Average remortgage repayments climb by over £300

Remortgage instructions surged by 23% in March, signalling a potential rebound in activity as homeowners responded to evolving market conditions, according to LMS’ latest Monthly Remortgage Snapshot.

Despite the uptick in new instructions, completions fell 20% from the previous month, reflecting a lag as borrowers move through the remortgaging process. The overall pipeline of activity increased by 10%, indicating that completions may rise in the coming months.

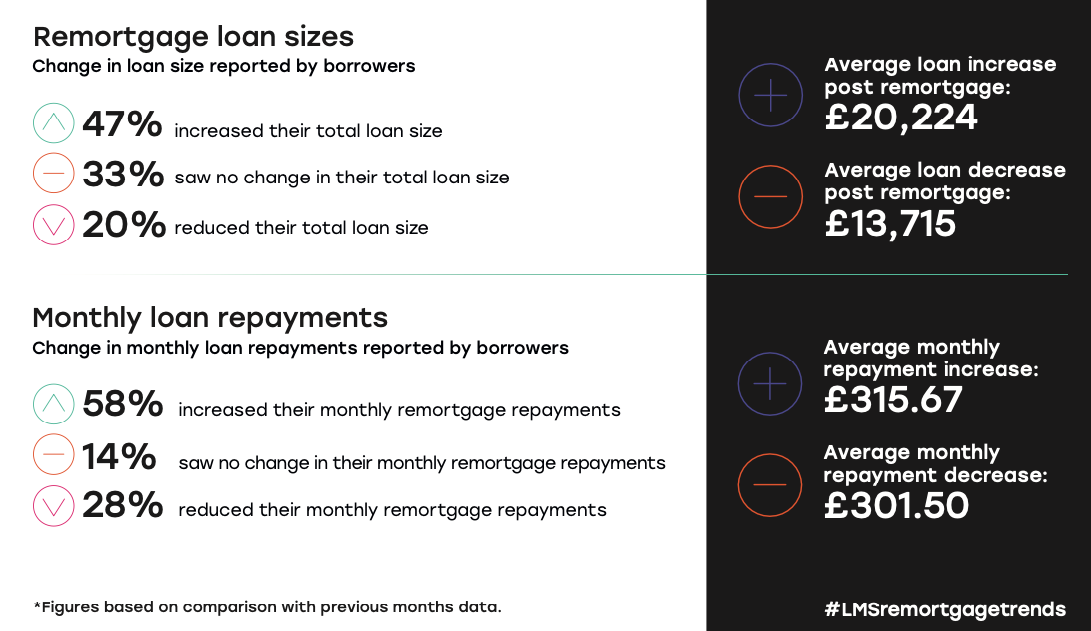

The average monthly repayment for those who remortgaged in March rose by £315.67, a reflection of both rising loan sizes and prevailing rates. Notably, 47% of borrowers increased their total loan amount, with the average increase at £20,224.91. In contrast, 20% reduced their loan size, with an average decrease of £13,715.94.

Five-year fixed-rate deals emerged as the most popular product, selected by 47% of remortgage clients. Two-year fixed options followed at 41%, with longer-term or variable products making up the minority. The desire for payment certainty remained a primary driver, with 74% of respondents citing the appeal of knowing exactly how much they would repay each month.

A significant portion of borrowers - 30% - sought to release equity from their property, while 26% aimed to reduce monthly repayments and 16% prioritised securing current rates amid economic uncertainty.

Regionally, the average remortgage loan in London stood at £319,045, nearly double the £161,298 average across the rest of the UK. Yorkshire reported the shortest average previous mortgage term at 69.95 months (5.83 years), while the North East saw the longest at 82.86 months (6.91 years).

The national average for remortgage amounts dipped 2% to £192,809. Northern Ireland recorded the steepest fall at 19%, while Yorkshire showed a 5% increase.

Commenting on the findings, LMS chief executive Nick Chadbourne (pictured) stated: “The foundations for a positive year are set. March’s figures show an expected seasonal change in cancellations and completions, and pipelines are projected to increase throughout the next quarter. The lowest swap rates we’ve seen in recent years have given lenders the confidence to competitively price their offerings.”

He added that although geopolitical and economic disruptions remain a risk, the strength of current pipelines suggests continued activity in the months ahead.

Borrower expectations around interest rates varied, with 50% anticipating a rise within the year, while 29% had no such expectation.

LMS’ report draws from internal conveyancing data, reflecting activity across thousands of transactions nationwide.

What are your thoughts on the latest findings? Share your insights in the comments below.