"We don't want to get to a point where the directive has kicked in and we have to tell clients"

Gindy Mathoon’s work at Create Finance isn’t just about brokering deals; it’s about solving some of the most intricate puzzles in the UK mortgage market. His biggest challenge right now? It’s not rising rates – it’s evolving regulations.

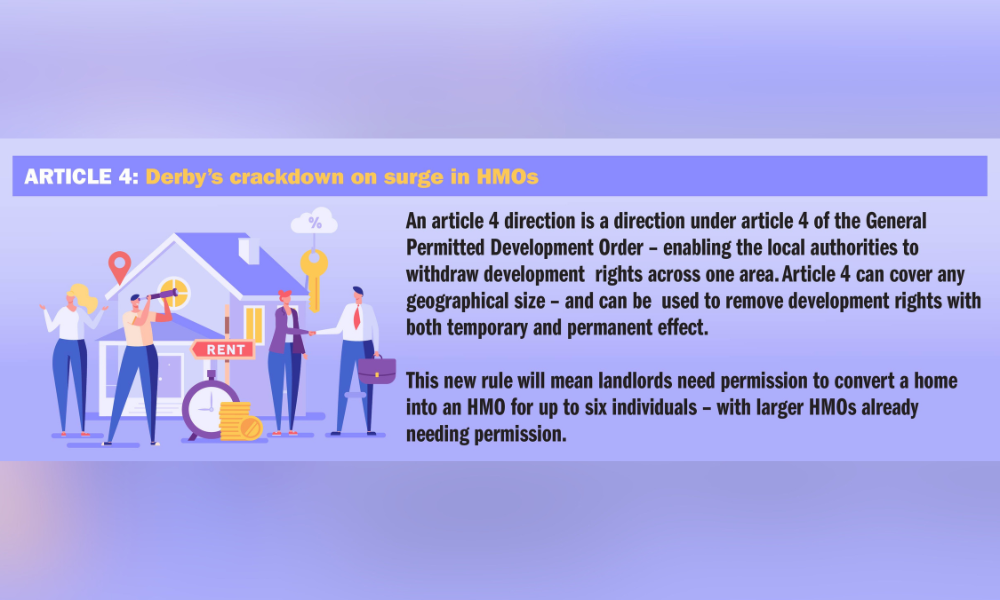

Speaking to Mortgage Introducer, Mathoon (pictured) said that, in particular, the imminent impact of Derby’s Article 4 directive is a prime example. This regulation, set to take effect in May 2025, requires planning permission for converting properties into six-bedroom HMOs (Houses of Multiple Occupancy). The directive has sparked a “race against time” as investors, particularly those from London, scramble to finalise their projects before the rule change.

“Derby is a very HMO-centric area,” Mathoon explained. “It’s a hotspot for London investors, and a lot of lenders have been pulling out during application processes, citing the impossibility of completing the work before the directive kicks in.”

“Derby is a very HMO-centric area,” Mathoon explained. “It’s a hotspot for London investors, and a lot of lenders have been pulling out during application processes, citing the impossibility of completing the work before the directive kicks in.”

Rather than accept these setbacks, Mathoon and his team work closely with lenders to establish clear commitments upfront.

“We’re speaking to lenders to say, ‘Are you likely to pull out now that this is coming in?’ If the answer is ‘no’, we move forward quickly,” he told Mortgage Introducer. “There's quite a lot of deals in at the moment. We don't want to get to a point where the directive has kicked in and we have to tell clients they’re too late and they need to apply for planning permission now. We've got a duty of care to make sure we're doing enough possible now to ensure that the clients have got the funding they need and that they've got their work done as well.”

Beyond Article 4, Create Finance specialises in aiding clients often overlooked by high-street banks, such as those with poor credit or unconventional employment situations. Products like 95% loan-to-value (LTV) mortgages have proven invaluable for first-time buyers with limited deposits.

“There’s still a lack of credit options for these clients,” Mathoon explained. “That can have a derogatory effect on their credit score on any credit file. As such, we're seeing the 95% deals are still being very, very popular because it caters to a market of small deposit. However, there's a few lenders there that will consider you even if you've got a bit of poor credit as well – whether that's a low credit score or a small default as such. Is there enough lenders lending at 95% LTV? ‘No’ is the answer.”

And this is reflective of the first-time buyer market in general, with Mathoon noticing a shift in the aspirations of younger buyers. Gone are the days when buyers would start small, gradually climbing the property ladder. Today’s borrowers aim straight for detached homes with gardens, pushing their borrowing capacity to the limit.

“The borrowers we’re seeing now stretch as much as possible, even going up to six times their salary,” he told Mortgage Introducer. “They don’t want to live in the terraced property at all, they want a detached property with a garden. Something has changed over the last few years whereby they want to maximise their borrowing – as such, lenders that allow high income multiple mortgages seems to be very, very popular.”

Despite a strong interest, the market isn’t without significant challenges. Stagnant wage growth and rising house prices have created a challenging landscape for many, with many buyers still waiting to see what inflation rates will look like in 2025. Investors however, as Mathoon told Mortgage Introducer, remain undeterred. And, despite stamp duty increases, Mathoon reports steady interest in buy-to-let properties.

“Investors view property as a long-term game,” he added. “Even with higher upfront costs, they’re factoring these into their strategies and looking at long-term gains.”