BTL could be finished by poor decisions and the government could shoot itself in the foot with a £3.6 billion loss says new report

In just over two weeks, Rachel Reeves will announce how she plans to raise funds for the new Labour government, without driving up interest rates or bringing the economy to a standstill. News has already leaked that payroll tax may well be in the crosshairs, with Jonathan Reynolds, Secretary of State for Business and Trade fuelling the discussion in interviews – and it’s widely believed that Capital Gains Tax is another target for her.

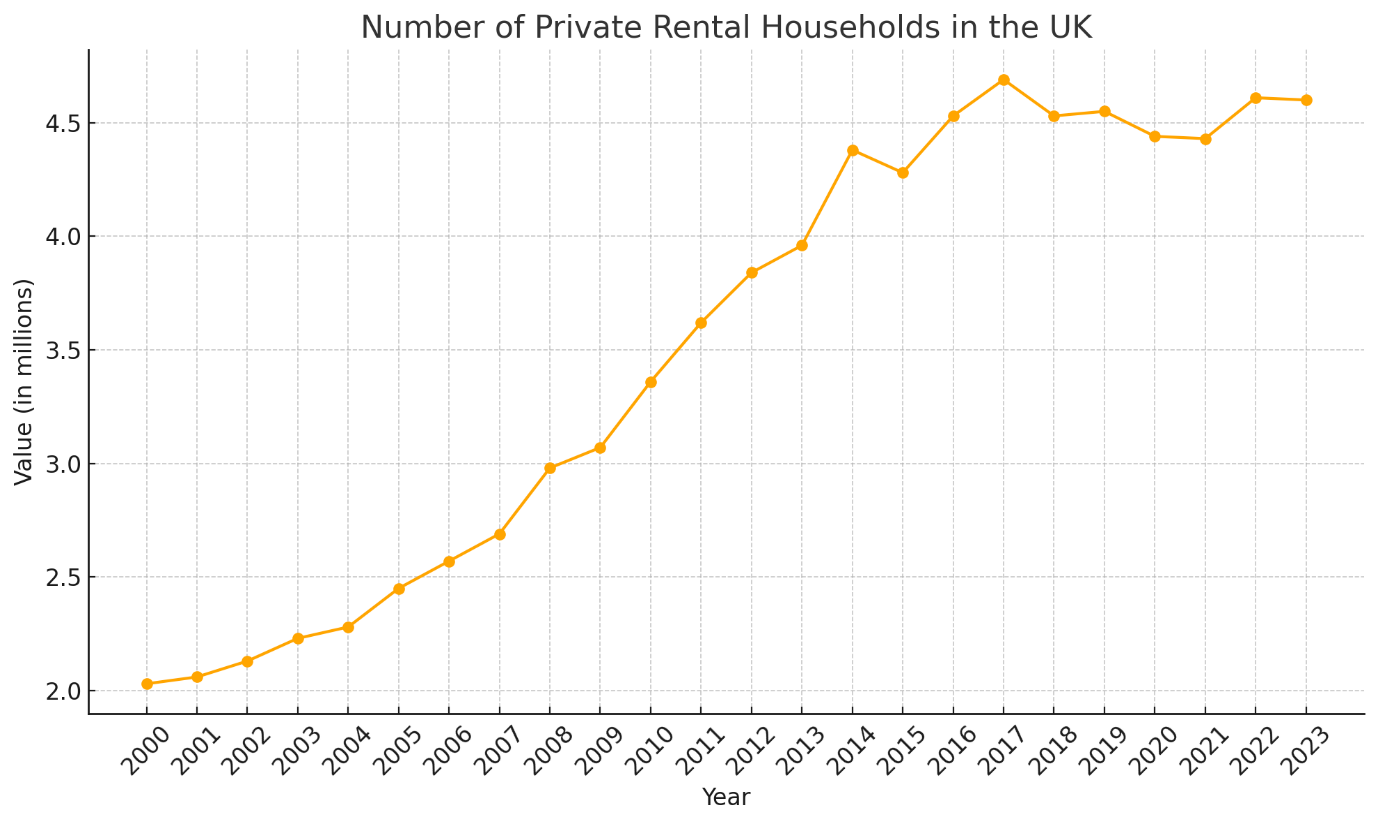

And a potential exodus of landlords could soon follow and drastically reduce the availability of rental properties if the rumoured Labour capital gains tax (CGT) reforms and other regulatory changes go ahead. Economic consultancy Capital Economics predicts that if Rachel Reeves raises CGT to align with income tax rates, nearly a million rental properties could vanish from the market over the next decade – leaving renters stranded.

The worrying forecast comes amid growing concerns within the buy-to-let sector about Labour’s broader housing reforms, including the proposed abolition of Section 21 ‘no fault’ evictions and energy efficiency standards that will require rented homes to achieve an Energy Performance Certificate (EPC) rating of ‘C’ by 2030. These measures, coupled with the looming possibility of CGT hikes, are leading many landlords to reconsider their involvement in the market.

