New revelations indicate that maybe it's not just Barclays that has been looking to buy the Spanish bank

First there were rumours about Santander’s commitment to the UK market – and whether the Spanish headquartered bank was looking to sell off its UK business. Then news broke that the bank’s chairman had announced a shock departure. But then, Ana Botin, executive chair of Banco Santander, who heads the UK unit, told us that Santander had no plans to abandon the British market. ““The UK is not for sale. We love the UK and the UK will remain a core market” she said just two weeks ago.

Unfortunately for the bank, the Financial Times has reignited speculation by revealing that the giant engaged in preliminary discussions with NatWest regarding a potential sale of its British retail business. While the discussions reportedly took place last year, FT sources indicate that interest from both parties remains.

Santander has repeatedly asserted that its UK business is “not for sale”, a statement it reiterated last month after speculation mounted about a possible exit from the British banking sector. One insider, however, has claimed that the Spanish lender has not actively sought buyers for its UK operations. Nevertheless, conversations between Santander and one of the UK’s major banking institutions will likely fuel further debate over its long-term plans.

What would a Santander/NatWest tie-up mean for mortgages?

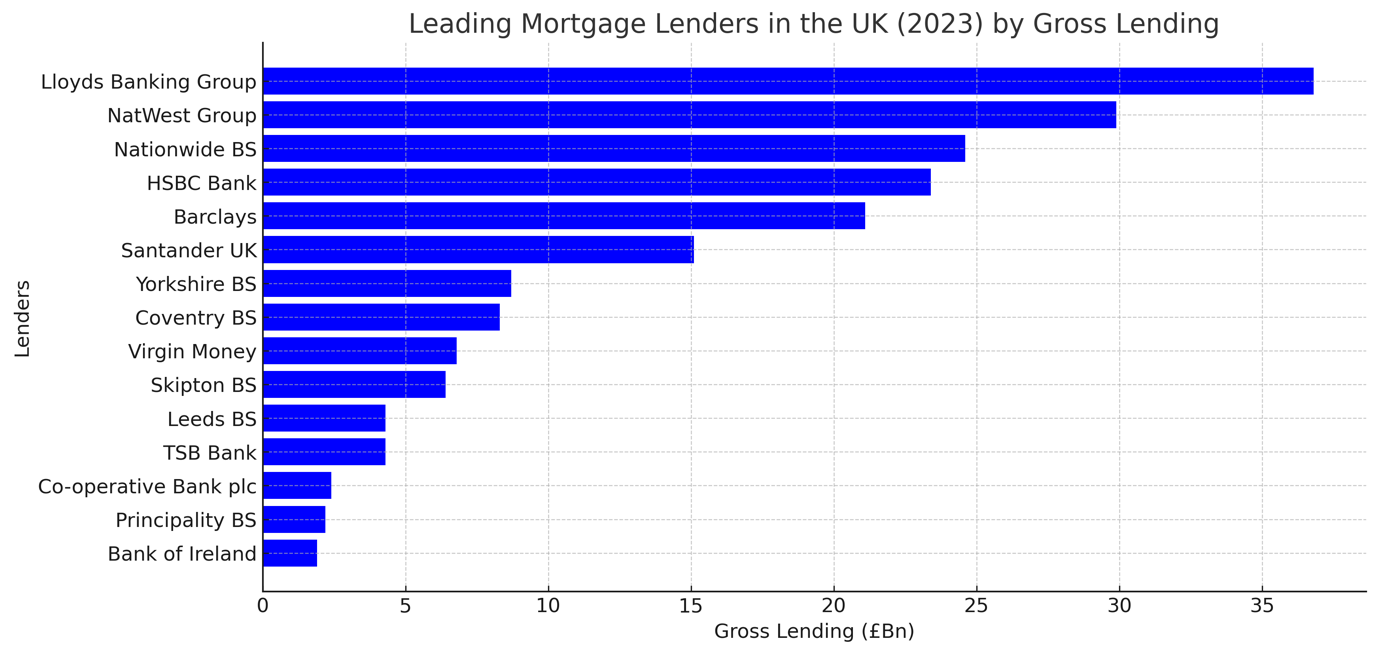

Both banks are big mortgage lenders – any tie up could see the combined entities overtake Lloyds to be the UK’s biggest mortgage lender.

Conflicting signals from Santander leadership

Despite Botin’s denials, industry analysts remain unconvinced, citing challenges posed by Britain’s stringent ring-fencing regulations, rising costs, and more attractive returns in other markets.

Santander UK, formed through a series of acquisitions including Abbey National, Alliance & Leicester, and parts of Bradford & Bingley during the financial crisis, has grown into one of Britain’s largest mortgage lenders. However, tighter regulations and increased competition from domestic banks such as Barclays, Lloyds, and HSBC have made profitability in the UK more difficult. Furthermore, Santander’s leadership shake-up, including the recent departure of Santander UK chairman William Vereker, has done little to quell speculation about its future in Britain.

NatWest’s strategic position

NatWest, which has been scaling up its operations since the financial crisis, could see an acquisition of Santander UK as an opportunity to expand its market presence further. With the UK government poised to offload its remaining stake in NatWest within months, the bank is reportedly evaluating mergers and acquisitions as part of its strategy for growth.

Paul Thwaite, NatWest’s CEO, indicated at the Financial Times Banking Summit in December that the bank was actively seeking expansion opportunities, saying the lender was on the “front foot” for acquisitions. In recent months, NatWest has completed deals, including the purchase of most of Sainsbury’s Bank and a £2.5 billion portfolio of residential mortgages from Metro Bank.

Previous interest from Barclays and regulatory challenges

Santander UK has previously attracted interest from other major banks, with Barclays reportedly making an offer last year that was deemed too low. Some industry observers believe Barclays would be a more natural fit for acquiring Santander’s UK operations, given its expansion ambitions in retail and corporate banking. However, NatWest’s interest could stem from a desire to shed the remnants of its government bailout era by bolstering its market position through acquisitions.

Nonetheless, any major sale of Santander UK would likely face regulatory scrutiny. The Financial Conduct Authority (FCA) is already investigating the bank over mis-selling allegations in the motor finance sector, which has led Santander to set aside £295 million in provisions for potential customer compensation. This ongoing inquiry is seen as a significant hurdle in any potential deal, with analysts predicting that no sale is likely until the issue is resolved.

Santander’s profitability concerns and the UK market

While Santander UK remains a key part of the group’s portfolio, its profitability lags behind its other divisions. The British arm reported net profits of €1.3bn for 2024, a major decline from the previous year, with return on tangible equity - a key profitability measure - also falling below the group’s other major markets. By contrast, Spain and Brazil continue to generate significantly higher profits for Santander.

Despite these challenges, Santander remains keen to highlight its commitment to the UK, particularly as it continues integrating its IT systems with its global operations. It has also been investing in its corporate and investment banking divisions, indicating a potential shift away from its traditional retail focus in the UK.

What lies ahead?

Whether Santander ultimately chooses to stay or sell its UK business, the ongoing regulatory environment and market conditions will play a crucial role in its decision. As Ana Botín has emphasised: “We would like to grow, there are different ways of doing that. The one we’re focused on is organic, through leveraging our global platforms.” However, with interest from major players like NatWest and Barclays, and growing speculation about the bank’s long-term commitment to the UK, Santander’s future in Britain remains uncertain.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.