But consumer distrust in AI persists, study finds

ComplyAdvantage has released its annual report, The State of Financial Crime 2024, focusing on fraud, money laundering, and financial crime.

The report has shed light on the criminal use of artificial intelligence (AI) as an emerging fraud challenge while highlighting consumer discomfort with AI, even when employed for their protection.

“Today, AI is being utilised by both criminals – who are using it as new ways to defraud customers – and institutions, who are using it to stay ahead of fraudsters and defend their customers,” said Vatsa Narasimha (pictured above), CEO of ComplyAdvantage.

“We know from our work with financial institutions around the world that AI-based technologies can significantly enhance the fight against financial crime. We see a tremendous opportunity for banks to show consumers how these new technologies and processes like explainable AI are being used to safeguard their finances.”

Artificial intelligence: A double-edged sword

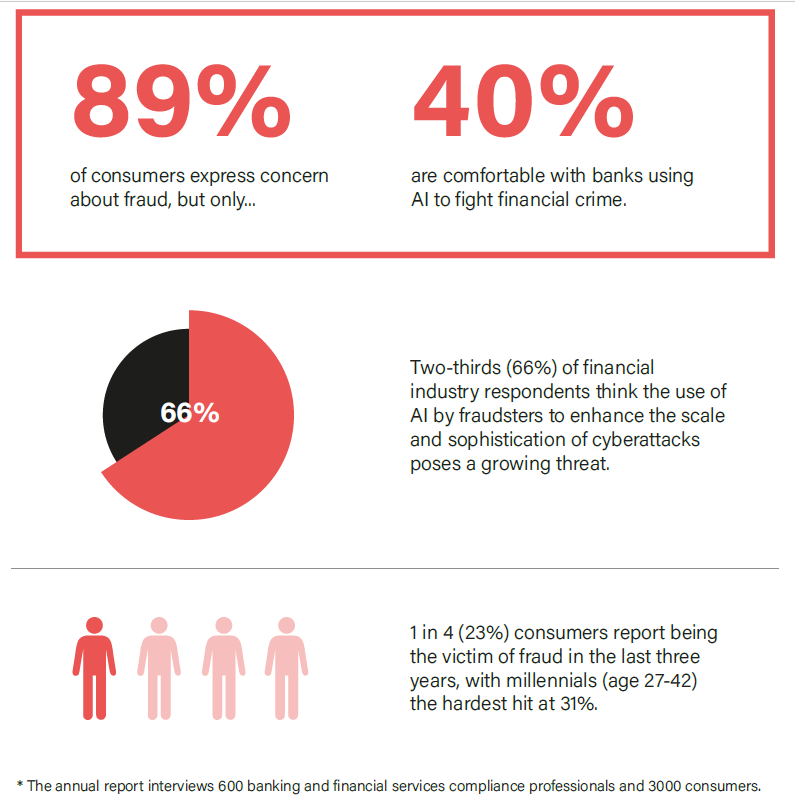

The study found that 66% of financial industry respondents see the use of AI by fraudsters as a growing cybersecurity threat, encompassing risks like deepfakes, cyber hacks, and generative AI for creating malware.

While 86% of financial institutions invest in new technologies to counteract these threats, only 53% prioritise explaining AI usage to customers.

“Whether they use AI to identify fraud patterns, analyse networks, or streamline processes, banks can take the lead on what we believe will be a key trend in 2024: explainability,” Narasimha said. “Namely, the ability of financial institutions to demonstrate to their customers how and why AI models have taken decisions that affect them.”

Compliance leaders needed not worry about customer reception too as the survey indicated that 65% of consumers were open to banks sharing transactional details with others for fraud detection.

Payment fraud challenges

ComplyAdvantage findings also showed 60% of industry executives reporting that payment fraud remained at high levels, with 8% noting an increase in the last 12 months.

Meanwhile, 89% of consumers expressed anxiety about potential fraud, and 23% reported being victims in the last three years, with millennials facing the highest incidence at 31%.

Survey participants commonly reported experiencing various types of fraud, with credit card fraud affecting 59%, identity theft and phishing attempts impacting 21%, employment scams targeting 12%, and investment fraud affecting 10%.

“Millennials have embraced digital payments and mobile banking, which dominate how we access banking services today,” Narasimha said. “The scale of fraud amongst this generation demonstrates how quickly criminals exploit technology and changes in consumer behaviour.”

Unpacking instances of “friendly fraud”

One in five consumers acknowledged engaging in "friendly fraud," revealing behaviours such as disputing a payment after receiving an unsatisfactory response from a merchant (21%), challenging a payment later recognised as legitimate (12%), and seeking a debit or credit card refund without returning the item (9%).

“The surprisingly high level of ‘friendly fraud’ uncovered in our survey shows just how widespread and complex fighting fraud can be when consumers can - even inadvertently – commit behaviour that may raise a red flag with their bank,” said Iain Armstrong, regulatory affairs practice lead for ComplyAdvantage.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.