Watch: Experts discuss buy-to-let market outlook

Capital Economics estimates that if CGT rises to 40-45% - up from the current 28% - landlords could sell off 790,000 properties and significantly reduce new purchases. The consultancy believes this would result in a shortfall of 910,000 rental homes over the next decade. It also calculates that the move would be stupid mathematically. While the tax hike might initially boost government revenues by £16.2 billion, the Treasury could suffer a £26.1 billion loss in income tax as landlords exit the market, leaving a £3.6 billion net deficit.

This projected decline in rental stock adds to concerns already raised by landlords over the proposed abolition of Section 21. A survey conducted by buy-to-let lender Landbay found that over 75% of landlords fear losing control over their properties if no-fault evictions are banned. Landlords argue that Section 21 is crucial for managing their investments and dealing with problematic tenants.

Figures from the Department for Levelling Up, Housing and Communities

One survey respondent described the proposed changes as a “catastrophe” for landlords, removing their ability to regain control of properties after a fixed-term tenancy ends. This concern has been echoed by the National Residential Landlords Association (NRLA), which has warned that a flood of eviction cases could overwhelm an already strained court system. Without improvements to the possession claim process, landlords worry they will struggle to regain their properties when needed, further disincentivizing investment in the rental market.

Read: Borrowing costs rise as Reeves budget fears spread

In addition to legal reforms, Labour’s energy efficiency targets are also weighing heavily on landlords. Ed Miliband, Labour’s Energy Secretary, announced plans to require all rental properties to meet an EPC rating of ‘C’ or above by 2030, a policy first proposed by the Conservatives but later dropped. For landlords, this means facing significant costs to upgrade older properties, which are notoriously difficult to bring up to modern energy standards. A consultation later this year is expected to cap landlords’ spending on upgrades at around £10,000 per property.

With nearly 45% of rental properties already meeting the required EPC rating, many landlords with older homes, particularly those built before 1919, will face a significant financial burden to comply. Chris Norris, policy director for the NRLA, emphasized that landlords need clear guidance and financial support to meet the new standards. However, Labour sources suggest they are prepared for pushback, signalling a potential battle between landlords and the government as the 2030 deadline approaches.

These proposed changes, combined with the uncertainty surrounding CGT, have created a climate of anxiety among landlords. Some are rushing to sell properties before potential tax hikes come into effect, while others are exploring ways to mitigate the financial impact, such as transferring assets to family trusts. The NRLA has warned that further tax increases could exacerbate the supply shortage in the rental sector, making it even harder for tenants to find affordable housing.

“Raising taxes on landlords while tightening regulations is a dangerous combination,” said Rob Stanton, sales and distribution director at Landbay. “While it’s important to protect tenants’ rights, the government must also consider the long-term impact on housing supply. We need a balanced approach that supports both landlords and renters.”

The strain on landlords is already evident in the sharp decline in buy-to-let loans. In the first quarter of 2024, new buy-to-let loans fell by 17.3% in value compared to the previous year, despite recent interest rate cuts by the Bank of England. With rental costs rising - up 8.4% in the past year according to the latest ONS figures - the pressure on landlords is unlikely to ease anytime soon.

Read more: Most landlords express concern over ‘no fault’ evictions ban

As Labour’s housing and tax reforms move forward, landlords face an increasingly challenging environment. The combination of rising costs, stricter regulations, and potential tax hikes could lead many to exit the market, further straining the already limited supply of rental properties. The October Budget will be a critical moment for the sector, as landlords and Buy-to-Let lenders await clarity on the future of CGT and other policy changes.

UK Finance figures show that in the first quarter of 2024, a total of 41,149 new buy-to-let loans were issued across the UK, amounting to £7.0 billion. This represented a decline of 16.7% in the number of loans (and 17.3% in value) compared to Q1 of the previous year.

The UK’s average gross rental yield for buy-to-let properties in Q1 2024 stood at 6.88%, an increase from 6.23% in the corresponding quarter of 2023. Meanwhile, the typical interest rate for newly issued buy-to-let loans was 5.40%, marking a decrease of 30 basis points from the prior quarter but a rise of 0.76 basis points from Q1 2023.

Read more: Is buy-to-let getting too hard?

In line with these interest rate trends, the buy-to-let interest cover ratio (ICR) in the UK averaged 191% in Q1 2024, up from 180% in Q4 2023 but lower than the 206% reported for the same period last year.

The total number of outstanding fixed-rate buy-to-let mortgages reached 1.38 million in Q1 2024, a 3.0% increase from the prior year. On the other hand, outstanding variable-rate loans fell by 14.4% to 596,000.

At the end of Q1 2024, there were 13,570 buy-to-let mortgages in arrears of more than 2.5% of the outstanding balance, unchanged from the previous quarter but up 93% compared to Q1 2023. Additionally, 600 buy-to-let properties were repossessed in Q1 2024, an increase of 39.5% compared to the same period last year.