NPAT down 38% in first half of 2024, as net interest margin also falls

Home loan market competition and compressed net interest margins have contributed to AMP Bank returning underlying net profit after tax of $35 million for the first half of 2024, down 38.6% on 1H 23.

The latest financial results for the bank, released on Thursday, August 8, along with AMP’s overall half year 2024 results, show credit quality remains strong and its plan to launch a small business digital bank for Q1 of 2024 is on track.

AMP revealed how the group was performing across its various business units, including AMP Bank, Platforms, Superannuation and Investments, Advice and New Zealand.

The results overview included:

- Overall underlying NPAT for AMP Group up 5.4% to $118m (1H 23: $112m)

- AMP Bank – underlying NPAT of $35m (1H 23: $57mn), reflecting previously flagged NIM compression. Credit quality remains strong

- Platforms – underlying NPAT of $54m (1H 23: $44m), with improved net cashflows and disciplined cost management. IFA flows now 35% of inflows and are up 30%

- Superannuation & Investments – (formerly Master Trust) underlying NPAT of $34m (1H 23: $28m), with stable margins and ongoing reduction in outflows

- Advice – underlying NPAT loss of $15m (1H 23: $25 million), an improvement of 40% on 1H 23. Transformational partnership for AMP Advice announced today

- New Zealand – underlying NPAT stable at $17m

AMP chief financial officer Blair Vernon (pictured above left) said overall the business unit performance metrics were delivering against the group’s guidance, plans and the commitments it had made.

“Whether that’s stabilising margin in the bank and earnings, growing our wealth businesses, trimming the loss in Advice and Group or steady performance in New Zealand – so overall a very good result,” Vernon said during an analyst briefing on the results.

AMP Bank home loan volumes

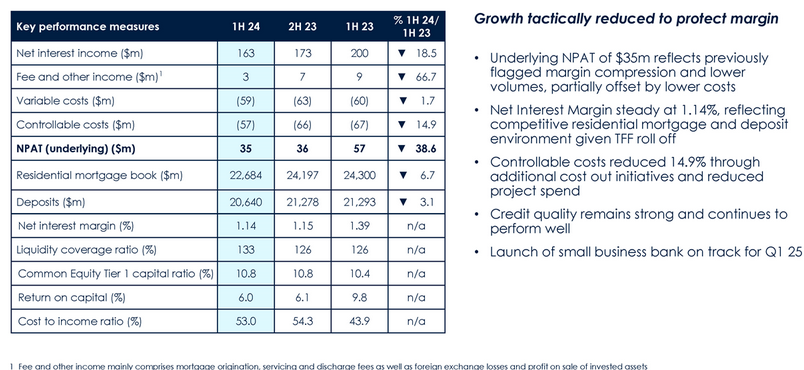

Vernon said while profit was down 38.6% for the half to $35m compared to 1H 23, it was broadly steady with 2H 23 outcomes, including $36m NPAT for that period.

“That really reflects the stabilisation in NIM you will see during the half where we have averaged 114 basis points, so within the guidance band we provided in the full-year results.

“Home loan volumes are slightly lower than we anticipated in the first half – that really reflects that intense competition we continue to see in the home loan market segments that we play in, relative to the balancing of our focus on margin management as our most important aim.”

AMP Bank First Half 2024 results

Source: AMP Bank

However, Vernon said costs had been reduced in the bank as it saw lower overall volumes and careful management of costs “given that we knew the NIM compression was occurring”.

The bank had overall, returned a very good result for the half.

“We are seeing some increased volumes again in the last few weeks, so we are hopeful of some improved volumes for the second half, getting us closer back to that open position in terms of volumes overall.”

Net interest margin

AMP Bank’s NIM for the first half of 2024 was broadly stable at 1.14%, compared to 1.15% for 2H 23.

Vernon said there had been some positive asset mix changes, involving two elements – back book to front book maturities, and fixed rate rollovers to variable rate loans, with some remaining fixed rolls to occur in the second half which the bank would watch closely.

“Offsetting that is the ongoing competitive pressure in the deposit market and particularly in this half for us has been call deposits, so some margin contraction there.”

Credit quality

The bank’s credit quality was positive overall when looking at the total book, said Vernon.

“There has been an increase in 30 and 90-day arrears, albeit we don’t see those trends as necessarily inconsistent with the sector overall and in recent weeks have seen them levelling off.”

There had only been $220,000 of write-offs in the half, reflecting AMP Bank’s very conservative debt position.

Source: AMP Bank

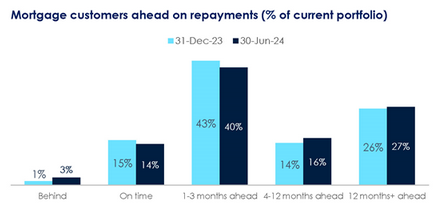

Vernon said in terms of forward indicators, two-thirds of the bank’s clients enjoyed an LVR of under 70%, while eight out of 10 customers were ahead on mortgage repayments and four out of 10 were ahead by four months.

“It shows the majority of our clients weathering the current pressure in terms of the mortgage market.”

Small business digital bank

AMP CEO Alexis George (pictured above right) said the launch of the company’s digital small business bank was on track for Q1 25 as part of a strategy to diversify revenues and funding mix in AMP Bank.

“We intend to soft launch our small and micro business and consumer bank in the fourth quarter [2024] to friends and family and publicly in the first quarter of next year,” George said.

“Recently, Engine by Starling which is the platform we are embedding into Australia was supportive of a new bank that launched in Romania and that scaled and performed very well which gives us additional comfort that we’ll be able to do the same in Australia.”

Looking at AMP’s overall results, George said the company had made good progress this half on its key strategic commitments.

“We have positive momentum heading into the second half of the year. We have continued to deliver on simplification and cost reduction, while also driving growth in our wealth businesses and returning capital to shareholders.”

AMP also today announced a new strategic partnership and ownership structure with Entireti Limited (Entireti) and AZ Next Generation Advisory Limited (AZ NGA) for its AMP Advice business. The aim of the partnership is to create a sustainable business model for AMP Advice.

In the results, AMP revealed an FY24 interim dividend of 2c per share, 20% franked and that $158m of tranche 3 on-market share buyback was completed in 1H 24.

What do you think of AMP Bank’s 1H 2024 results? Comment below