Financial Policy Meeting minutes look like good news for borrowers

Over recent months there have been a number of headlines predicting imminent doom for mortgage holders, and a ‘cliff edge’ of refinancing by those on fixed mortgages. But over the last few weeks, rates have slipped driven by the Bank of England’s rate cut and an ongoing battle between the big lenders for market share.

Read more: Barclays market share slips

Into that lead up, the Financial Policy Committee (FPC) has just released its report from its meeting on 19 September 2024. It provides a detailed analysis of how Bank analysis views the UK financial system, including specific insights into the mortgage market and mortgage lending. And the report makes comforting reading as it highlights the resilience of UK households in the face of higher interest rates and evaluates the broader mortgage landscape in the country.

Easing of Mortgage Conditions

The report notes that UK credit conditions have shown signs of easing, a trend influenced by improvements in the macroeconomic outlook. Mortgage rates have decreased slightly since the FPC's previous meeting in June 2024, providing relief for mortgage holders, particularly those with variable rate loans. This easing has been observed even as interest rates remain relatively high, with the Bank of England having cut the base rate to 5% in August 2024. However, it is important to note that while some households are already benefiting from lower rates, a substantial proportion of mortgage holders have yet to refinance at the current rates, particularly those with fixed-rate mortgages.

Impact on Household Debt

The Bank says UK mortgagors are continuing to show resilience despite the pressures of elevated interest rates. Notably, around 20% of mortgage holders are on floating rates, meaning they immediately feel the benefits of lower rates. However, approximately one-third of mortgage holders have yet to refinance at current rates.

It’s not all good news though - mortgage debt service ratio (DSR)—a measure of household mortgage payments relative to disposable income—is projected to increase, given that a number of older low rate mortgages need to refinance, but remains well below the peaks seen in the 1990s and the global financial crisis of 2007-2008. This indicates that, despite the current financial pressures, households are not experiencing the same level of financial strain as they did during past crises.

Graph data: Department for Communities and Local Government (UK)

Mortgage Arrears and Vulnerable Groups

Mortgage arrears and consumer credit arrears have remained largely unchanged since June 2024 and are reported to be low by historical standards. However, the FPC does point out that some lower-income households and renters are under pressure due to the rising cost of living and persistent inflation. This group is particularly vulnerable to financial shocks, although the overall resilience of UK households to these challenges remains strong.

Is six times income too much?

The report also discusses the FPC’s role in regulating mortgage lending through specific policies designed to ensure financial stability. One such policy is the mortgage loan-to-income (LTI) ratio, which limits the number of high-LTI loans (those with a loan-to-income ratio of 4.5 or higher) that banks can issue. The FPC reminded lenders that this policy remains in place, ensuring that banks limit the proportion of risky mortgage lending to 15%. The FPC emphasises the importance of this policy in maintaining stability, especially in the context of the current economic environment where financial market vulnerabilities are still present.

Read more: Nationwide offers six times income mortgage

Future Outlook and Risks

While the UK mortgage market appears to be stabilizing, the FPC expresses caution regarding future risks. The report cautions that the financial system remains susceptible to external shocks, including geopolitical uncertainty and volatility in global financial markets. A sharp correction in asset valuations could affect the availability and cost of credit for households, which would have direct implications for the mortgage market.

The FPC’s next meeting will be on 15 November 2024 and the record of that meeting will be published on 29 November 2024.

