Rental growth also appears to be stabilising

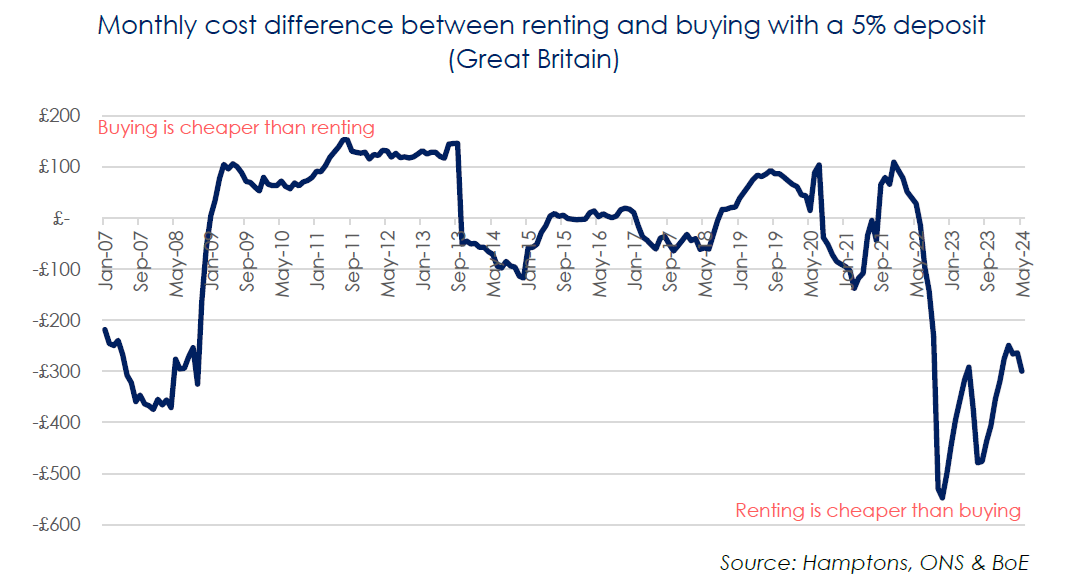

Prospective buyers in Great Britain with a 5% deposit face mortgage repayments averaging £300 more per month than renting the same home, according to data from residential estate agent Hamptons.

The disparity persists despite an annual rental growth rate averaging around 7% across the country each month this year. While buying a home allows owners to build equity, Hamptons said most tenants would struggle to cover the additional £300 per month and pass a stress test at current rates.

Higher mortgage rates have made buying with a 5% deposit financially unviable south of Birmingham. In Scotland and the northern regions of England, including North West, North East, and Yorkshire and the Humber, the cost difference between renting and buying with a 5% deposit is below £100 per month. In the Midlands, the difference ranges from £117 to £122 per month.

Further south, where affordability is more stretched, most renters would find themselves significantly worse off by purchasing a home. In the South West, an average first-time buyer with a 5% deposit pays £341 more per month to buy a similar home. In London, the cost difference rises to £775 per month, equivalent to £9,300 per year.

The Hamptons Monthly Lettings Index has shown that the gap between renting and buying has narrowed since mortgage rates peaked last year. In November 2022, the average tenant in Great Britain would have paid £547 more per month to buy their rental home with a 5% deposit. This has since reduced to £300 more per month.

Despite the narrowing gap, current mortgage rates remain a barrier for most buyers with a small deposit, especially given stress tests at even higher rates. Furthermore, negligible house price growth has slowed the rate at which homeowners can build equity.

According to the Bank of England, the average mortgage rate for a buyer with a 5% deposit is currently 6.1%. Nationally, this rate would need to fall to around 4.2% to equalise the monthly costs of renting and buying with a 5% deposit. In London, the rate would need to drop to 3.6%.

The high cost of buying relative to renting is evident in the current mortgage guarantee scheme, which aims to boost 95% loan-to-value lending by guaranteeing potential lender losses. High interest rates have reduced mortgage guarantees in 2023 to 35% of the 2022 average, with completions at 15% of the level achieved by the Help to Buy scheme.

