High street mortgage rate battle could get even hotter

It may still be the country’s fifth largest lender, but with HSBC nipping at its heels and growing market share, Barclays’ mortgage business is under pressure. Barclays PLC released its interim results for the first half of 2024 earlier today – and its mortgage lending business is slipping.

Internationally Barclays made inroads in optimising its lending portfolio, by completion of the sale of its 5.3 billion Euro Italian mortgage book. The strategic move aligns with the bank’s ongoing efforts to streamline operations and enhance financial stability, and will see the bank book a 260 million Euro loss this year on the sale of the business.

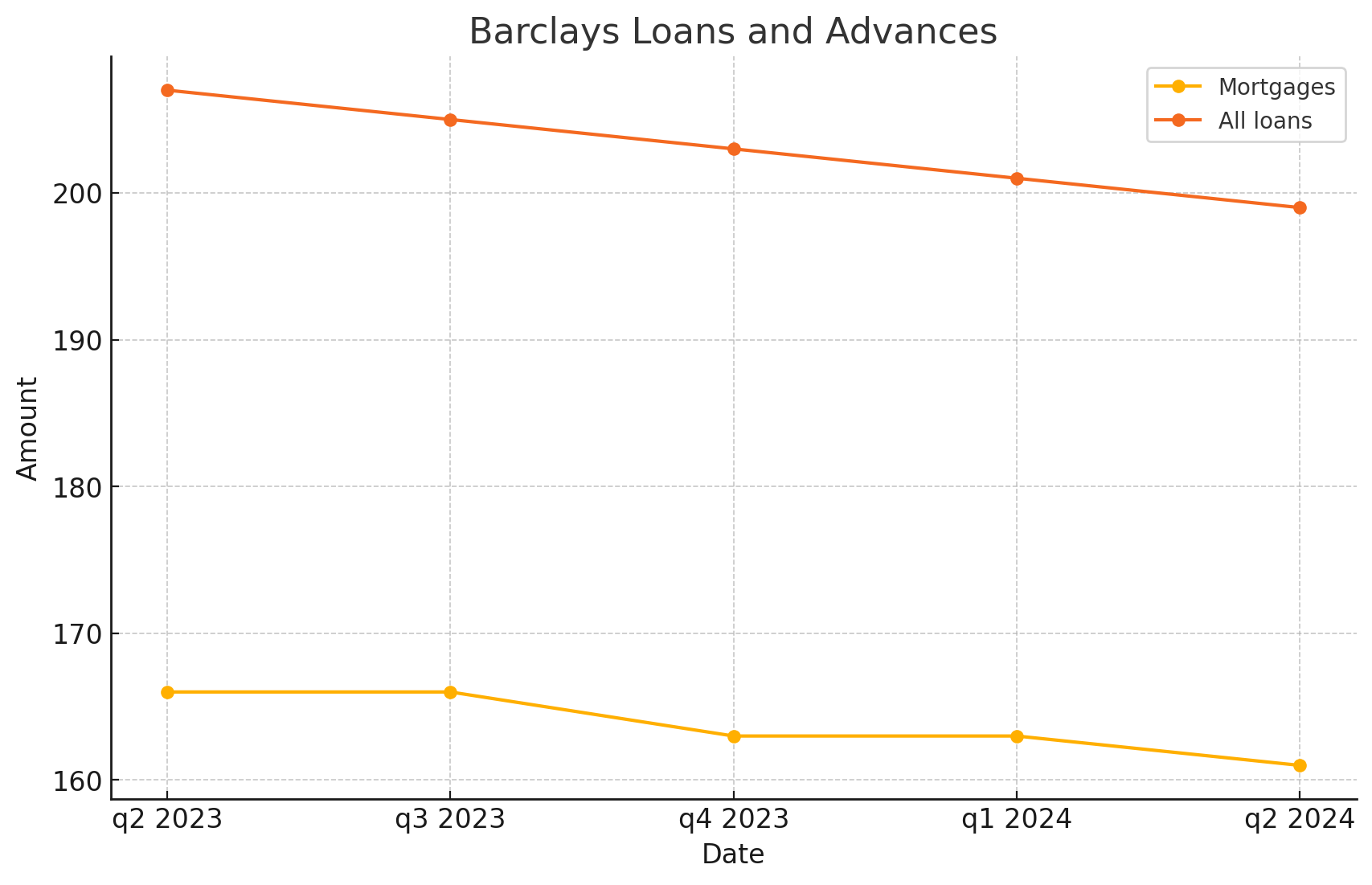

As of June 30, 2024, Barclays’ UK mortgage balances stood at £161.1 billion, down from £163.6 billion in the same period last year. The gross lending flow for mortgages also saw a decline, dropping to £9.2 billion from £12.2 billion. This comes despite the bank cutting interest rates to try to maintain market share.

The bank’s Common Equity Tier 1 (CET1) ratio remained stable at 13.6%, despite the £220 million loss incurred from the sale of the Italian retail mortgage portfolio.

Mortgage pressures have affected the whole UK division’s results. Barclays has reported a 5% decrease in total income, amounting to £3,713 million. This decline was driven primarily by a 4% reduction in net interest income (NII), which fell to £3,146 million. The decrease in NII was attributed to mortgage margin pressure and adverse product dynamics in deposits. However, there were signs of improvement in these areas during the second quarter of 2024. The bank’s cost-to-income ratio in the UK remained steady at 57%, reflecting continued efforts to manage operational costs effectively.

Strategic moves, such as the acquisition of Tesco Bank’s retail banking business, may enhance Barclays’ retail banking footprint. Set to complete in November 2024, this acquisition is expected to add approximately £400 million in annualized net interest income, bolstering Barclays’ lending capabilities and perhaps holding off HSBC’s bid to be the country’s fifth biggest lender.

Barclays also achieved significant efficiency gains, with £0.4 billion in cost efficiency savings realized in the first half of 2024. This contributes to the bank’s goal of £1 billion in savings for the year. In terms of credit management, Barclays reported a significant drop in credit impairment charges in the UK, which fell to £66 million from £208 million. This reduction reflects an improved macroeconomic outlook and robust credit performance across portfolios.

It remains to be seen just how hard Barclays will continue to compete to try to maintain market share, but any competition must be good for intermediaries.