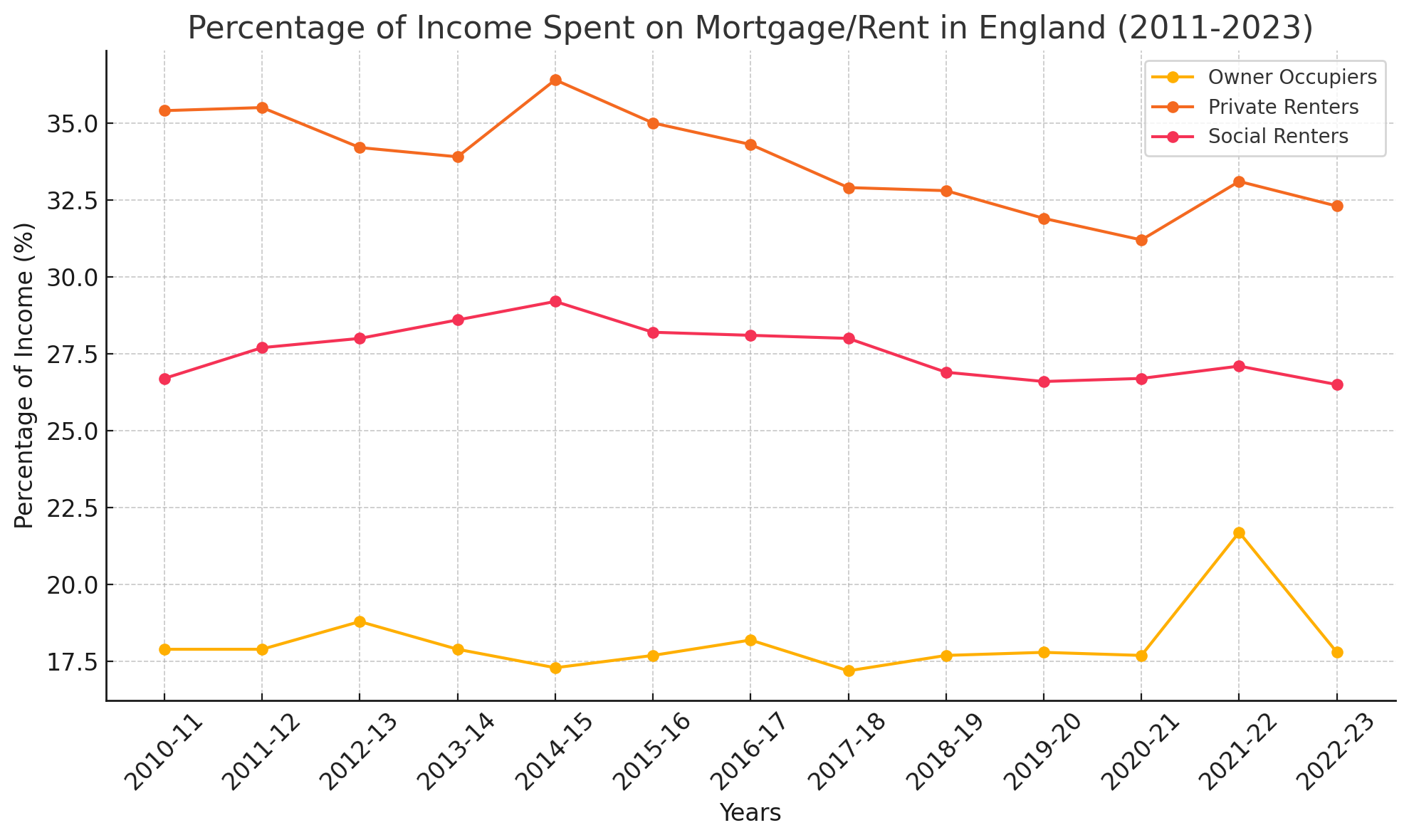

How much of our disposable income do we spend on property?

1. Owner-Occupiers:

- The percentage of income spent on mortgages has remained relatively stable for owner-occupiers, hovering around 17% to 18% for most of the period, with a notable peak in 2021-22 where it rose sharply to 21.7%.

- By 2022-23, it dropped back down to 17.8%, indicating some fluctuation during these years.

2. Private Renters:

- Private renters consistently spend a significantly higher proportion of their income on rent compared to owner-occupiers.

- The percentage fluctuated from a high of 36.4% in 2014-15 to a lower point of 31.2% in 2020-21. However, there has been a slight rise again in recent years, reaching 32.3% in 2022-23.

3. Social Renters:

- Social renters, on average, spend less of their income on rent compared to private renters, with percentages ranging from 26.5% to 29.2%.

- Over the years, social renters' rent costs as a percentage of income have remained relatively stable, with some minor fluctuations. The highest percentage was seen in 2014-15 (29.2%), while it was 26.5% in 2022-23, slightly below the earlier years.

Summary:

- Stability for Owner-Occupiers: While owner-occupiers have seen some variation, the overall percentage of income spent on mortgages has remained fairly consistent, with a temporary peak in 2021-22.

- High Burden on Private Renters: Private renters bear a larger burden, spending over 30% of their income on rent throughout the period, with fluctuations but no significant relief over time.

Moderate Stability for Social Renters: Social renters, while still spending a considerable amount of income on rent, experience more stability in terms of the percentage of income spent, though they consistently spend less compared to private renters.