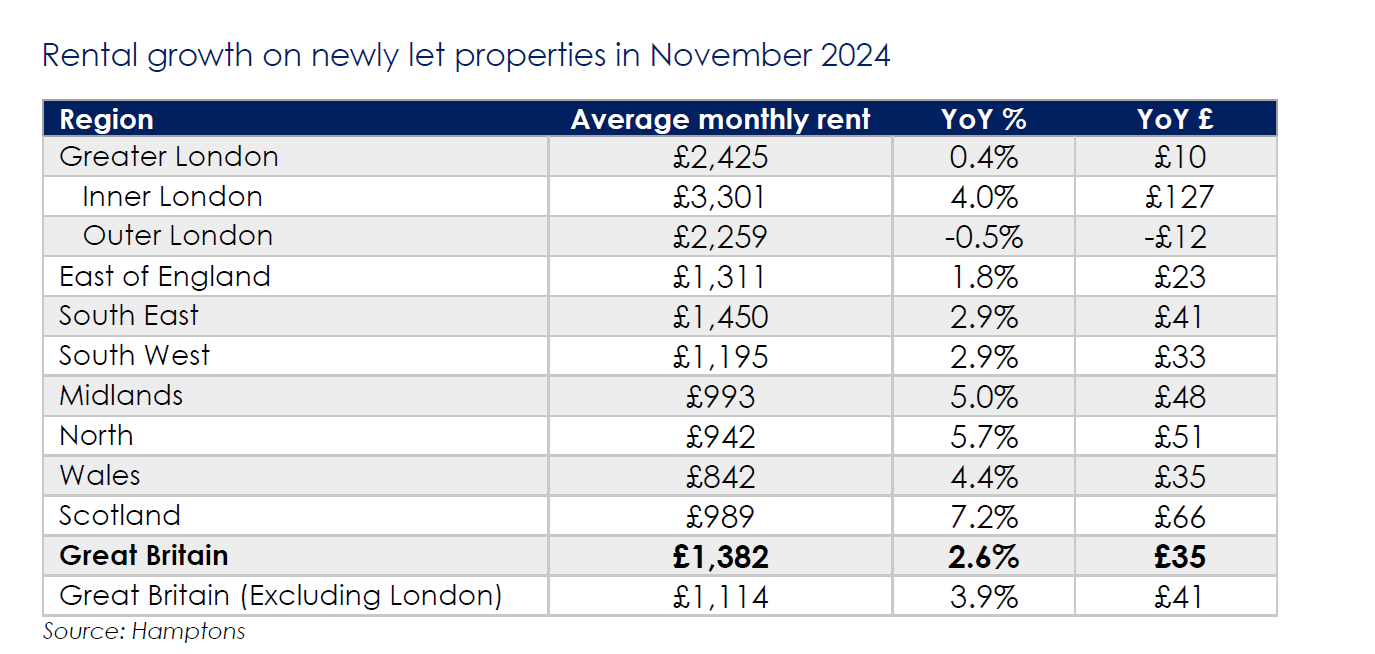

Rental growth slows to four-year low

Rental growth across Great Britain has slowed markedly, with average rents on newly let properties rising by just 2.6% in the 12 months to November — the slowest pace since 2020. However, rents have surged by 31.6% since November 2020, outpacing wage growth during the same period.

The strongest rental growth in the past year occurred in Scotland (7.2%) and Northern England (5.7%), while London saw a modest 0.4% increase. Southern England experienced annual rental growth ranging from 1.8% to 2.9%.

Rental stock levels have risen, helping to ease upward pressure on rents. In November, there were 13% more homes available to rent than a year earlier, though stock remains 10% below pre-pandemic levels in 2019.

“While the number of buy-to-let purchases by landlords remains muted compared to historic levels, their numbers have not collapsed,” said Aneisha Beveridge (pictured), head of research at Hamptons. “Purchases are concentrated in the Midlands and Northern England, which are becoming buy-to-let heartlands where the surcharge bites slightly less hard.”

Beveridge noted that falling interest rates could improve buy-to-let returns in 2025, particularly in regions offering high yields.

“While political headwinds haven’t gone away, these risks and added costs are increasingly being priced into buy-to-let returns in the form of higher yields,” she added.

On the rental market, Beveridge observed that slower growth in newly let rents reflects a return to pre-pandemic conditions.

“However, tenants renewing contracts continue to see increases well above these levels, though the pace will likely slow as rents align with market rates,” she said.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.