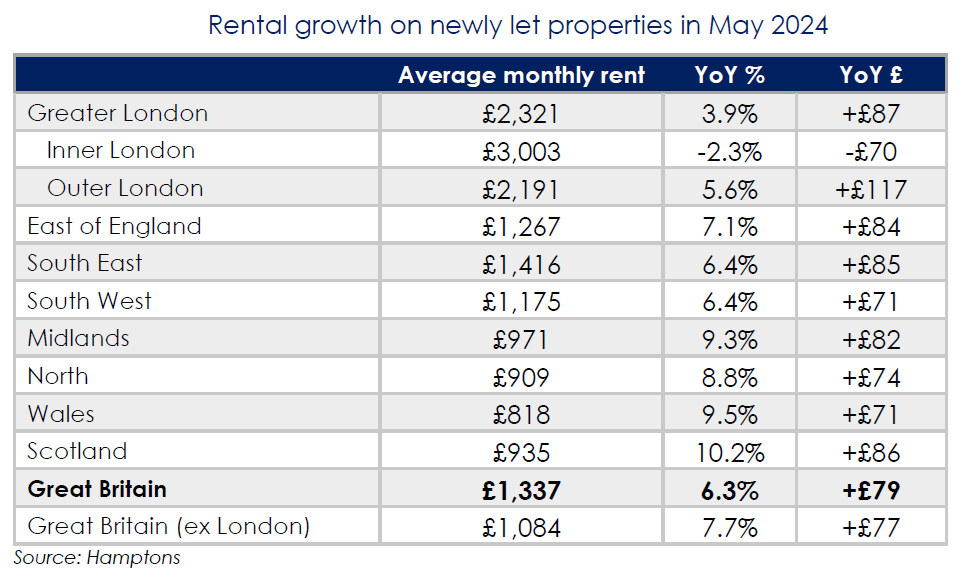

Meanwhile, rental growth appears to be stabilising. The average cost of a newly let home in Great Britain rose to £1,337 per month in May 2024, a 6.3% increase from the same time last year. This marks the third consecutive month where year-on-year increases have averaged around 6%. However, rental growth for tenants renewing their contracts continues to rise, with average renewal rents up 8.8% year-on-year in May, compared to 8.3% in April.

London has led the slowing of national rental growth, with annual growth falling to 3.9% in May 2024, the lowest rate since November 2021. Inner London saw rents fall on an annual basis for the second consecutive month, with the average tenant paying £3,003 per month in May, the lowest level in 14 months.

Smaller homes are experiencing larger rent increases than larger homes, reflecting affordability challenges pushing tenants to seek more affordable options. In May 2024, rents for newly let one-bedroom homes rose 7.6%, outpacing the 6.2% increase for two-bedroom homes.

“Despite rental growth setting at around 6% year-on-year, renting remains more cost-effective than buying for most households across the country,” commented Aneisha Beveridge (pictured), head of research at Hamptons. “High mortgage rates have squeezed buyers with small deposits out of the market, forcing more households to rent for longer. The uplift in the monthly cost to buy a home with a small deposit has made purchases unviable in most places south of Birmingham.

“This analysis also suggests that in a world of high interest rates, the take up of the Conservative’s 0% capital gains tax incentive for landlords to sell to their tenant is likely to be fairly low, too. Rather, a Help to Buy style scheme is better suited to help renters with small deposits become homeowners, particularly when compared to the mortgage guarantee scheme. It was the Help to Buy Equity Loan which aided affordability in the most expensive markets, serving to top up deposits and significantly reduce mortgage repayments for the first five years.

“Persisting affordability pressures have driven competition for Britain’s more affordable rental homes. Smaller homes in traditionally cheaper parts of the country recorded the highest rental growth last month. With tenants squeezed from multiple angles, their ability to save for even a 5% deposit has been curtailed.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.